Understanding the forces behind the wave.

The past two years have been a season of resets. Bankruptcies, closures and pivots captured the headlines, but another equally important story has been consolidation. While the word can feel like a euphemism for weakness, the reality is more nuanced.

Consolidation is being driven by the same macro forces that have reshaped the entire consumer economy: rising customer-acquisition costs, compressed margins, investor pressure and a landscape dominated by trillion-dollar retailers. For some companies, scale has become the price of admission; for others, smart combinations are an accelerant to product depth, field stability and global reach.

It’s important to note that not all consolidations have been proactive growth plays. Several were rescue missions—moves designed to preserve value from distressed assets and protect distributors and customers from disruption. Together, both growth-driven and rescue-driven deals are reshaping the competitive map. As my good friend and strategic expert Tony Jeary says, when you want results, act with clarity, focus and execution.

Direct selling is not the first sector to consolidate around leaders who can provide stability and innovation. What is unique here? The deeply personal connections at the heart of the model—consolidation is not just about spreadsheets. It’s about how well cultures blend; how effectively distributors are ushered in; and whether customers feel continuity rather than disruption.

Done well, consolidation is a way to evolve with speed.

Recent Deals and Why They Matter

Material consolidations have reshaped the direct selling landscape. Each one not only shifted company trajectories but also revealed larger patterns in how scale, science and strategy are driving the channel forward.

December 2023 & February 2024—Vida Divina Acquires MIALÉ and Radien

In December 2023, Vida Divina acquired Peruvian company MIALÉ, a wellness brand with a strong presence in South America. The deal gave Vida Divina access to MIALÉ’s established distributor networks, in-houses manufacturing capabilitiesand exciting intellectual property around its skincare line. This move strengthened the company’s foundation in a key regional market while adding depth in both wellness and beauty categories.

Then in February 2024, Vida Divina purchased Radien, a Tennessee-based skincare brand known for its clinically backed formulations and licensing of wound-healing technologies. Radien brought to Vida Divina brand equity, advanced skincare IP and product development expertise. The transaction value was reported to be as high as $100 million with performance incentives, reflecting confidence in Radien’s innovation pipeline and market potential.

Why it matters: These acquisitions extended Vida Divina’s footprint in both Latin America and North America while broadening its product base across wellness and skincare. MIALÉ added regional strength, distributor reach and manufacturing depth, while Radien introduced advanced skincare science and IP through a landmark deal. Together, they positioned Vida Divina to compete more aggressively in daily-use wellness and beauty categories.

January 2024—Beauty Bank Acquires Amare Global

Beauty Bank, led by David Chung, acquired Amare Global in January 2024. Amare had carved out a niche in gut-brain health and mental wellness and, in 2022, had itself acquired Kyäni to expand into antioxidant-rich nutrition and cellular wellness. Together, Amare and Kyäni represented a diversified product story built on daily-use categories with international reach. Beauty Bank viewed the combination as a way to expand its wellness footprint with proven product lines and a community already primed for growth.

Why it matters: This deal highlighted how acquiring strong product platforms—mental wellness, gut health and nutrition—can accelerate category expansion. Beauty Bank gained a credible portfolio anchored in sticky, consumable products with global potential.

July 2024—Greenway Global Acquires Some Assets from Jeunesse

As a rescue mission, Greenway Global responded to Jeunesse’s plea for help and stepped in to acquire Jeunesse, one of the industry’s most visible international wellness/beauty brands. The stated aim: steady the global footprint, refresh the commercial engine and lean on a stronger capital/ops base to restore growth.

Both Greenway Global and Velovita acquired portions of the Jeunesse business in separate transactions, underscoring the complexity of parsing a global platform into distinct pieces. The legal and operational untangling of those assets is still unfolding, but for the distributors and customers involved, the emphasis has been on continuity and product access.

Why it matters: This was as much about stabilization as growth. Jeunesse had faced mounting pressures, and Greenway’s role was effectively to rescue a legacy global brand from decline—protecting distributors and preserving valuable product lines while positioning the platform for renewed relevance.

October 2024—Velovita Acquires Additional Jeunesse Assets

Months later, a Velovita affiliate claimed to acquire select Jeunesse assets, including international markets in Asia-Pacific and Europe. For Velovita—a biohacking-forward brand with a digital edge—these assets added product range and access to complementary customer segments.

Currently, the dispute between Greenway and Velovita over the acquired Jeunesse assets is ongoing in a Florida court case. Ultimately, it’s clear both companies benefited from the deal, expanding their product range and securing access to additional customer segments.

Why it matters: By absorbing valuable product lines and communities, Velovita gave parts of Jeunesse new life under a brand positioned to grow them.

November 2024—Party Products Acquires Tupperware Assets

A consortium of lenders operating under Party Products LLC acquired Tupperware, rescuing the storied kitchenware brand from financial distress. Following the acquisition, Tupperware restructured its global footprint: closing its US manufacturing plant and shifting production to Mexico, exiting markets like Australia and pivoting select markets from direct selling to retail and ecommerce. At the same time, operations in core geographies—including the US, Canada, Mexico, Brazil, China, South Korea, India and Malaysia—were retained and strengthened, with the Tupperware name continuing under Party Products’ umbrella.

Why it matters: This was as much a rescue as a reset. By stabilizing the Tupperware brand while scaling back underperforming regions, the acquirers preserved an iconic name; rebalanced its geographic priorities; and set the stage for a hybrid future spanning direct sales, retail and digital channels.

December 2024—USANA Acquires Controlling Stake in Hiya Health

Late last year, USANA acquired a 78.8 percent stake in Hiya Health, a fast-growing children’s nutrition brand built on a subscription-based DTC model generating more than $100 million in trailing net sales. Importantly, Hiya continues to operate as a standalone business with its own leadership, systems and DTC-first approach.

This was not a consolidation. Instead, it marked USANA’s expansion into a new category (children’s health) and a new marketing channel (direct-to-consumer subscriptions). Hiya gained USANA’s scientific credibility and access to international distribution, while USANA gained exposure to a younger demographic and a recurring revenue engine that complements—but does not integrate with—its traditional direct selling model.

Why it matters: This was a textbook case of portfolio expansion, not channel consolidation. By adding Hiya, USANA broadened its reach into DTC marketing while preserving Hiya’s independence. The partnership also gives Hiya a faster path to international markets through USANA’s global infrastructure, creating growth opportunities without forcing integration.

Q1 2025—L’Occitane Takes Full Ownership of LimeLife

In early 2025, L’Occitane International acquired the remaining shares of LimeLife by Alcone, a brand known for its professional-grade cosmetics and passionate field following, that it didn’t already own. The decision came at a time when LimeLife required additional support, and L’Occitane stepped in to provide the stability needed to keep the brand and its community moving forward. Full ownership gave L’Occitane the ability to more closely align LimeLife with its broader beauty strategy while maintaining the social-selling strengths that made the brand distinctive.

Why it matters: This move was about continuity as much as strategy. By fully absorbing LimeLife, L’Occitane ensured that its field community and product portfolio had a secure home while also broadening its own reach in social selling. It demonstrated how consolidation can serve both as a safeguard and a growth platform, reinforcing the value of product adjacencies between retail and direct selling.

April 2025—Herbalife Acquires Majority Interest in Pro2col, Prüvit and Link BioSciences

Herbalife recently announced it would acquire majority stakes in both Pro2col—a new wellness-tech platform—and Prüvit, the ketone-focused brand with an established customer base.

The first phase of Pro2col Beta launched in July, with full US commercialization planned for 2026. Positioned as Herbalife’s next-generation personalized wellness platform, Pro2col integrates personal data & biomarkers, targeted supplementation, lifestyle habits, coaching and community into a single experience. The platform delivers a personalized daily plan—your “Pro2col”—to guide customers through consistent, trackable behavior change designed to support customer health goals and amplify distributor connection.

Herbalife also acquired a 51 percent stake in Link Biosciences, a software company powering personalization and customized product delivery. The Link platform provides not only the technological backbone but also the manufacturing experience for personalized nutrition—an emerging frontier for the channel.Meanwhile,Prüvit continues operating during a transitional period.

Why it matters: This deal was about optionality and future positioning. Herbalife gained both an innovation platform (Pro2col) and a personalization engine (Link Biosciences), alongside Prüvit’s established community. Together, these moves demonstrate how a global player can hedge bets and expand category relevance by layering new capabilities onto its existing scale.

May 2025—Shaklee Acquires Modere Assets

Shaklee announced in May 2025 that it had acquired Modere’s assets, including trademarks, patents and its flagship Liquid BioCell collagen line. The deal also included access to Modere’s product IP pipeline, giving Shaklee a foothold in collagen-based innovation and related beauty-from-within categories. In addition, Shaklee invited Modere’s “Social Marketers” to join its field organization, offering an immediate pathway for distributors to continue their work under a stable, established brand. For Shaklee, the move was as much about strengthening its beauty and wellness positioning as it was about bringing a displaced community into its fold.

Why it matters: A product-led rescue acquisition with upside. Shaklee gained a marquee collagen portfolio and a ready-made distributor network, while Modere’s community was offered continuity under a trusted brand. It demonstrated how consolidation can preserve value even from distressed situations while broadening a company’s product relevance.

Notable but Smaller Moves

Beyond the larger deals, a handful of other smaller deals offer equally important insights into where the channel is headed.

January 2024—Neora Acquires ACN Korea

Neora announced the acquisition of ACN Korea as part of its expansion across Asia Pacific. The two companies share a long history of collaboration, and the transaction brought ACN Korea—one of the top players in its sector—under the Neora brand. Leaders from both companies emphasized the cultural alignment and opportunity to accelerate growth in South Korea and beyond.

Why it matters: This deal demonstrated how regional consolidation can strengthen global ambitions. For Neora, acquiring ACN Korea not only deepened its Asia Pacific presence but also added a well-established team and distributor base in one of the region’s most competitive markets.

September 2024—Scout & Cellar Joins Full Glass Wine Co.

DTC portfolio company Full Glass Wine acquired Scout & Cellar alongside e-tailer Splash Wines. Around the same time, Splash Wines had also absorbed customers from the shuttered Traveling Vineyard, further consolidating wine subscription and direct selling audiences under its umbrella. These deals were positioned to push the combined entity beyond $125 million in revenue by tapping shared fulfillment, ecommerce and brand synergies.

Why it matters: This wasn’t a traditional DS-on-DS consolidation. Instead, a DTC aggregator absorbed a direct seller to capture brand equity and community while offering scale economics in return. Expect more cross-model pairings in the future.

November 2024—Stemtech Merges with VIÁGO

Stemtech and lifestyle platform VIÁGO announced a merger under a public-company umbrella. VIÁGO is the former Seacret Direct business, which had previously acquired assets of WorldVentures. The strategy highlighted a recurring theme: pair a wellness core with lifestyle membership to expand appeal and customer lifetime value.

Why it matters: Wellness plus lifestyle utility can add meaningful stickiness. By folding the legacy of WorldVentures into a broader platform, the merger illustrated how consolidation can also be about reimagining assets in new configurations. The real test will be integration—comp plans, communities and technology.

September 2025—LifeVantage Acquires LoveBiome

LifeVantage announced its acquisition of LoveBiome, a move designed to deepen its science-backed wellness credentials and expand its gut-health portfolio. The deal brought together complementary products, overlapping field leadership and shared R&D.

Why it matters: Science and proof points remain the currency of credibility. In a crowded wellness market, consolidations that sharpen a company’s evidence-based positioning are more likely to strengthen both recruiting and retention.

Zinzino’s Strategy: A Case Study in M&A Success

Few companies have leaned into consolidation as effectively as Zinzino. Its expansion playbook stretches back several years, beginning with the 2020 acquisition of VMA Life, which added a foothold in personalized nutrition and a new base of distributors in key European markets. In 2022, Zinzino followed with the acquisition of Enhanzz Global, a Swiss direct sales company with a portfolio spanning premium skincare, fashion and wellness. These earlier moves laid the groundwork for Zinzino’s multi-category expansion strategy and demonstrated its ability to integrate both products and field organizations effectively.

The roll-up accelerated in May 2024 with the acquisition of Xelliss, a spirulina-based nutrition and cosmetics company in Southern Europe, bringing both plant-based products and a new distributor base into the fold. Next, Zinzino absorbed European distributor assets from ACN, further enlarging its field base and reach. In February 2025, Zinzino expanded further into North America by acquiring Zurvita, best known for its healthy drinks and nutrition products. The deal paired Zurvita’s loyal distributor community across the Americas with Zinzino’s science-first positioning and European infrastructure, strengthening transatlantic scale.

In April 2025, Zinzino added Valentus Global, acquiring its distributor database, inventory and IP to bolster European distribution. Two months later, in June 2025, it absorbed Ecosystem SAS, a French wellness company that broadened both its product range and its field footprint. By September 2025, Zinzino announced the acquisition of Bodē Pro, gaining customer records, IP and distributor assets across North America and Japan. The move added roughly $7 million in annual revenue and expanded Zinzino into metabolic and energy categories.

Around the same time, the company also acquired Truvy, the Utah-based wellness brand with strong momentum in weight management and communities across North America, Latin America and South Korea. This underscored Zinzino’s intent to solidify its presence in key geographies while adding further depth in daily-use health categories.

Across all these transactions, Zinzino relied heavily on its strong stock performance as deal currency—an advantage that gave it flexibility and confidence to pursue acquisitions that would be more difficult for privately held firms. Importantly, these transactions were about more than products: they were also about acquiring established field organizations and customer lists that delivered immediate volume and reach.

Why it matters: Zinzino’s roll-up strategy shows that consolidation isn’t just about headline mergers. By layering in products that meet daily consumer needs—nutrition, energy, weight management—while simultaneously securing experienced distributor networks, Zinzino has built one of the broadest and stickiest portfolios in the channel.

Why Now?

The surge in deal activity isn’t random—it reflects mounting pressures converging at once. For many companies, consolidation has shifted from “optional” to “necessary”. Here are four reasons why:

Economic realities

Inflation, shrinking margins and escalating customer acquisition costs have exposed the vulnerability of companies without scale. Larger platforms can absorb those pressures; smaller ones often cannot.

Capital expectations

Investors want predictability and profitability, forcing leadership teams to find efficiencies and revenue stability faster than organic growth alone can deliver.

Competitive benchmarks

With Amazon and Walmart controlling consumer expectations on price, speed and convenience, joining forces is often the only way to present a credible alternative.

Field dynamics

Distributors gravitate to brands with tech, compliance and marketing at a modern standard—lacking those resources risks attrition.

Taken together, these forces have created an environment where consolidation has become a viable path to resilience.

Four Emerging Patterns

Beyond the headline announcements, several clear themes are beginning to take shape. These patterns not only explain why certain deals have happened but also hint at what will define successful consolidations going forward.

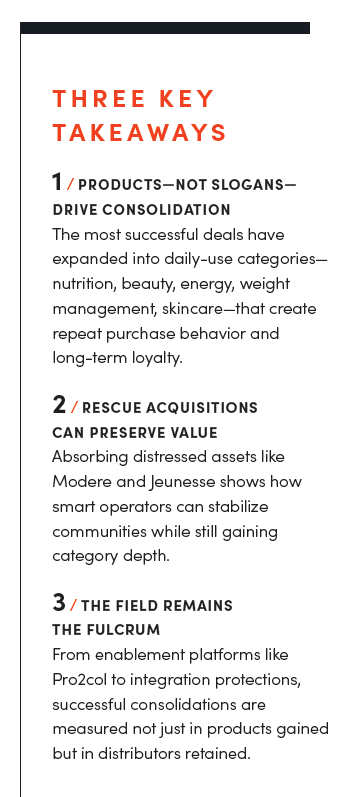

- Portfolios are being built around daily-use products, not slogans.

The material deals above consistently add items customers use every day—nutrition, collagen, energy, weight management, gut health, core skincare/cosmetics. That’s what lifts reorder rates and household lifetime value. - Hybrid portfolios are deliberate plays.

The USANA–Hiya deal is the clearest example. This was not a consolidationbut a portfolio and channel expansion. By taking a controlling stake while allowing Hiya to remain a standalone DTC business, USANA gained exposure to children’s health and subscription-based retention while preserving the independence and momentum of both brands. It also positioned Hiya to accelerate international growth with USANA’s infrastructure. This hybrid approach is likely to be repeated as companies seek both diversification and stability. - Rescue missions have a place.

Deals like Greenway’s absorption of Jeunesse assets and Shaklee’s acquisition of Modere’s collagen line show that not all consolidation is proactive. Some moves are designed to preserve value, protect customers and give distributors a viable home. When handled well, rescue acquisitions can stabilize communities while still adding product depth to the acquiring company. - Integration and infrastructure remain decisive.

Financial terms grab headlines, but continuity wins loyalty. Protecting hero products, ensuring tech fit and keeping the field whole are hallmarks of success. Cross-border compliance, data systems and modern enrollment/ecommerce platforms are now baseline requirements, which is why moves like Herbalife’s Pro2col investment reflect enablement as much as product logic.

The Road Ahead

While some consolidation activity occurred in 2022 and 2023, this article has focused specifically on the last 24 months—when deal-making reached a new level of intensity and strategic clarity.

And the consolidation wave is unlikely to subside anytime soon. Smaller brands will continue to seek shelter under larger umbrellas, while well-capitalized players will look for acquisitions that expand their product breadth, geographic reach, scientific credibility and digital capabilities.

But it’s important to recognize that many of these moves are primarily at their core about field acquisition. Access to experienced distributors and their customer networks remains one of the fastest ways to secure growth. The winners will be those who treat consolidation not only as a financial or product play, but as a strategic move that respects and retains the field.

Not every deal will succeed—cultural mismatches and integration missteps remain real risks. But the throughline is clear: the companies that align product depth with field continuity and distributor trust will come out on top.

Direct selling has always been about community and trust. Consolidation—done well—can strengthen both. The opportunity is to build companies that compete at scale and stay true to the values that make this channel unique.

If leaders approach it with clarity, care and courage, consolidation won’t mark the end of an era, but usher in the beginning of an even stronger one.

Why Products Lead the Way

Consolidation in direct selling isn’t just about scale—it’s about building the right mix of products that keep customers engaged every day.

- Everyday use matters

Nutrition, energy, beauty and weight management products fit naturally into customers’ routines, creating repeat purchase behavior.

Ask yourself: Will this deal add products customers use daily—or ones they’ll buy once and forget? - Proof drives adoption

Products with measurable outcomes—better energy, visible beauty results, weight loss—fuel referrals and retention.

Ask yourself: Can we defend and communicate the results of our combined product line? - Portfolio synergy

Products that complement each other across categories strengthen relevance, increase customer stickiness and build broader daily-use portfolios.

Ask yourself: Does this lineup simplify and strengthen our message? - Customer favorites

From skincare to supplements, customers expect continuity of their hero products. Lose those, and loyalty slips away.

Ask yourself: Are we protecting the products people love most? - Brand architecture

Some companies can operate independently, while others thrive under full integration. The key is clarity.

Ask yourself: Will these brands live side by side or integrate fully—and can the field explain it in one sentence? - Field continuity

Protecting distributor stability is non-negotiable. Comp changes or unclear migration paths can unravel even the best deal.

Ask yourself: Have we secured commitments from top leaders and built protections that keep the field whole for the next 6–12 months? - Global readiness

Products designed for broad appeal and compliance can move more seamlessly across markets, making them natural anchors for consolidation.

Ask yourself: Are these products ready for international expansion, or will compliance and positioning slow us down?

Focus, Not Consolidation

Not every strategic move in the past two years has been about getting bigger. In fact, some of the most telling developments have been about companies deliberately narrowing their scope. Under mounting economic and operational pressures, leaders are choosing to focus on the markets and portfolios where they hold the greatest strength—rather than stretching resources across geographies or categories that no longer fit.

- Natura &Co consolidated Avon’s Latin American markets into its own Natura operations, while divesting Avon businesses in Europe, Africa, Asia and Central America. This move underscored Latin America as the company’s anchor region and reflected its strategy of concentrating resources where brand equity and distributor strength are greatest.

- ACN has taken this approach even further. Over the past several years, the company has fully divested its international operations and now operates exclusively in the US and Canada. By the end of 2024, ACN had exited every other market worldwide. Today, 32 years after its founding, ACN remains profitable and growing, with the founders still at the helm and focused on building a stronger business in its two core geographies.

In a year dominated by consolidation headlines, these examples remind us that sometimes the boldest decision isn’t to acquire, but to double down on core strengths. Focus, like scale, can be a path to resilience—and in some cases, it may be the more sustainable one.

STUART JOHNSON has served the direct selling industry for nearly 40 years. His passion for the channel encompasses a broader commitment to build and connect the direct selling community through exclusive industry events such as Direct Selling University and the DSN Global Celebration. Stuart is arguably the most connected person in direct selling, building and growing a network of executives, thought leaders, strategists and innovators. His advice and counsel are sought after by leaders throughout the channel.

An Online Exclusive from Direct Selling News magazine.