-

February 2026

Brought to you by Direct Selling Capital Advisors

Brought to you by Direct Selling Capital AdvisorsDirect Selling Index Mirrors the DJIA for the Month of February 2026

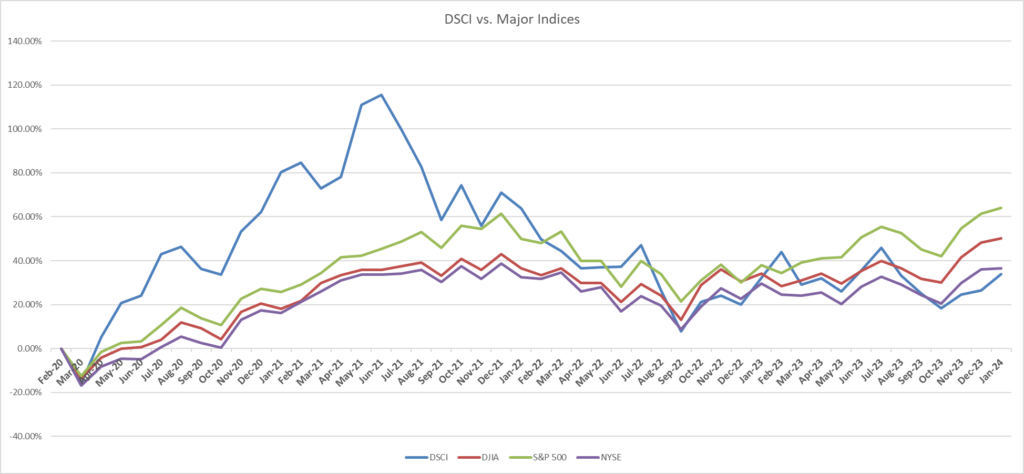

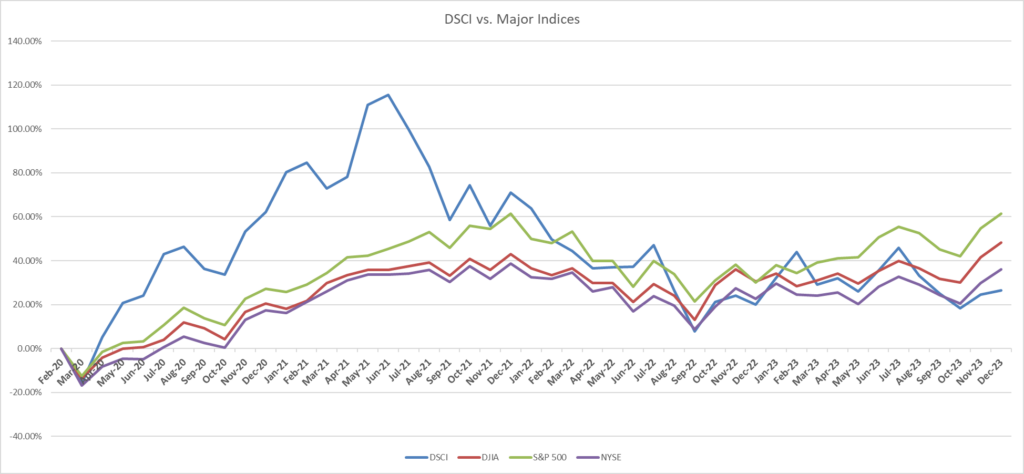

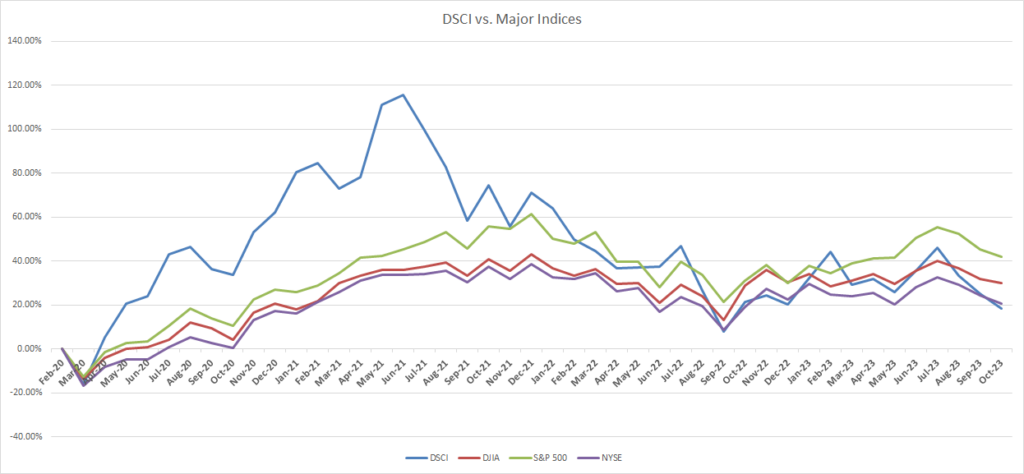

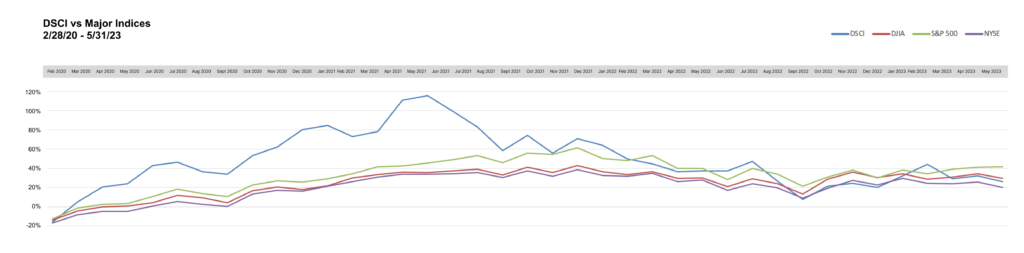

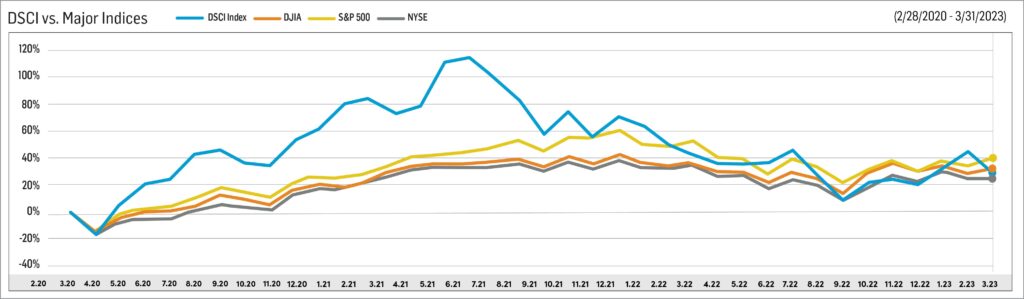

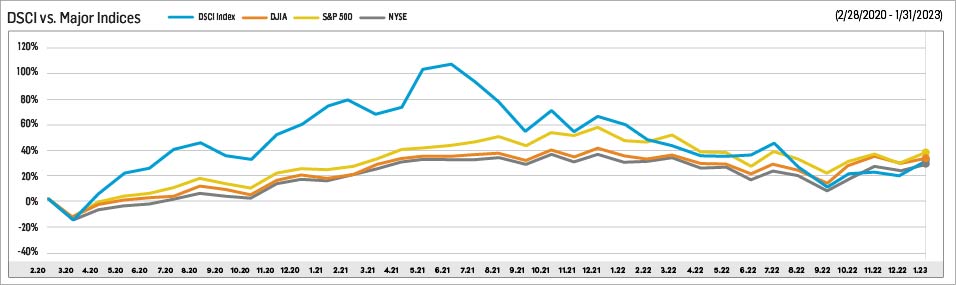

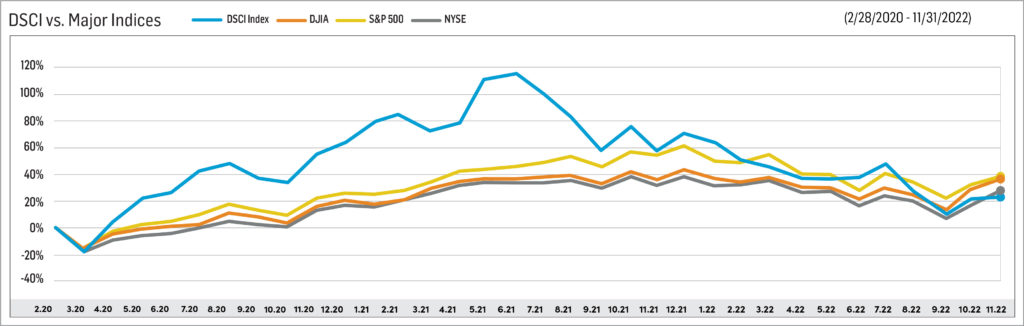

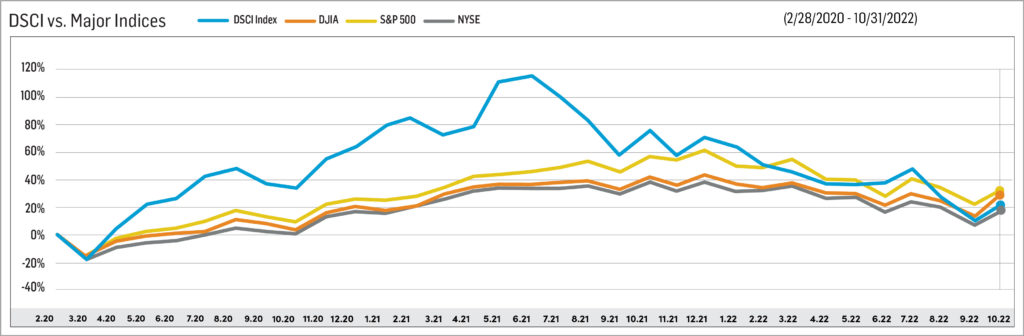

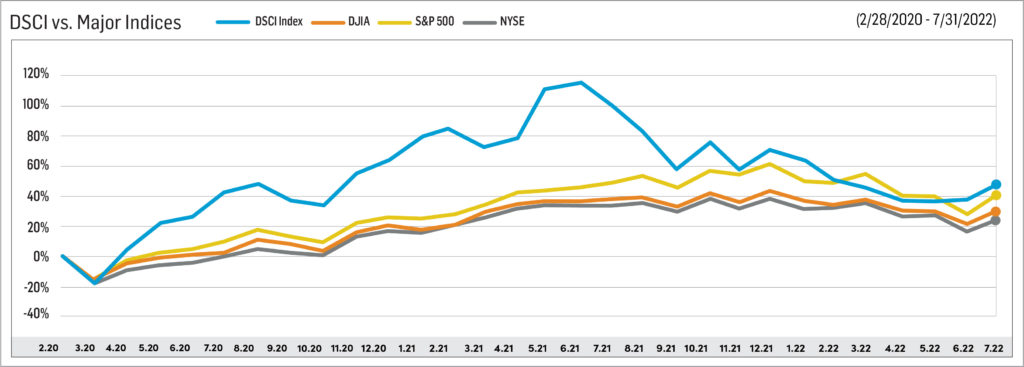

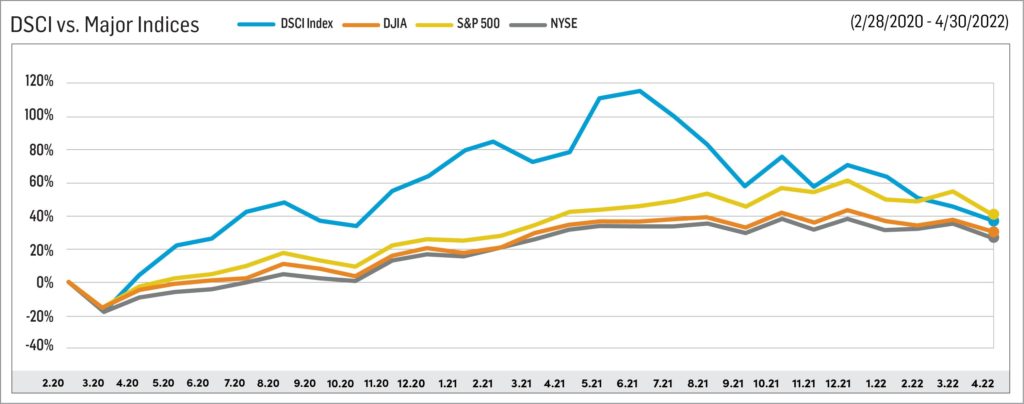

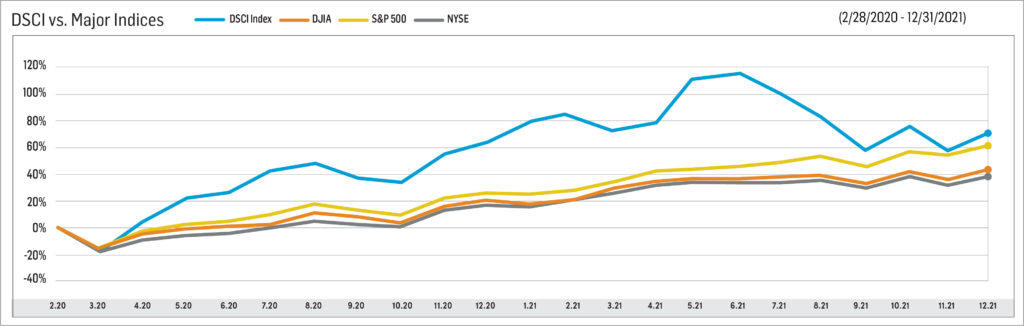

The Direct Selling Capital Advisors Direct Selling Index (DSCI) increased by 0.2% in February 2026 compared to January, closely tracking the performance of the Dow Jones Industrial Average (DJIA), which rose 0.4% over the same period.

Over the first two months of 2026, the DSCI has recorded a modest gain of 1.9%, reflecting generally stable performance among publicly traded direct selling companies despite ongoing macroeconomic uncertainty.

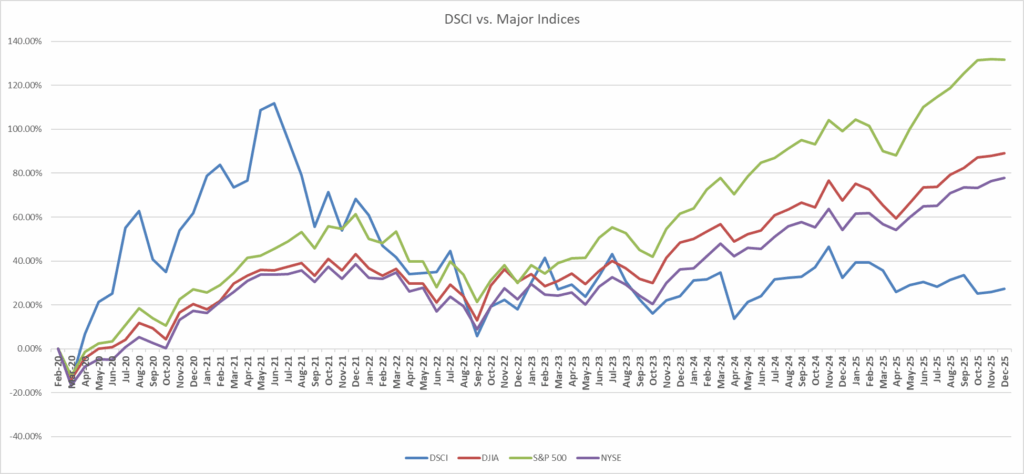

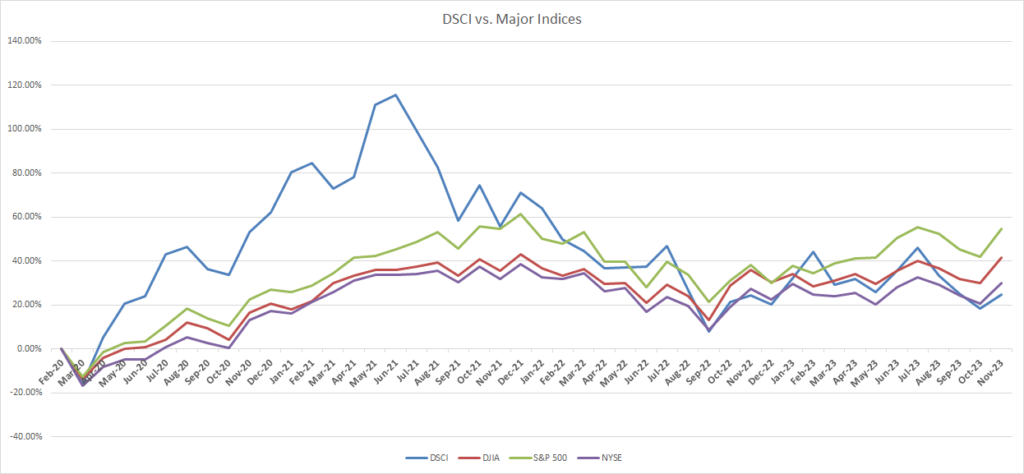

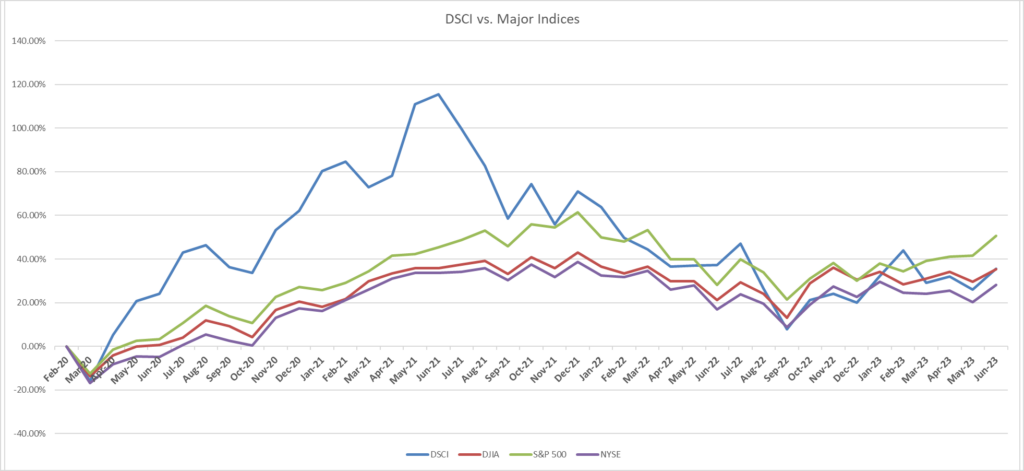

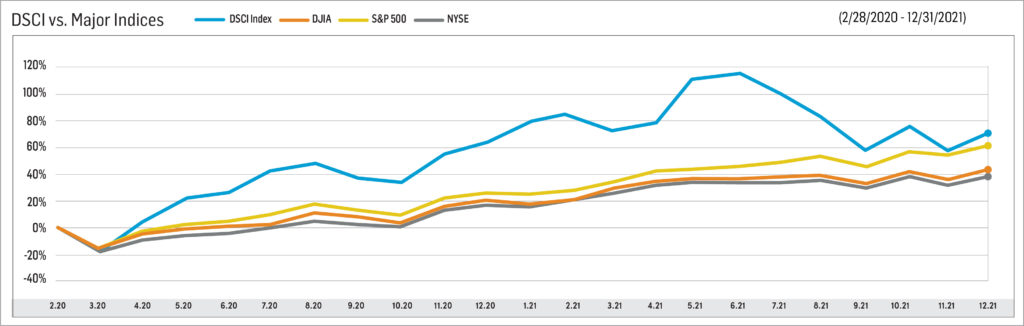

Since its inception, the DSCI has generated a cumulative return of 92.8%, underscoring the long-term resilience and growth potential of the direct selling sector relative to broader equity markets.

Market and Economic Environment

US equity markets experienced increased volatility during February 2026 as investors navigated a complex macroeconomic environment shaped by geopolitical tensions, persistent inflation concerns and mixed economic data. While major indices fluctuated throughout the month, markets broadly reflected cautious sentiment as investors reassessed expectations for monetary policy and global economic stability. Rising energy prices and geopolitical developments in the Middle East contributed to heightened market uncertainty and increased volatility across equity and commodity markets.

Economic data released during February suggested a gradually softening labor market alongside ongoing inflation pressures. The US economy unexpectedly lost approximately 92,000 jobs during the month, pushing the unemployment rate higher and raising concerns about slowing economic momentum. At the same time, elevated oil prices and supply disruptions increased inflation risks, complicating the Federal Reserve’s policy outlook and potentially delaying anticipated interest rate cuts.

Fixed income markets reflected this uncertainty as Treasury yields and mortgage rates fluctuated in response to shifting expectations regarding inflation and monetary policy. Although borrowing costs remain below the highs seen in 2023, interest rates continued to reflect caution among policymakers as they balance inflation control with signs of weakening employment growth.

Investor sentiment remained selective throughout February, with market participants favoring companies demonstrating resilient earnings, disciplined cost structures and strong balance sheets. At the same time, geopolitical risks and energy price volatility contributed to concerns about potential stagflation scenarios, reinforcing a more defensive investment posture across global markets.

Direct Selling Industry Developments

The direct selling industry continued to demonstrate structural resilience during February 2026 despite broader macroeconomic uncertainty. Consumer demand within core categories—including wellness, nutrition and personal care—remained relatively stable as companies continued to adapt their business models to evolving market conditions.

Industry research and commentary during the month highlighted a growing divergence in performance among direct selling companies. According to industry surveys and analysis, approximately half of mid- to large-sized direct selling companies reported year-over-year growth, while the remaining companies experienced declining revenues, illustrating an increasingly competitive and fragmented operating environment.

Companies achieving the strongest performance were typically those investing in digital infrastructure, modern compensation structures and enhanced distributor engagement strategies. The continued integration of mobile commerce tools, social commerce platforms and data-driven field support solutions has emerged as a critical factor supporting distributor productivity and customer retention.

Technology-enabled transformation therefore remained a defining theme across the sector. Companies increasingly focused on blending traditional direct selling models with digital commerce capabilities, enabling more flexible customer acquisition and strengthening omnichannel engagement strategies.

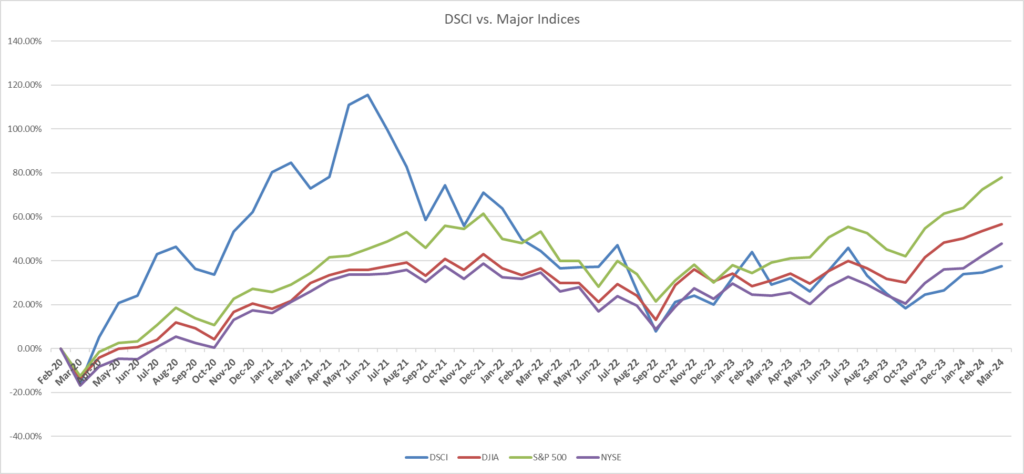

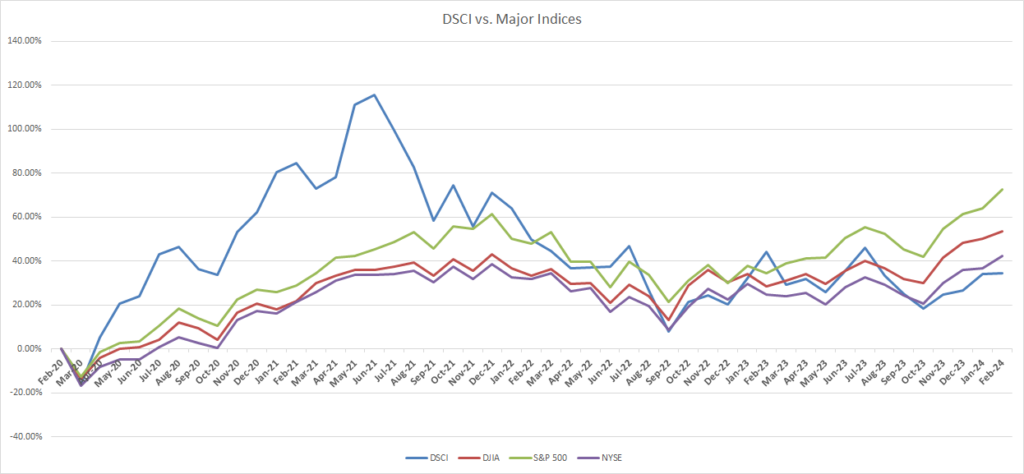

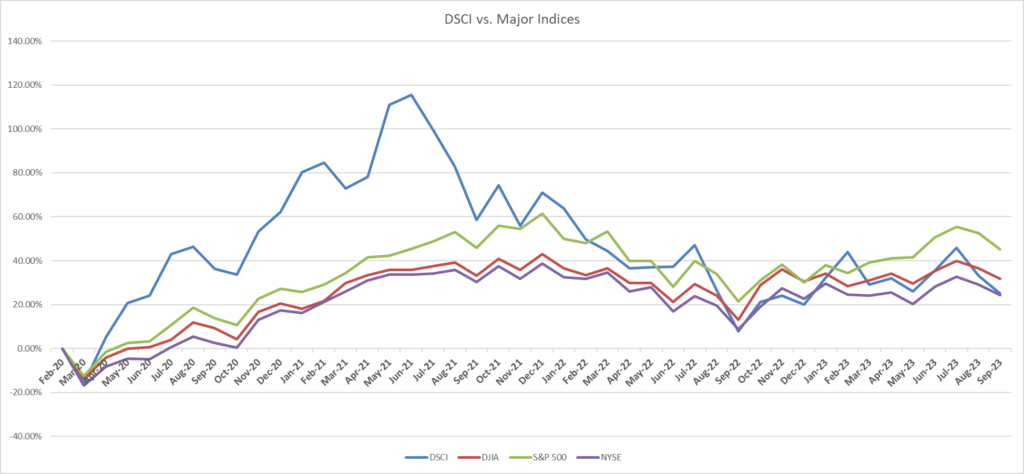

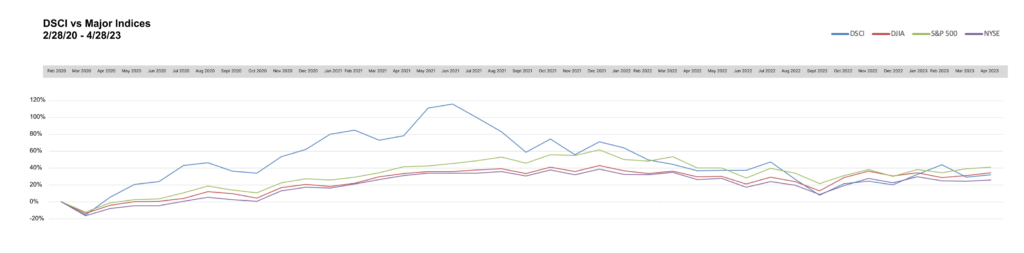

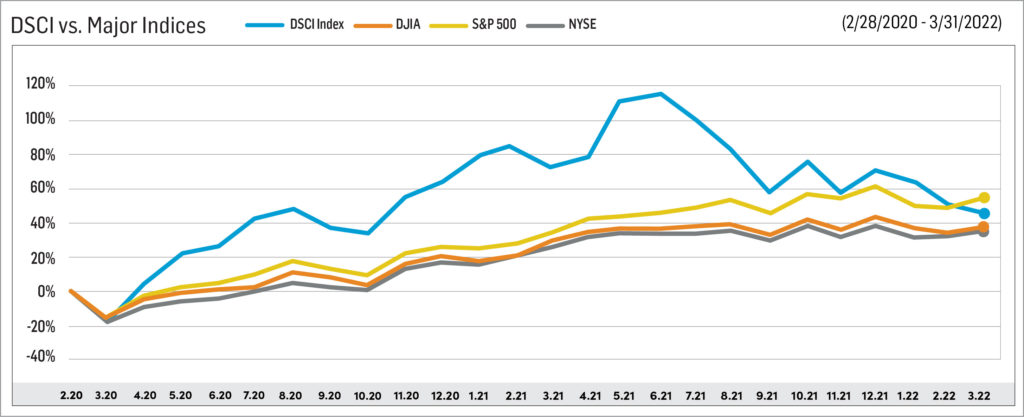

Direct Selling Capital Advisors Index (DSCI)

The Direct Selling Capital Advisors Index (DSCI) recorded modest gains during February, broadly mirroring the performance of major US equity benchmarks. While volatility increased across global markets, several large-cap direct selling companies demonstrated relatively stable trading patterns, supported by ongoing operational improvements and improving investor sentiment toward companies showing progress in earnings visibility and balance sheet management.

Compared with broader equity indices, the DSCI continued to display relatively moderate volatility during periods of market stress. This stability reflects the defensive characteristics often associated with the sector, particularly among companies operating in consumer wellness and personal care categories.

Since its inception, the DSCI continues to demonstrate strong cumulative performance relative to traditional benchmarks, underscoring the long-term growth potential of publicly traded direct selling companies despite cyclical market pressures.

Looking Forward—Strategic Outlook

As the first quarter of 2026 progresses, the direct selling sector continues to face a dynamic combination of macroeconomic challenges and strategic opportunities. Several key themes are likely to influence industry performance in the months ahead:

Macroeconomic sensitivity: Consumer spending trends may face pressure from higher energy costs, labor market softness and continued inflation uncertainty.

Digital and omnichannel transformation: Companies investing in social commerce, mobile ordering platforms and digital distributor tools are likely to maintain a competitive advantage.

Operational efficiency and cost discipline: Continued focus on margin management and supply chain optimization will remain critical as companies navigate economic volatility.

Strategic differentiation: Firms successfully balancing traditional distributor networks with modern ecommerce and digital engagement strategies are expected to outperform peers.

Overall, February 2026 highlighted a more uncertain macroeconomic environment compared with the start of the year. Nevertheless, the direct selling sector continues to demonstrate resilience through adaptable business models, expanding digital capabilities and consistent demand across core consumer product categories.

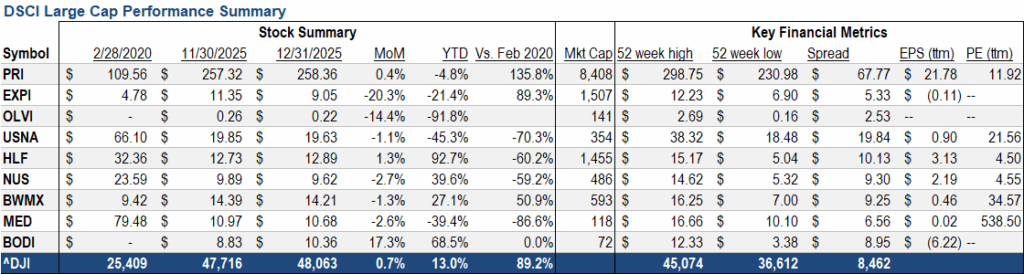

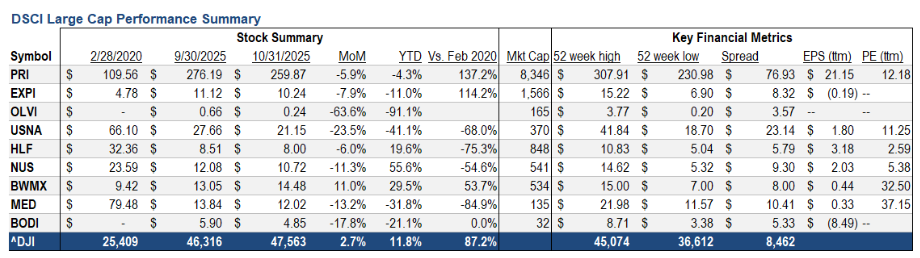

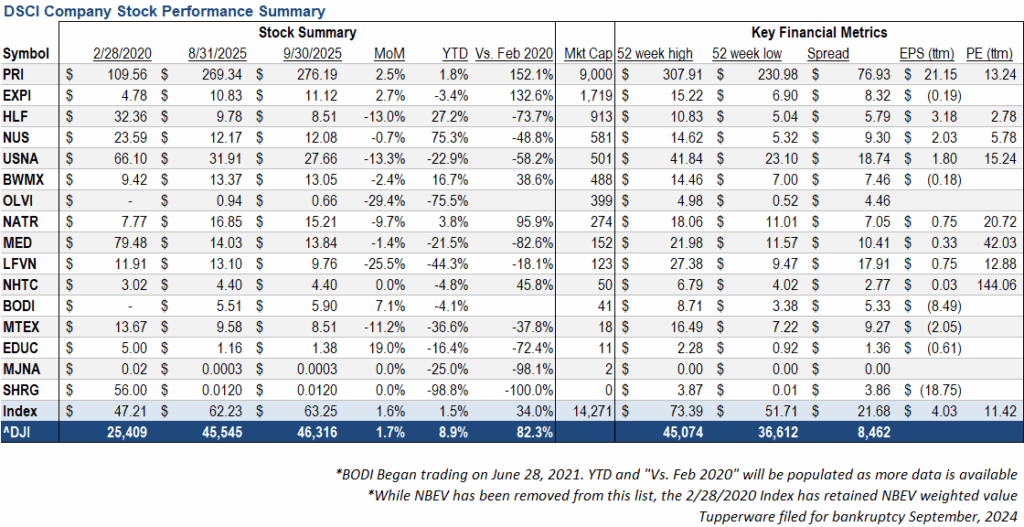

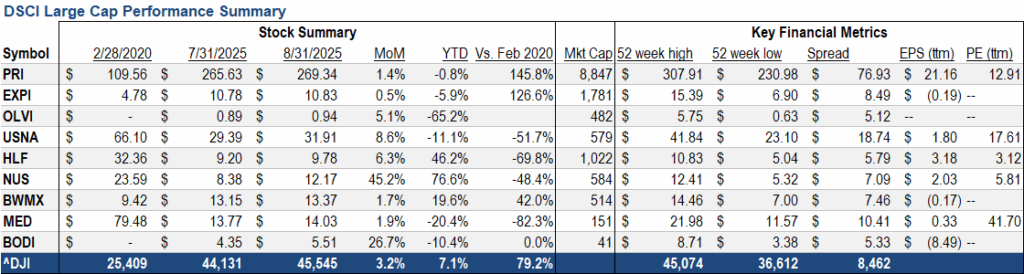

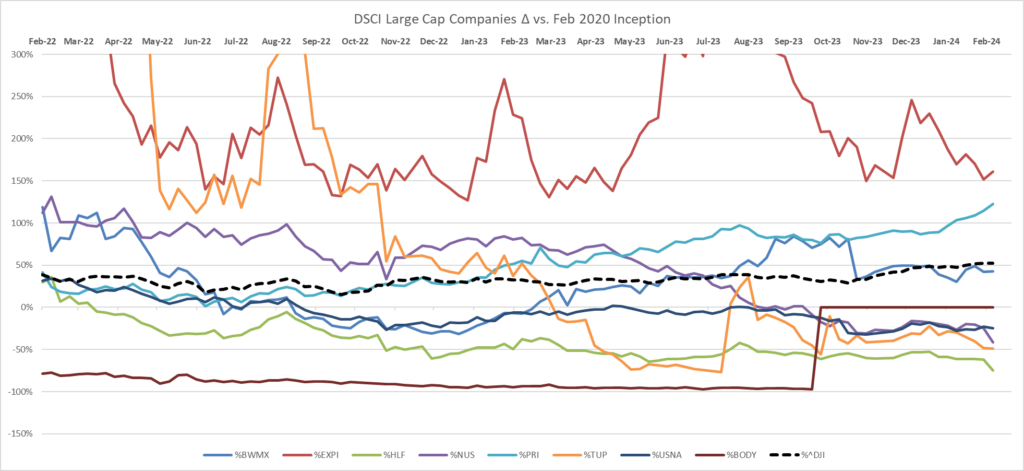

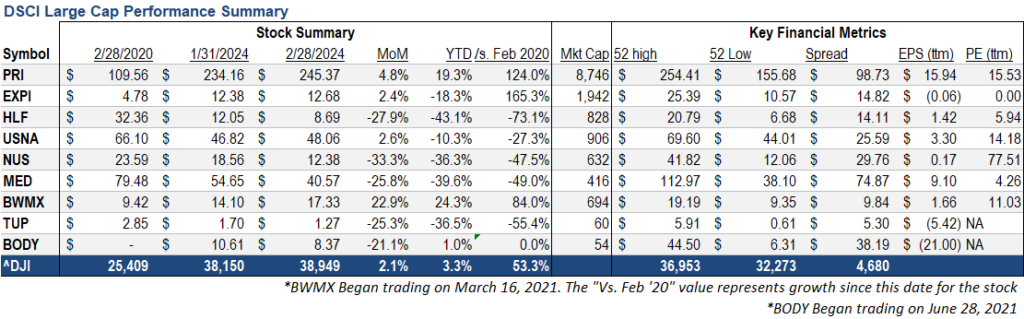

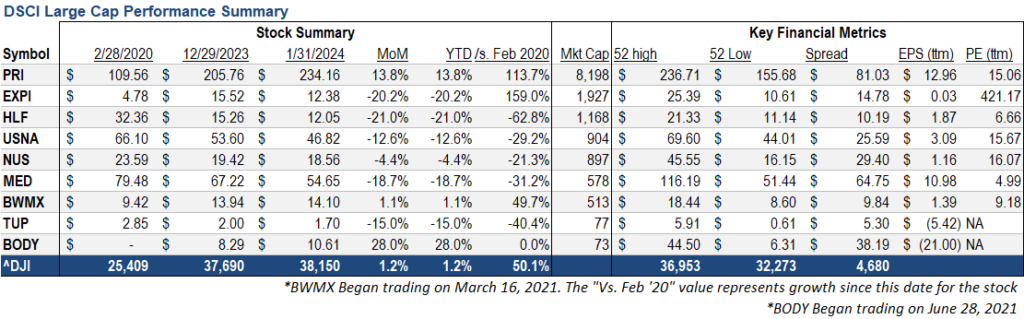

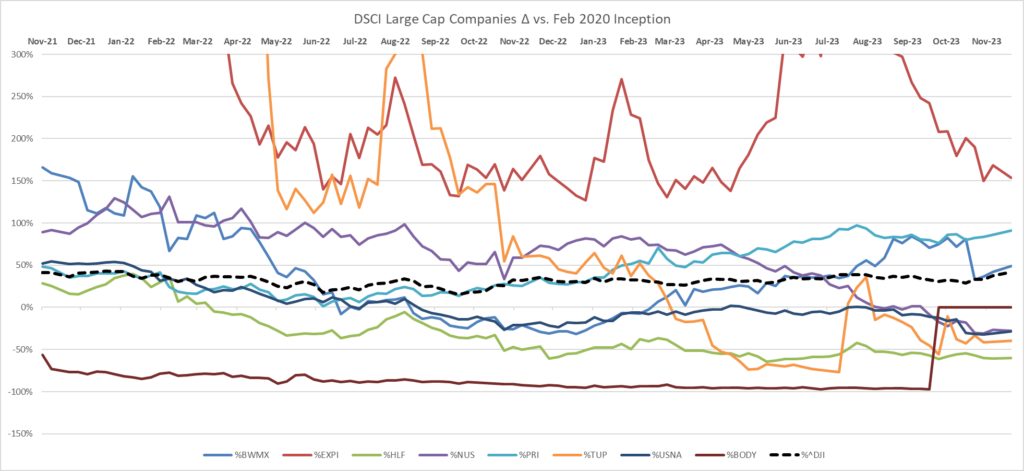

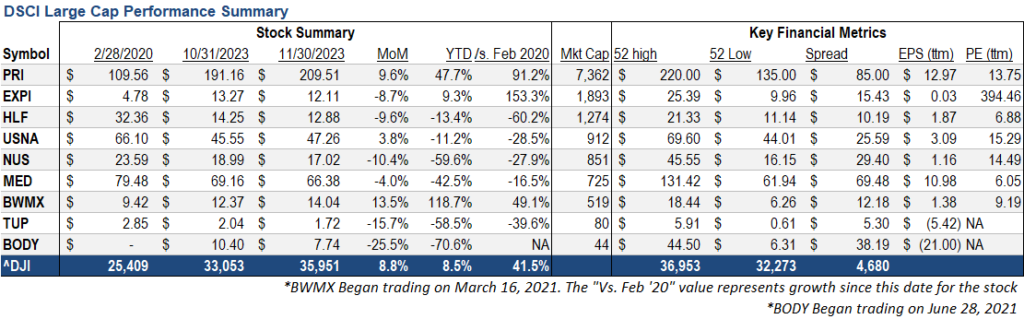

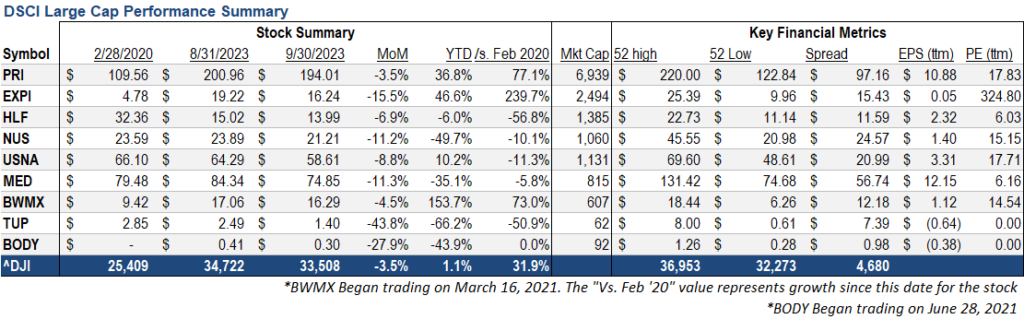

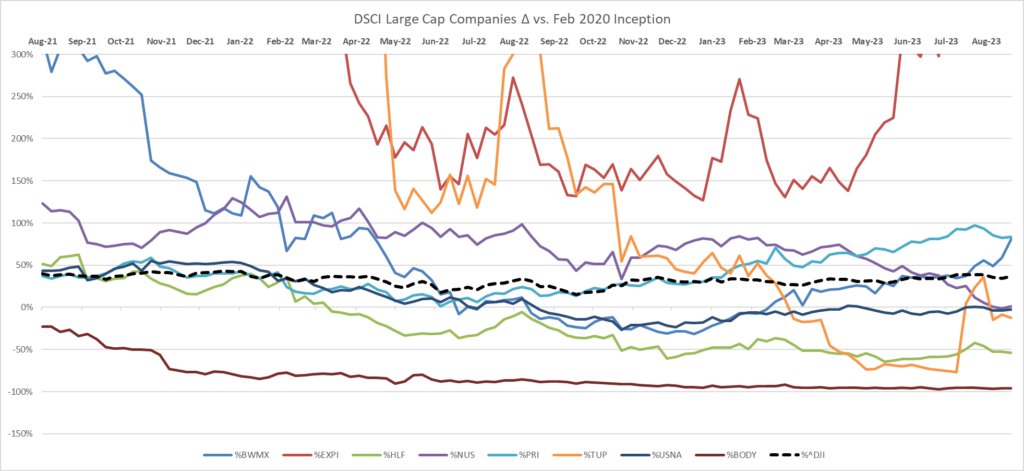

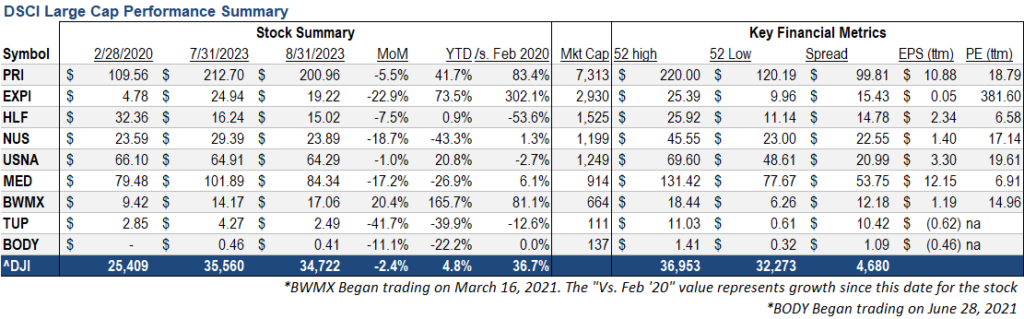

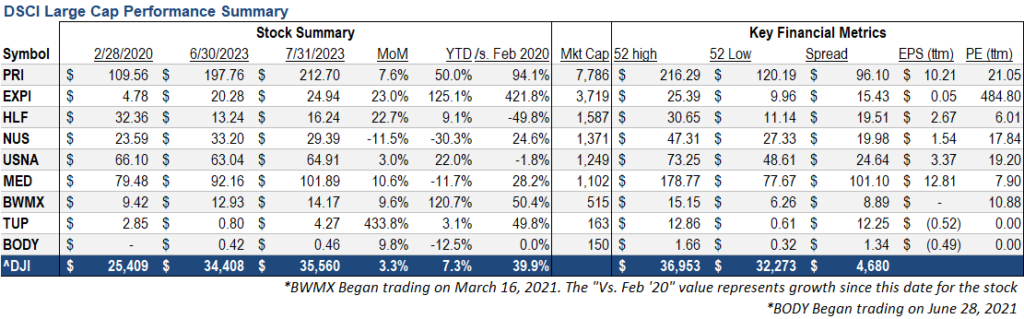

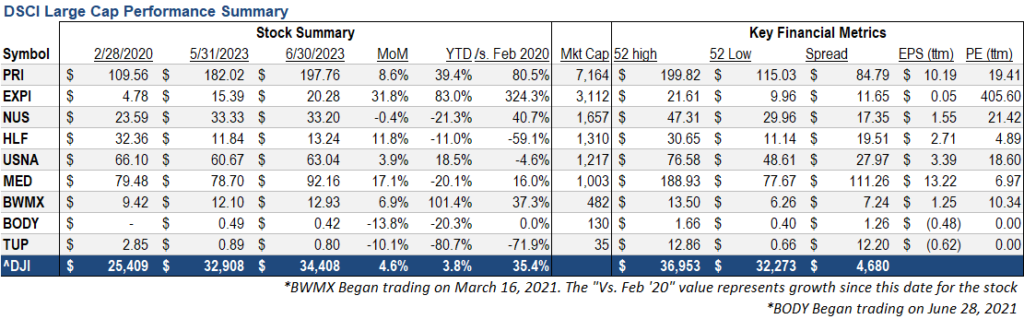

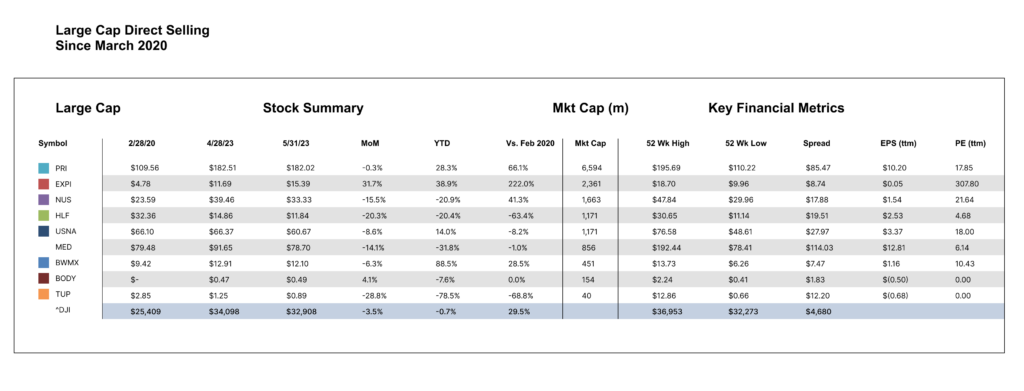

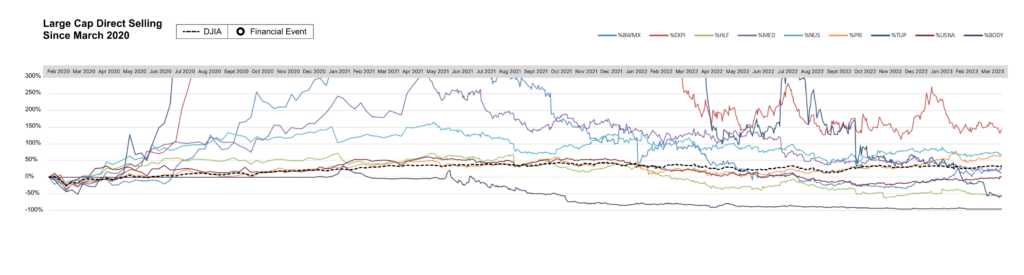

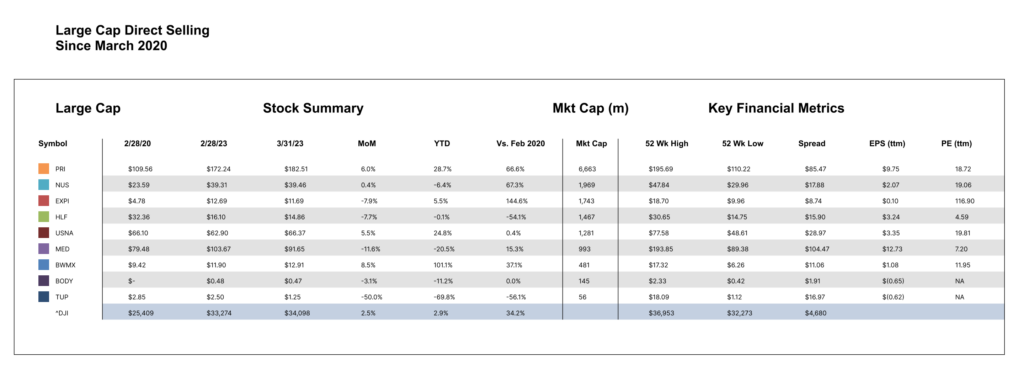

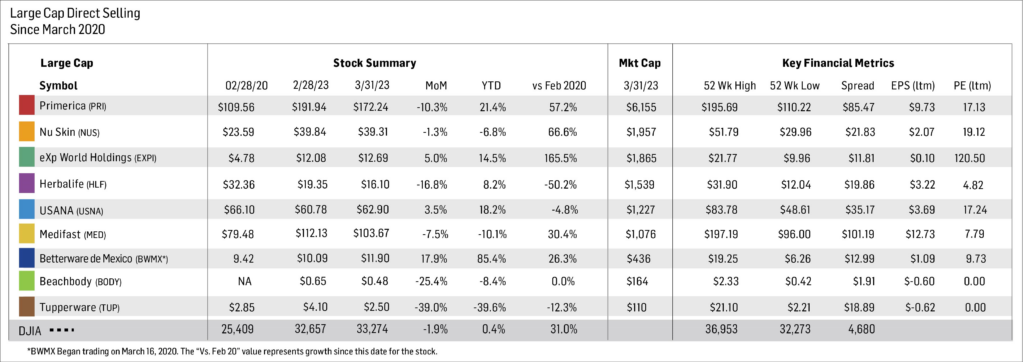

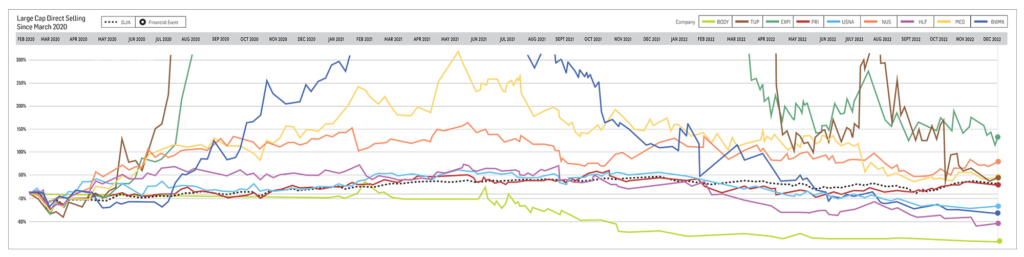

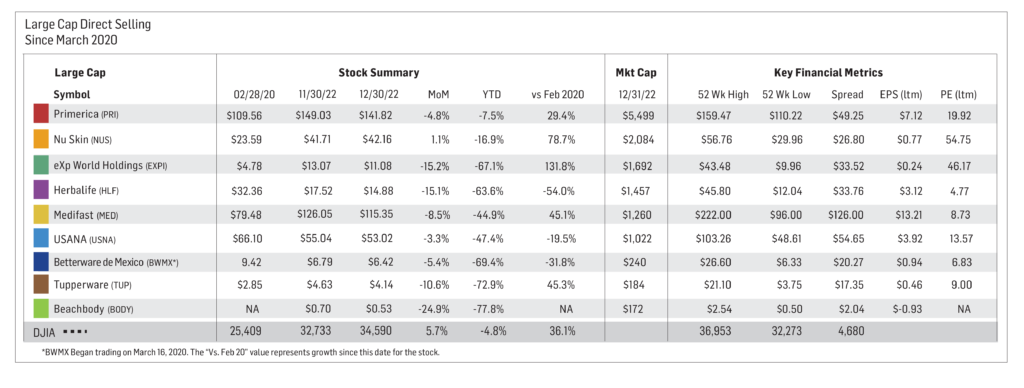

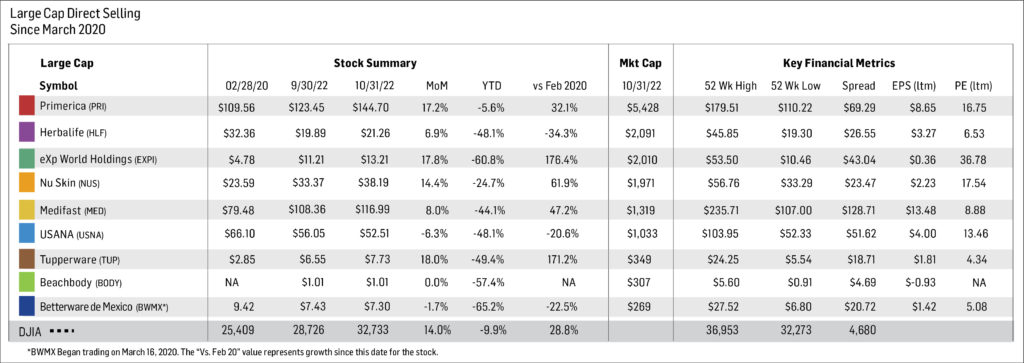

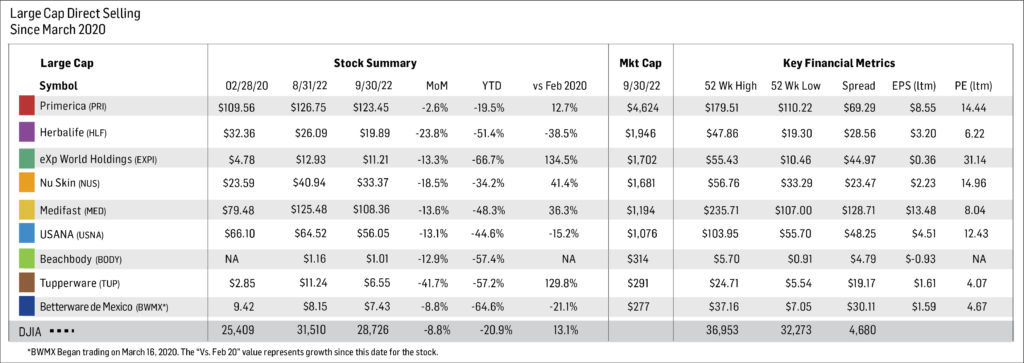

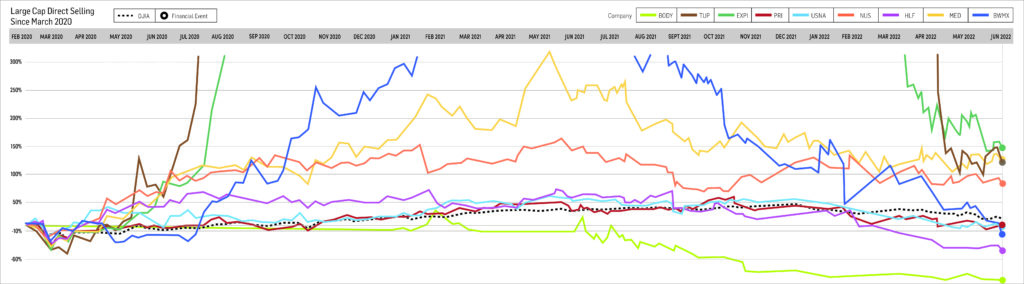

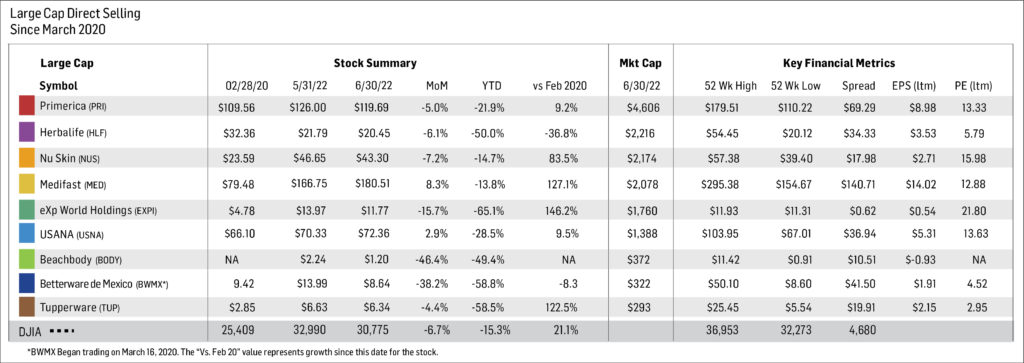

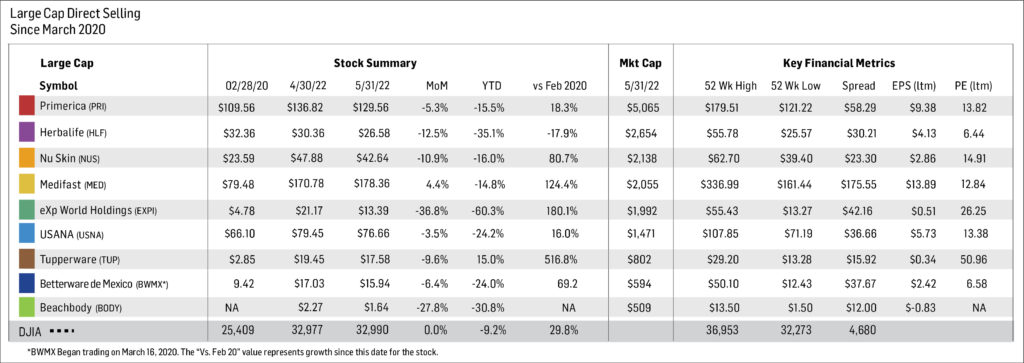

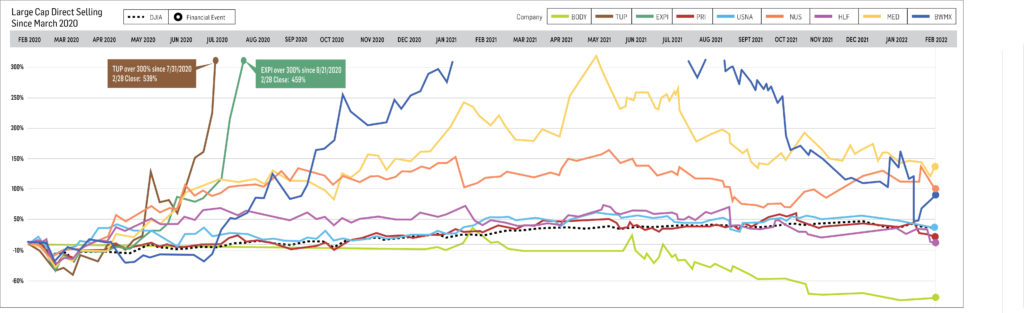

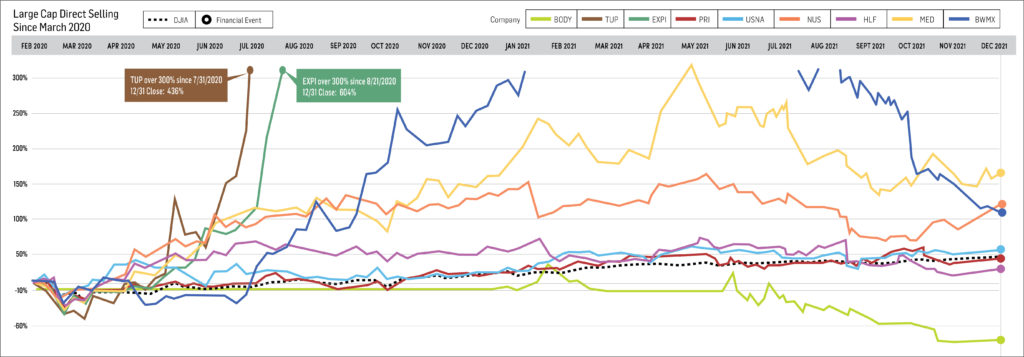

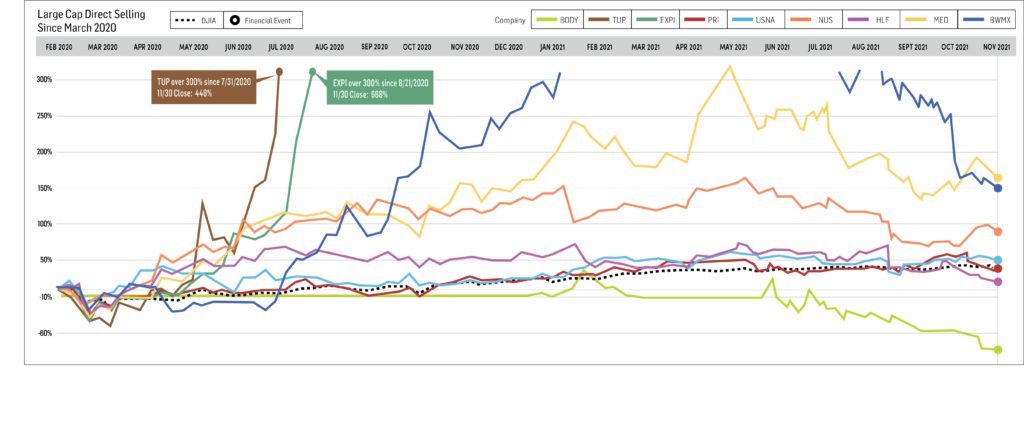

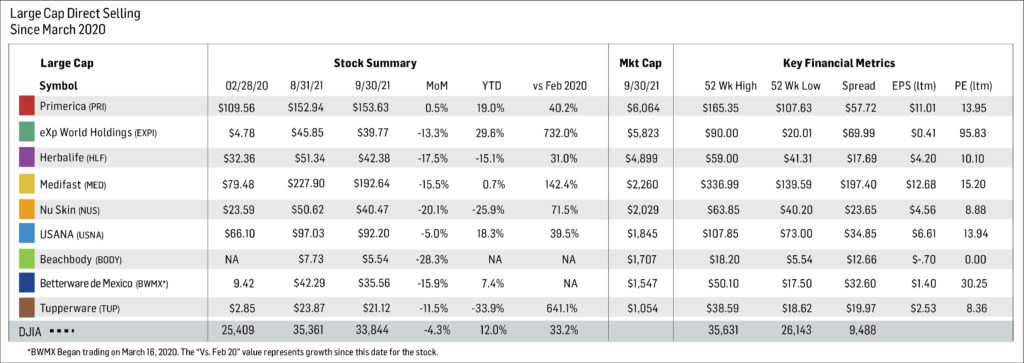

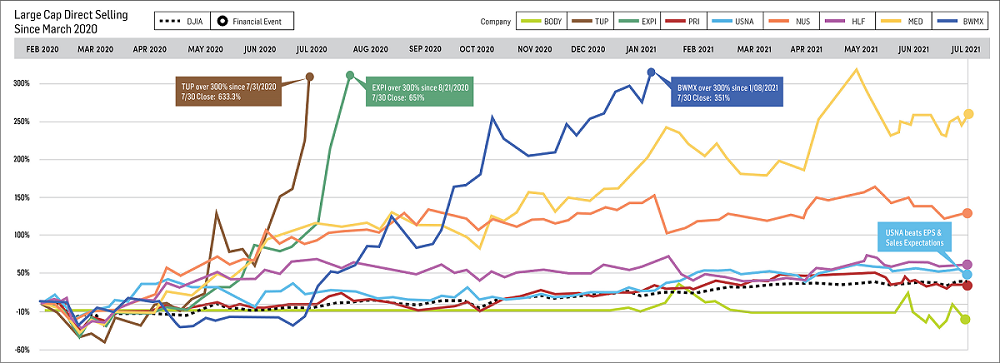

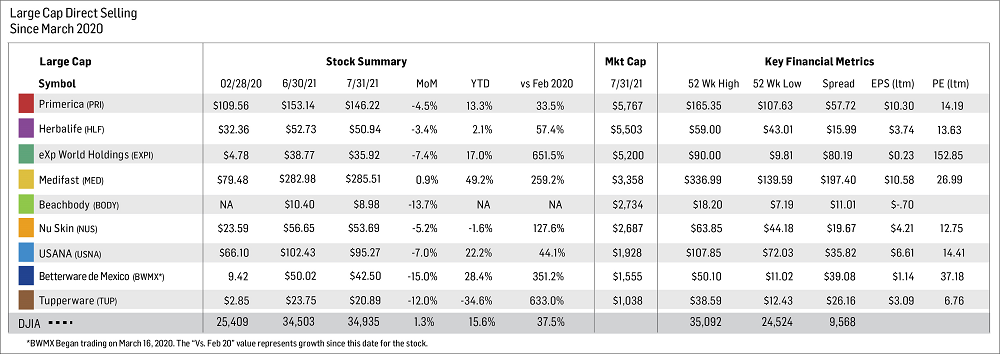

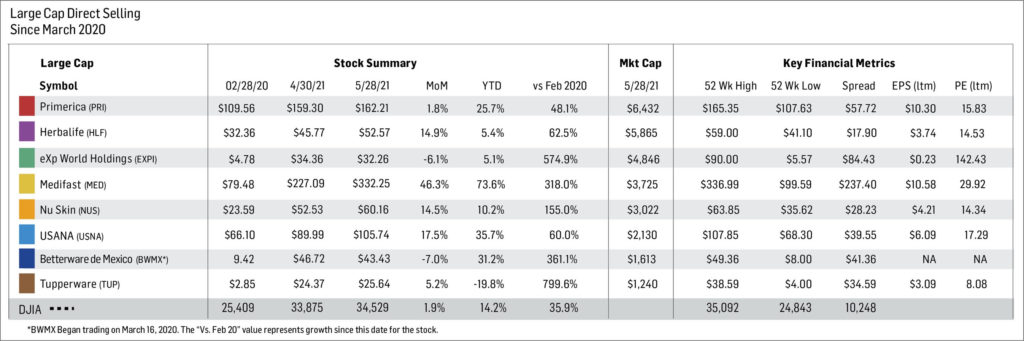

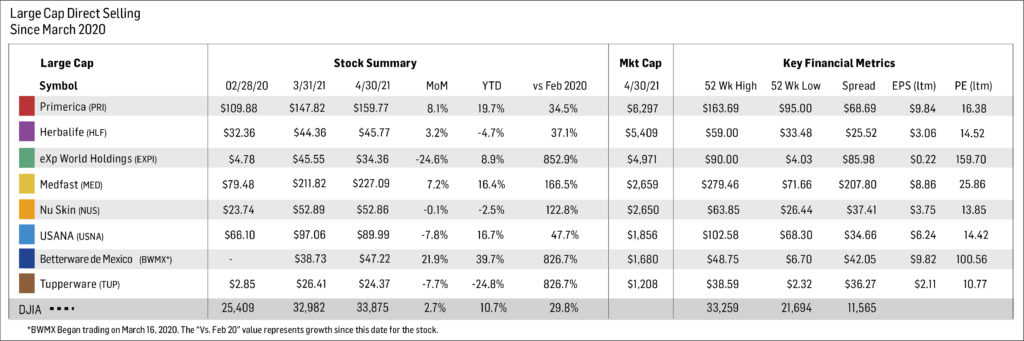

Large Cap

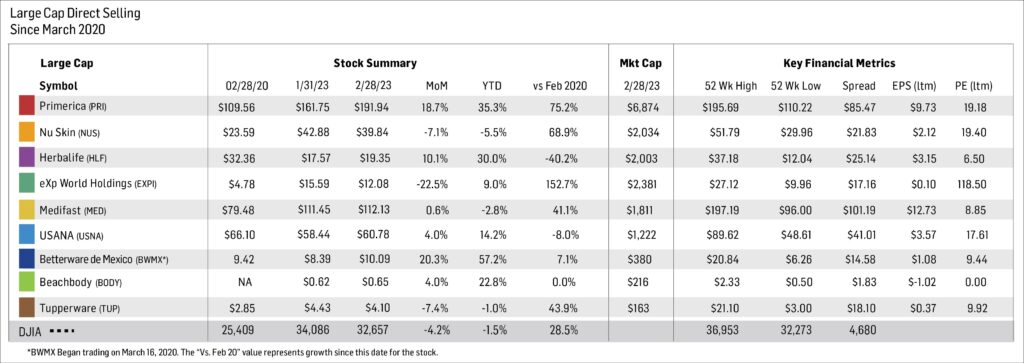

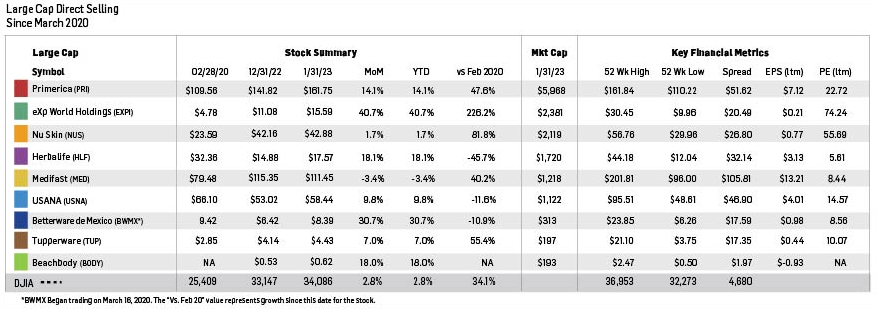

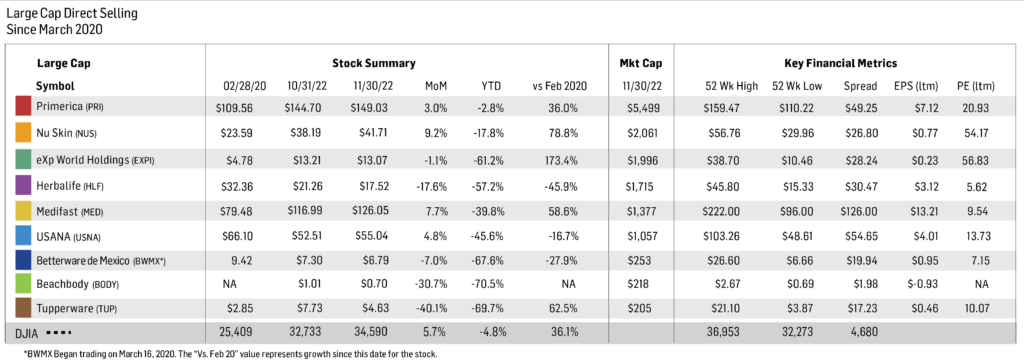

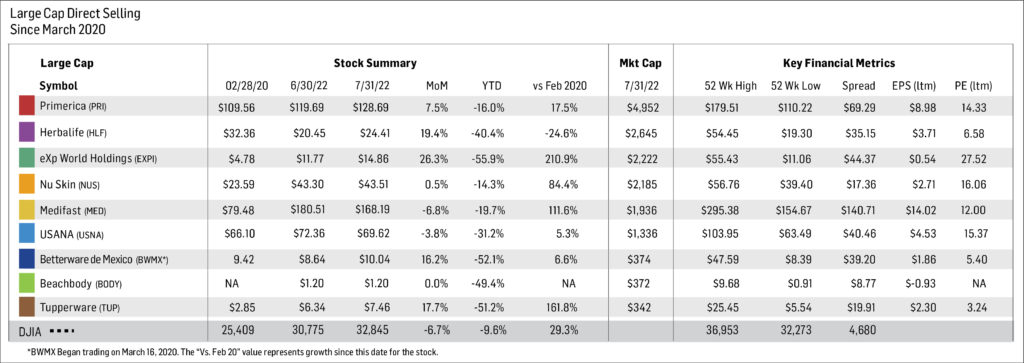

Note: For the purposes of this report, Direct Selling Capital considers companies with a market capitalization more than $1 billion “Large Cap.”

Betterware de Mexico (NASDAQ: BWMX), founded in 1995, is the leading direct-to-consumer company in Mexico focused on innovative products related to household organization, practicality, space-saving and hygiene. Through the acquisition of JAFRA on April 7, 2022, the company expanded into the beauty market in Mexico and the US, offering fragrances, color cosmetics, skincare and toiletries. The combined business operates an asset-light model with low capital expenditure, consistent profitability, double-digit revenue growth and strong free cash flow generation. Today, Betterware distributes its products in both Mexico and the United States.

In February 2026, Betterware’s stock declined by 7.7% compared to January, bringing its year-to-date performance to 16.6%. Since the inception of the DSCI, the stock remains up 75.9%. At month-end, BWMX had a market capitalization of approximately $652 million and traded in a 52-week range of $7.00 to $19.79.

February activity was driven by the company’s fourth-quarter 2025 results and subsequent dividend announcement. BeFra reported steady operating progress, ongoing debt reduction and continued strategic expansion efforts, while also announcing that shareholders approved an aggregate dividend payment of MXN 200 million at the February 20, 2026 meeting. While the share price softened during the month, the company’s continued focus on free cash flow, shareholder returns and regional growth remains constructive for the medium-term outlook.

The February decline appears more consistent with profit-taking after the strong January rally than with any major deterioration in fundamentals. Investors will likely remain focused on execution in Mexico, JAFRA integration benefits and the pace of geographic expansion across Latin America.

Nu Skin Enterprises, Inc. (NYSE: NUS), together with its subsidiaries, engages in the development and distribution of various beauty and wellness products worldwide. It offers skincare devices, cosmetics and other personal care products, including ageLOC LumiSpa and ageLOC LumiSpa iO; and nutrition skincare products. The company also provides wellness products, such as LifePak nutritional supplements, ageLOC TR90 weight management system and Beauty Focus Collagen+. In addition, it is involved in the research and product development of skincare products and nutritional supplements. The company sells its products under the Nu Skin, Pharmanex and ageLOC brands through retail stores, website, digital platforms and independent direct sellers and marketers, as well as a service center. Nu Skin Enterprises, Inc. was founded in 1984 and is headquartered in Provo, Utah.

In February 2026, Nu Skin’s stock declined by 20.1% compared to January, reducing year-to-date performance to -11.9%. Since the DSCI’s inception, the shares remain down 64.1%. At the end of February, the stock traded in a 52-week range of $5.32 to $14.62, with a market capitalization of approximately $373 million.

February sentiment was pressured despite continued shareholder returns. Nu Skin announced that its board declared a quarterly cash dividend of $0.06 per share, payable in March. At the same time, investor focus remained on earnings quality, currency headwinds and the company’s need to translate product innovation and market expansion into more consistent revenue stabilization. Yahoo Finance coverage of the company’s fourth-quarter earnings highlighted 51% EPS growth and management’s plans for global expansion, but those positives were not enough to offset the market’s cautious stance during the month.

While Nu Skin continues to promote long-term catalysts such as new device rollouts and geographic expansion, February’s share-price weakness indicates that investors still want clearer evidence of sustainable top-line recovery. The balance between innovation, field productivity, and margin preservation will remain central to the stock’s trajectory in coming quarters.

Herbalife Nutrition, Inc. (NYSE: HLF) provides health and wellness products across North America, Latin America, EMEA, China and Asia Pacific. The company offers products in the areas of weight management; targeted nutrition; energy, sports and fitness; outer nutrition; and literature, promotional and other items. It also provides weight management products, including meal replacement products, protein shakes, drink mixes, weight loss supplements, healthy snacks and metabolism boosting teas; targeted nutrition products, which comprise functional beverages and dietary and nutritional supplements that contain herbs, vitamins, minerals and other natural ingredients; outer nutrition products, such as facial skin, body and hair care products; and energy, sports and fitness products, including N-R-G tea and energy drink products. In addition, it offers literature, promotional and other materials that comprise start-up kits, sales tools and educational materials. The company sells its products through sales representatives, independent service providers and company-operated retail stores and platforms. The company was formerly known as Herbalife Nutrition Ltd. and changed its name to Herbalife Ltd. in April 2023. Herbalife Ltd. was founded in 1980 and is headquartered in Los Angeles, California.

In February 2026, Herbalife’s stock increased by 13.2% compared to January, extending its year-to-date gain to 51.4%. Despite this strong recovery, the shares remain down 39.7% since the establishment of the DSCI in February 2020. As of month-end, Herbalife had a market capitalization of approximately $1.71 billion and traded within a 52-week range of $6.20 to $20.40.

The February rally was supported by stronger fourth-quarter and full-year 2025 results. Herbalife reported fourth-quarter net sales growth of 6.3% to approximately $1.3 billion, adjusted EBITDA of $156.1 million, and diluted EPS of $0.81. Management noted continued debt reduction, improving sales trends and strategic emphasis on product innovation and a more digitally enabled distributor experience. The company also disclosed that Cristiano Ronaldo invested $7.5 million in Herbalife’s Pro2col technology platform, highlighting continued commitment to digital engagement tools that could improve distributor productivity and customer retention.

Herbalife’s strong February performance suggests investors are increasingly rewarding operational stabilization, improving financial discipline, and digital transformation initiatives. Although volatility is likely to remain elevated, the company entered March with improving momentum and a meaningfully better sentiment profile than a year ago.

Medifast, Inc. (NYSE: MED), through its subsidiaries, operates as a health and wellness company offering habit-based, coach-guided lifestyle solutions focused on weight management and obesity support in the United States. The company’s flagship brand, OPTAVIA, delivers clinically-supported weight loss programs, GLP-1 support plans and a wide variety of food products—such as bars, shakes, soups, cereals and snacks—complemented by one-on-one coaching, digital tools and community support. Medifast was founded in 1980 and is headquartered in Baltimore, Maryland. Its products are sold via point-of-sale transactions and ecommerce.

In February 2026, Medifast shares declined by 8.0% compared to January, bringing year-to-date performance to -1.4%. Since the inception of the DSCI, the stock has fallen 86.8%, making it one of the weakest long-term performers in the index. At month-end, MED had a market capitalization of approximately $117 million and traded within a 52-week range of $10.10 to $15.46.

February developments were dominated by the company’s fourth-quarter and full-year 2025 results. Direct Selling News reported fourth-quarter revenue of $75.1 million and full-year revenue of $385.8 million, while the company ended the year with $167.3 million in cash, cash equivalents and investment securities and no interest-bearing debt. Management guided first-quarter 2026 revenue to a range of $65 million to $80 million, reflecting continued top-line pressure. Investors responded somewhat positively to revenue coming in ahead of expectations, but concerns remain around coach productivity, profitability and the pace of the company’s transformation.

Overall, Medifast remains a higher-risk turnaround story. The balance sheet is still a key strength, but sustained revenue declines and structural pressure from the evolving weight-management market continue to weigh on sentiment. Investors will likely need clearer evidence of stabilization before assigning a more constructive valuation.

USANA Health Sciences, Inc. (NYSE: USNA) develops, manufactures and sells science-based nutritional, personal care and skincare products across Asia Pacific, the Americas and Europe. The company operates through two segments: Direct Selling and Hiya Direct-To-Consumer. Its product lineup includes USANA Nutritional Optimizers for cardiovascular, skeletal and digestive health; Essentials/CellSentials—vitamin and mineral supplements for all ages beginning at 13 months; and food products such as meal replacement shakes and snack bars for healthy weight management, digestive health and hydration. USANA also offers the Celavive skincare line tailored for various skin types and ethnicities, as well as online tools and business materials for associates. Products are sold through retail, subscription-based models and direct selling. The company holds research collaboration agreements with the Beijing University of Chinese Medicine and the National Sports Training Bureau. USANA was founded in 1992 and is headquartered in Salt Lake City, Utah.

In February 2026, USANA’s stock declined by 0.8% compared to January, though year-to-date performance remained positive at 9.6%. Since the inception of the DSCI, the shares are down 67.4%. At month-end, USANA had a market capitalization of approximately $347 million and traded in a 52-week range of $18.48 to $38.32.

February trading was shaped by the company’s fourth-quarter and full-year 2025 financial results. According to Direct Selling News, fiscal 2025 net sales reached $925 million, up 8% year-over-year, while net earnings totaled $10.8 million with diluted EPS of $0.58 and adjusted EBITDA of $101.3 million. USANA’s fourth-quarter results came in roughly in line with revenue, while full-year guidance slightly exceeded analyst expectations. Management continues to position product innovation, global brand development and omnichannel diversification as key priorities entering 2026.

Although the stock was relatively stable in February, investor sentiment remains measured. The company’s debt-free balance sheet and improving revenue base are positives, but execution risk remains around distributor engagement, inventory management and the pace at which direct-to-consumer initiatives can supplement the core business.

eXp World Holdings, Inc. (NASDAQ: EXPI) together with its subsidiaries, provides cloud-based real estate brokerage services for residential homeowners and homebuyers. The company operates through three segments: North American Realty, International Realty and Other Affiliated Services. It acts as a licensed broker for processing residential and commercial real estate transactions and provides other real estate support services. In addition, the company offers FrameVR.io, a web-accessible proprietary technology providing immersive 3D platforms; SUCCESS magazine and its related media properties, which offer training, classes, resources and tools under the SUCCESS brand; and SUCCESS Space, a coworking solution that provides rental workspaces, professional development coaching, media production services, virtual-world communications technology and full-service cafes.

The company operates primarily in North America, Canada, the United Kingdom, Australia, South Africa, India, Mexico, Portugal, France, Brazil, Italy, Hong Kong, Colombia, Spain, Israel, Panama, Germany, the Dominican Republic, Greece, New Zealand, Chile, Poland, Dubai and has expanded into Japan, Romania and The Netherlands, with additional international markets across Europe and Asia. eXp World Holdings, Inc. was formerly known as eXp Realty International Corporation and changed its name in May 2016. The company was incorporated in 2008 and is headquartered in Bellingham, Washington.

In February 2026, eXp’s stock price declined by 22.9% compared to January, bringing year-to-date performance to -23.0%. Despite the sharp monthly decline, the stock remains up 45.8% since the inception of the DSCI. At the end of February, eXp had a market capitalization of approximately $1.10 billion and traded in a 52-week range of $6.68 to $12.23.

Investor sentiment in February was influenced by the company’s fourth-quarter and full-year 2025 earnings release. eXp reported quarterly revenue of approximately $1.19 billion, while full-year revenue reached $4.77 billion. However, the company also reported a full-year net loss of $22.7 million, or $0.14 per share, which likely contributed to the sharp reset in the share price during the month. Management’s first-quarter 2026 revenue outlook of $960 million to $980 million and full-year revenue guidance of $4.85 billion to $5.15 billion suggest continued scale, but investors appear to remain cautious on profitability and execution.

While eXp’s long-term digital brokerage model remains differentiated, February’s decline indicates the market is taking a more selective view of growth companies that have yet to demonstrate consistent earnings leverage. Near-term performance will likely depend on management’s ability to improve margins while sustaining agent productivity and international expansion.

Primerica, Inc. (NYSE: PRI), together with its subsidiaries, provides financial products and services to middle-income households in the United States and Canada. The company operates in three segments: Term Life Insurance; Investment and Savings Products; Senior Health; and Corporate and Other Distributed Products. The Term Life Insurance segment underwrites individual term life insurance products. The Investment and Savings Products segment provides mutual funds and various retirement plans, managed investments, variable and fixed annuities and fixed indexed annuities; and offers segregated funds. The Corporate and Other Distributed Products segment provides mortgage loans; prepaid legal services that assist subscribers with legal matters, such as drafting wills, living wills and powers of attorney, trial defense and motor vehicle-related matters; ID theft defense services; auto and homeowners’ insurance; home automation solutions; and insurance products, including supplemental and accidental death and disability insurance. It distributes and sells its products through licensed sales representatives. Primerica, Inc. is headquartered in Duluth, Georgia.

In February 2026, Primerica’s share price declined by 3.6% compared to January, bringing its year-to-date performance to -1.8%. Despite the modest monthly pullback, the stock remains up 131.5% since the establishment of the DSCI in February 2020. As of month-end, Primerica had a market capitalization of approximately $8.35 billion and traded in a 52-week range of $230.09 to $296.00.

February trading was shaped primarily by the company’s fourth-quarter 2025 results. Primerica reported total revenues of $853.7 million, up 15% year-over-year, with diluted adjusted operating EPS of $6.13 versus $5.03 in the prior-year period. The company also highlighted record investment and savings product sales, client asset values of $129 billion and a new $475 million share repurchase authorization through the end of 2026. These results reinforced the company’s strong operating momentum, even as the stock gave back a portion of its January gains following earnings.

Overall, Primerica remains one of the strongest long-term performers in the index. Its combination of high profitability, recurring cash generation and shareholder returns continues to support a constructive outlook, although the February decline suggests some near-term consolidation after a strong multi-year run.

Oliveda International, Inc. (OTC: OLVI) was founded in 2003 and has more than 20 years of experience in: 1) the management and organic certification of mountain olive trees; 2) the extraction of international award-winning extra virgin olive oils; 3) the extraction of hydroxytyrosol, a compound with antioxidant, anti-inflammatory and skin- and eye-protective effects; and 4) the production and distribution of cosmetic and holistic waterless products derived from the olive tree.

Oliveda International, Inc. and its subsidiaries, including Olive Tree People Inc., Olive Tree People Europe AG, Oliveda Deutschland GmbH, and Olive Tree Farmers SL, were founded by German real estate investor Thomas Lommel. The group has established a unique market position through innovations such as Olive Tree Therapy “10 years in 14 days,” olive matcha (made from ground olive leaves), and a coffee alternative based on olive leaves and hydroxytyrosol. Lommel is also active in the mindfulness sector with his olive tree sound bath meditations and the broadcast of olive tree frequencies globally.

In February 2026, Oliveda’s share price increased by 49.3% compared to January, bringing its year-to-date gain to 36.4%. As of month-end, the stock traded at $0.30, with a market capitalization of approximately $186 million and a 52-week range of $0.16 to $2.57, according to the figures in your table.

While February’s move appears to reflect continued interest in the company’s growth story, Yahoo Finance coverage from 2025 highlighted Oliveda’s very rapid reported expansion. The company announced more than $104.5 million in second-year US sales, growth of nearly 1,700% with plans for further expansion into Canada and Europe. Subsequent Yahoo Finance coverage also noted continued strong momentum in 2025, including first-half growth above 70% and the launch of additional international initiatives.

Overall, Oliveda remains a highly volatile small-cap name, but February’s strong gain suggests investors continue to respond positively to its aggressive growth narrative and international expansion plans. At the same time, the gap between the current share price and its 52-week high indicates that sentiment remains uneven and that the stock is still likely to trade with elevated volatility.

The Beachbody Company, Inc. (NYSE: BODI) operates as a fitness and nutrition company in the United States and internationally. The company offers Beachbody on Demand, a subscription streaming service providing fitness programs such as P90X, Insanity and 21 Day Fix; nutrition programs including Portion Fix and 2B Mindset; and nutritional products like Shakeology shakes and Beachbody Performance supplements. The company has also faced regulatory scrutiny in California related to the classification of independent contractors, an issue that could potentially impact aspects of its historical direct selling model.

Company developments during the month continued to center on Beachbody’s broader turnaround strategy and its efforts to stabilize revenue while strengthening its digital subscription platform. Management remains focused on expanding its BODi streaming ecosystem, improving user engagement across its digital content library, and maintaining cost discipline following the company’s transition away from its former multi-level marketing structure. While the company remains in the early stages of rebuilding consistent growth, February developments suggest that investors continue to monitor subscriber trends, operating efficiency and the company’s ability to generate sustainable revenue growth as key indicators of the long-term success of its transformation strategy.

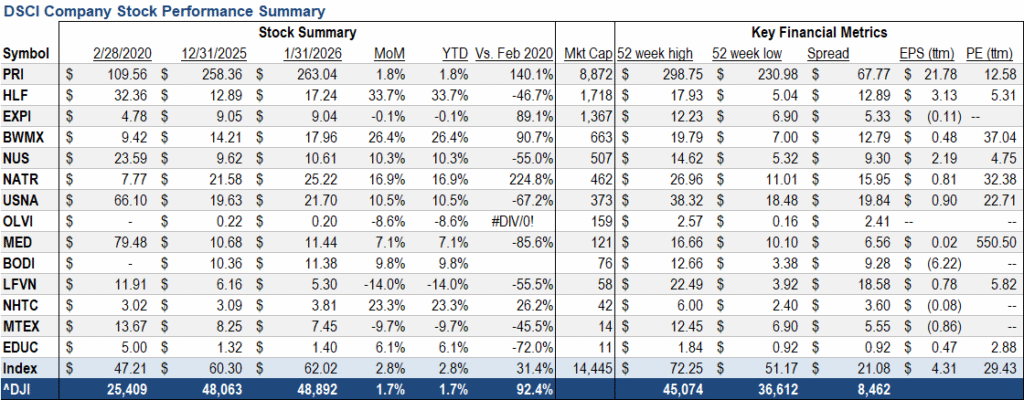

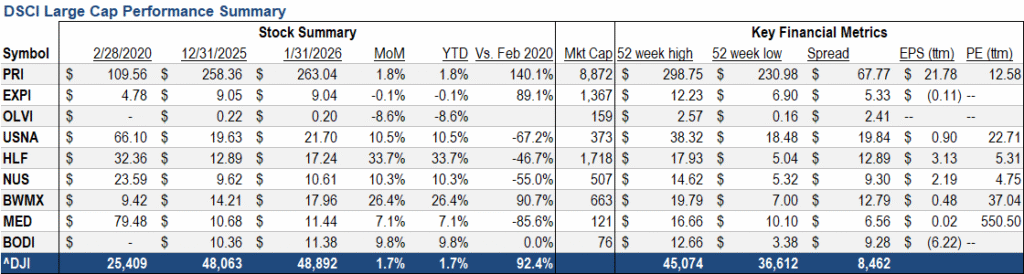

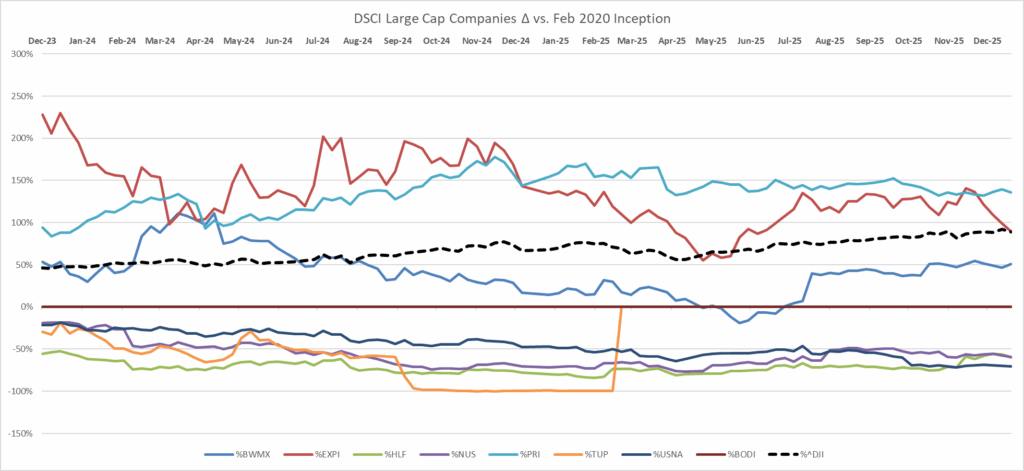

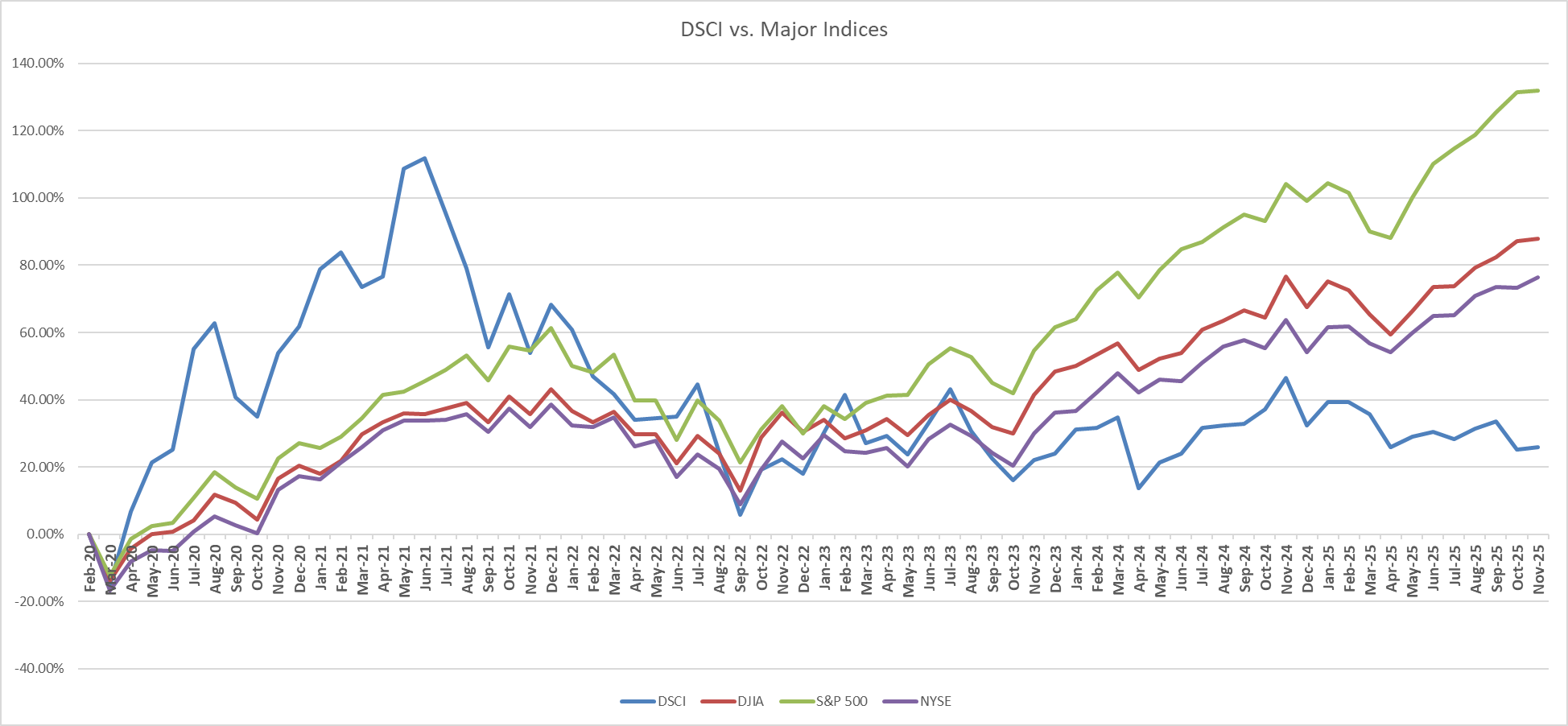

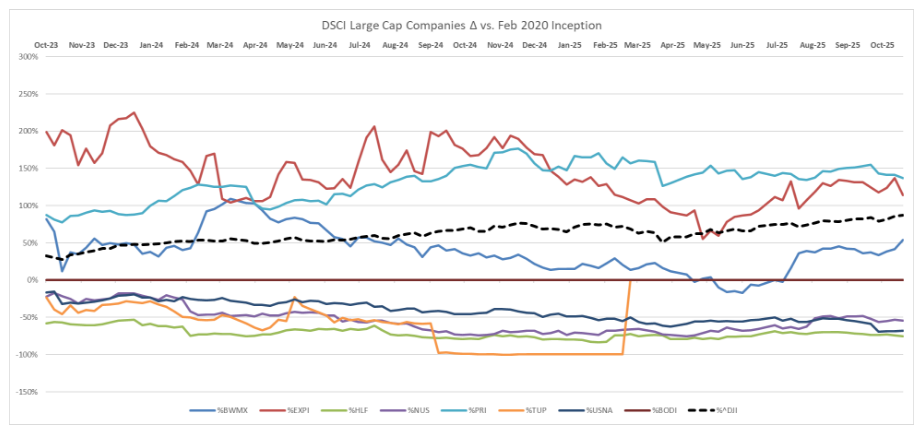

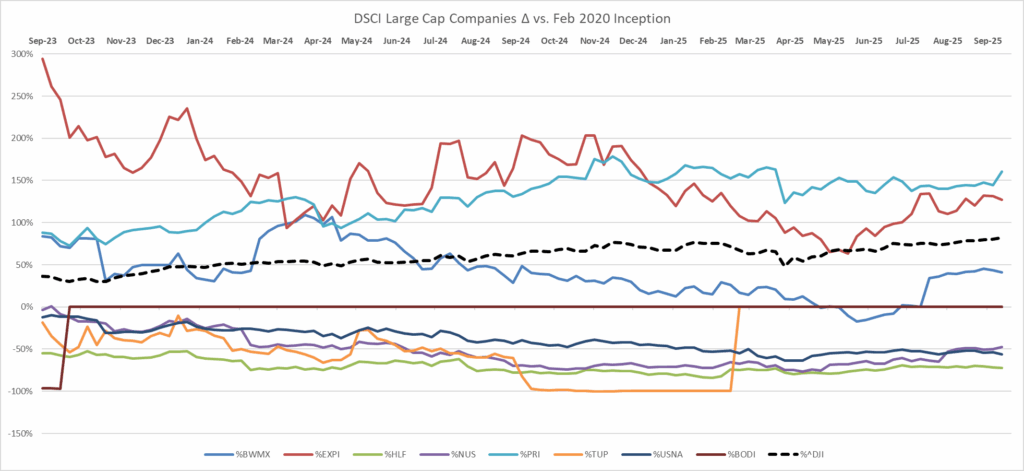

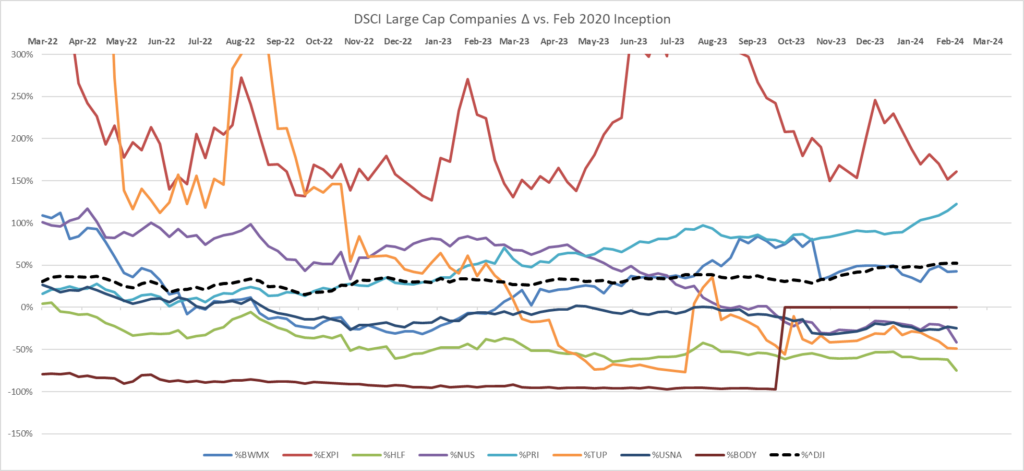

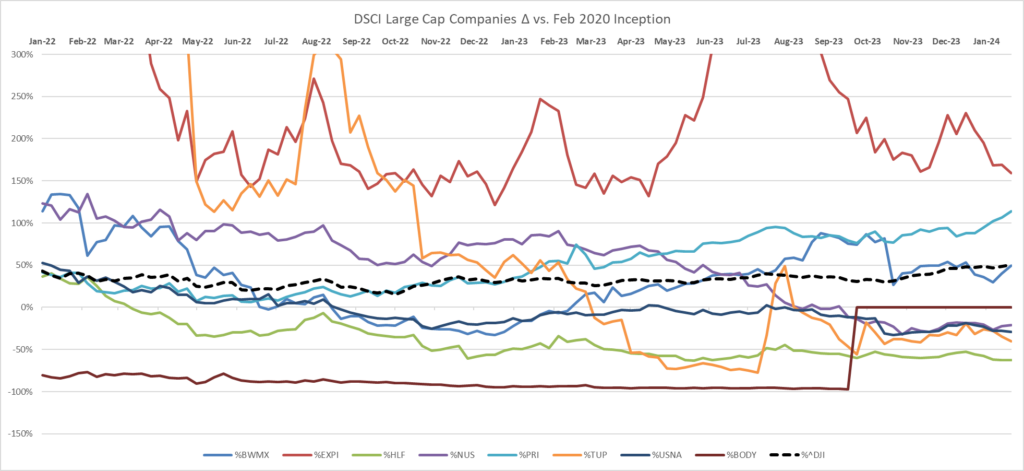

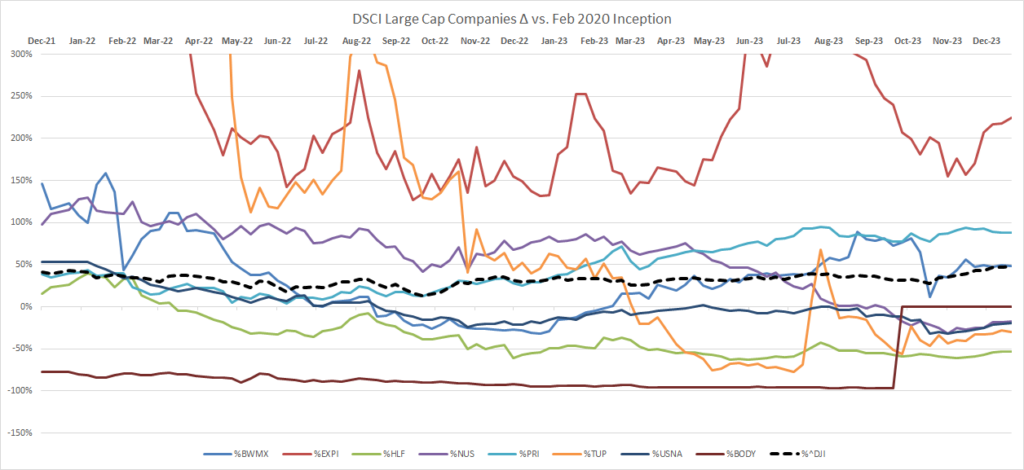

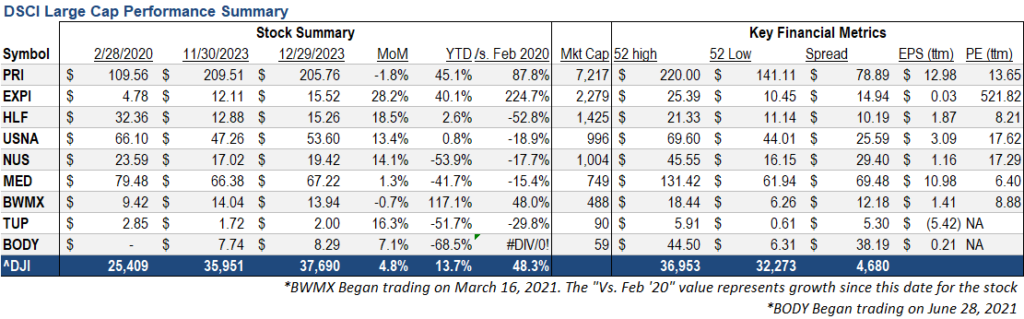

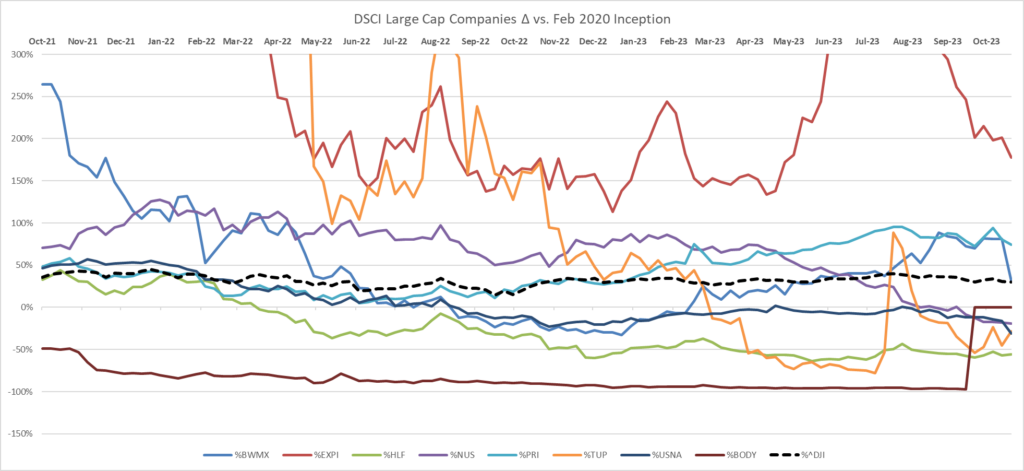

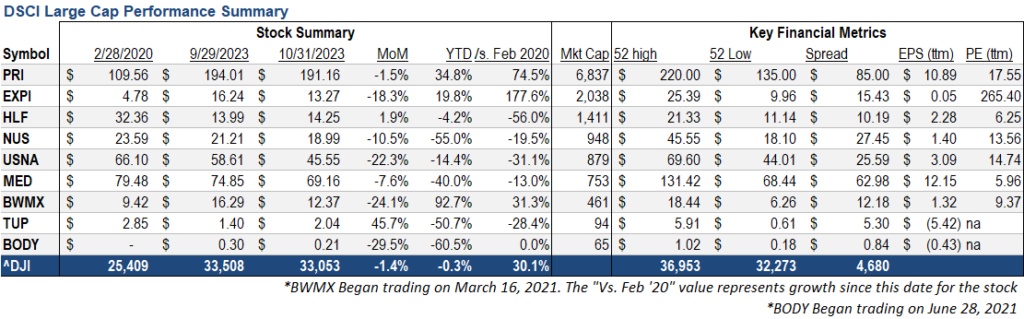

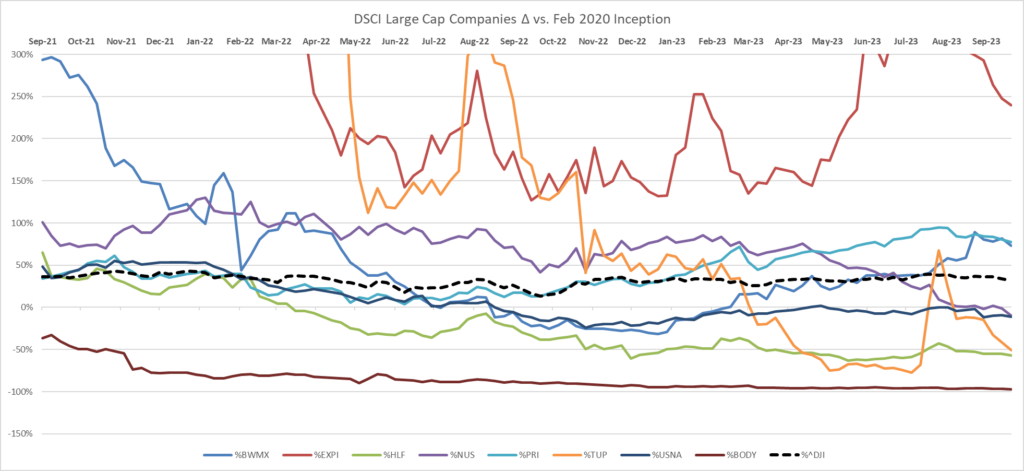

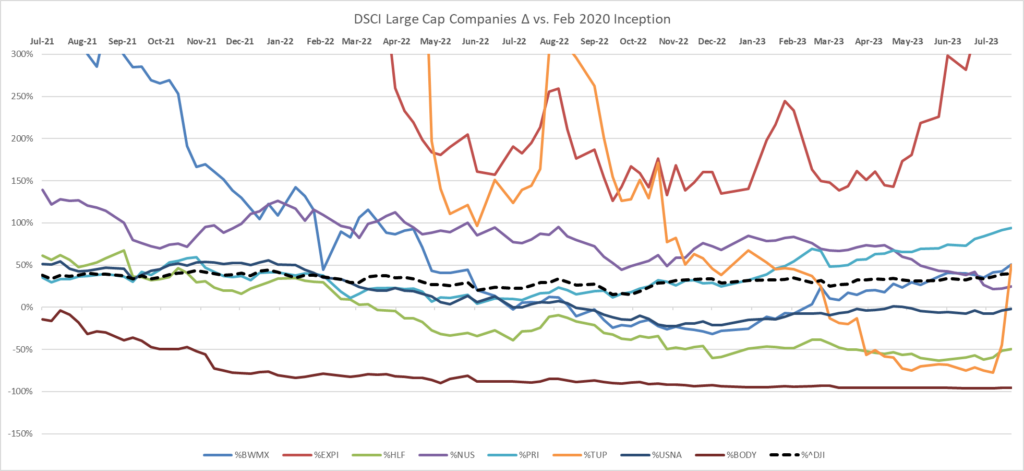

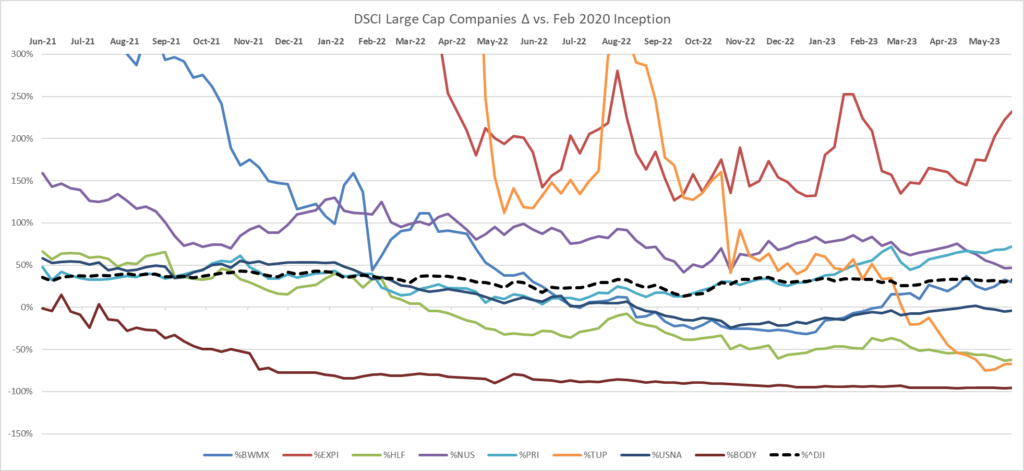

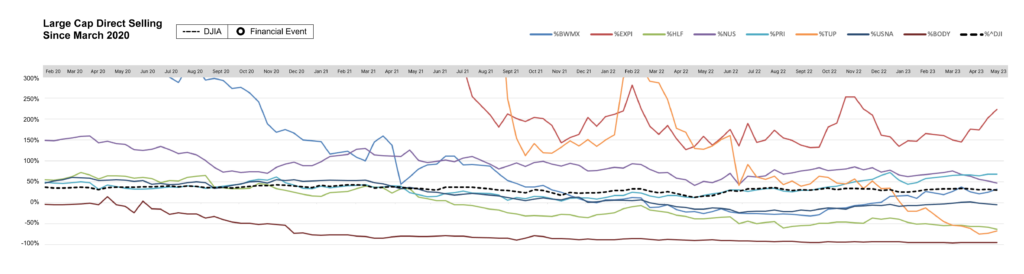

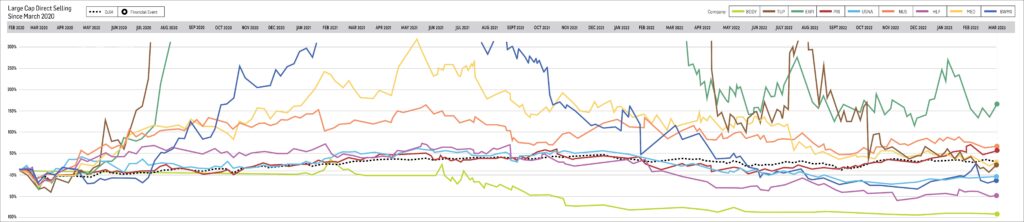

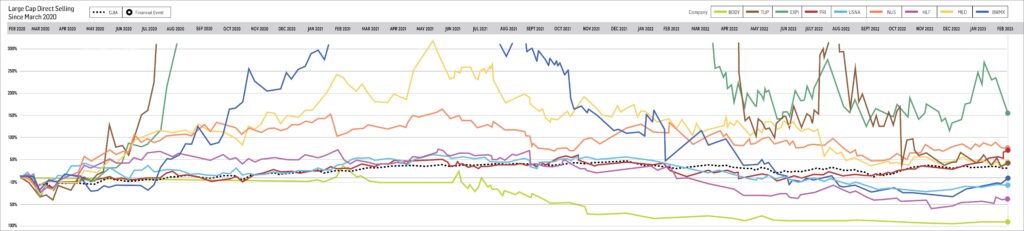

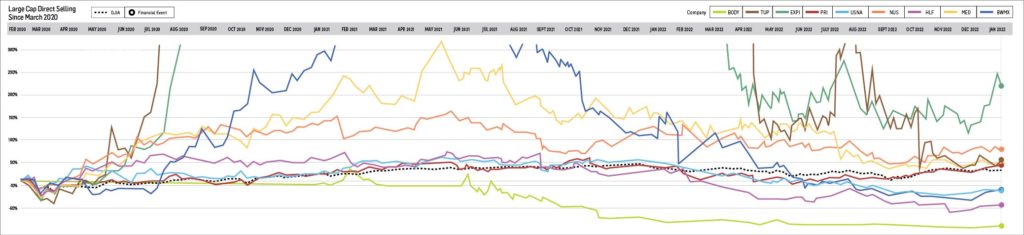

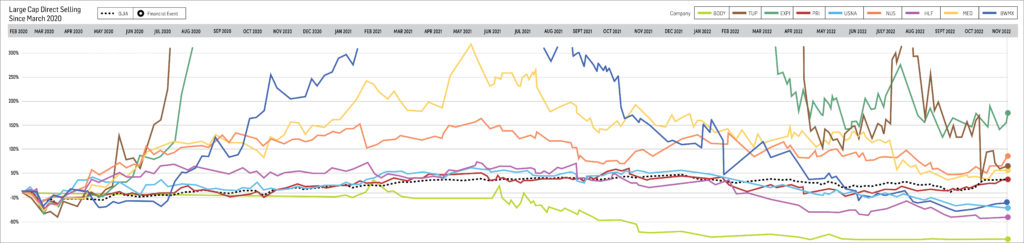

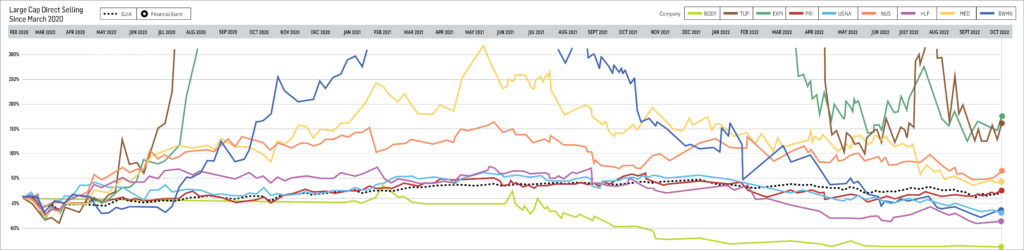

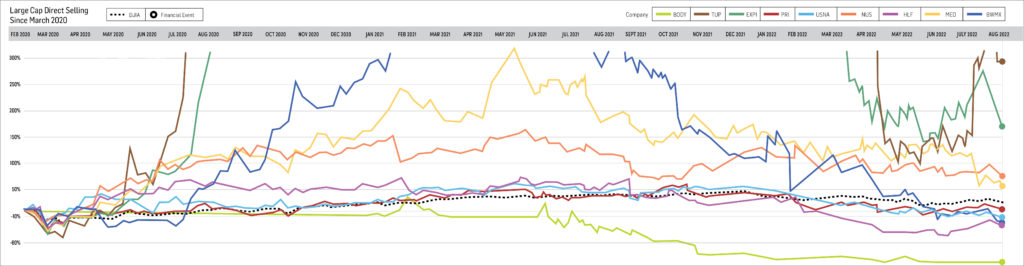

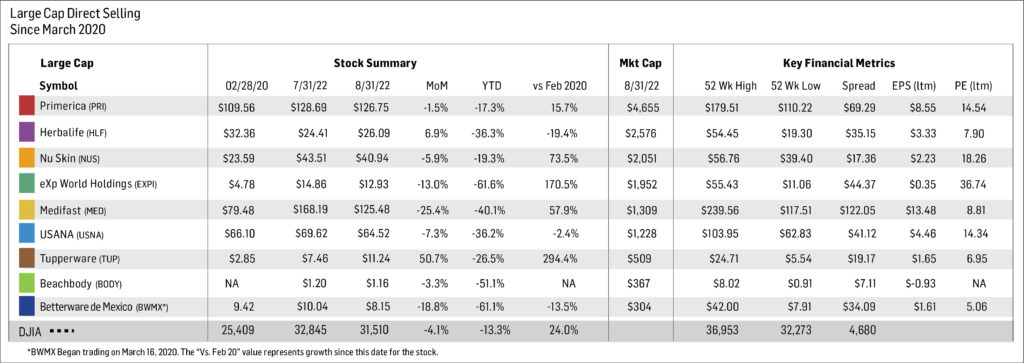

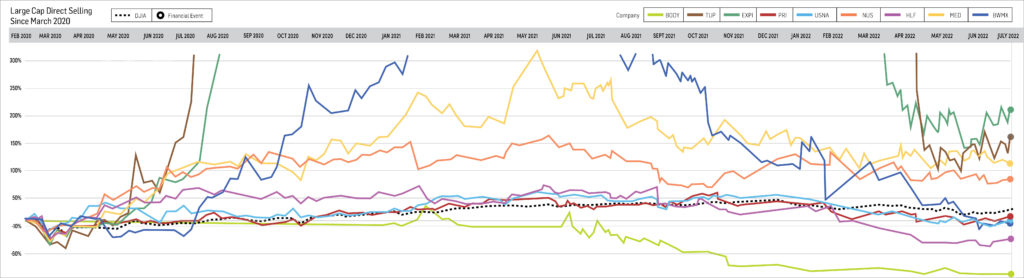

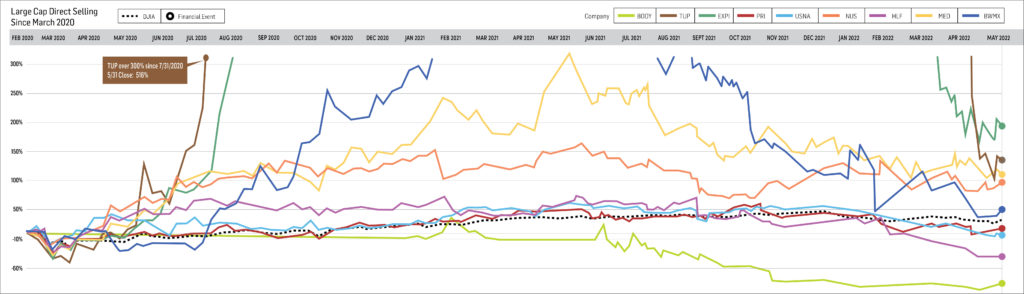

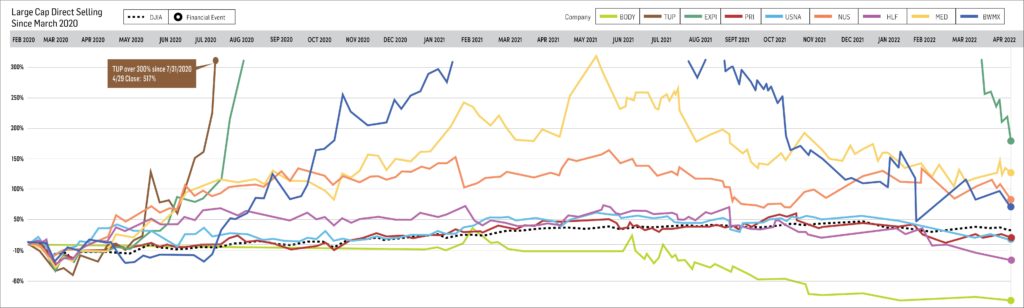

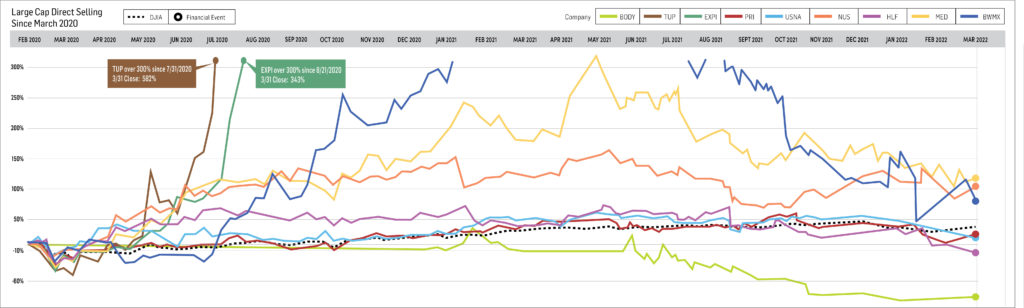

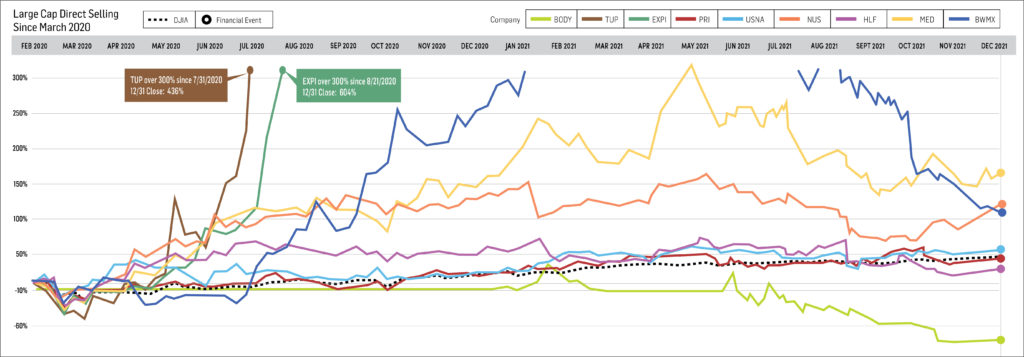

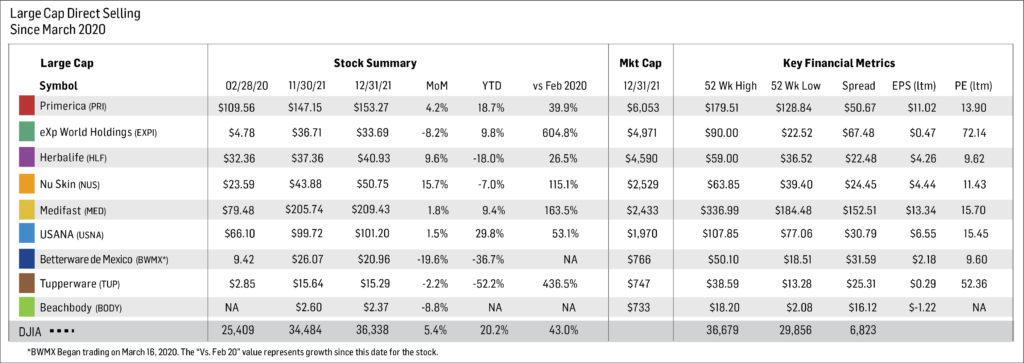

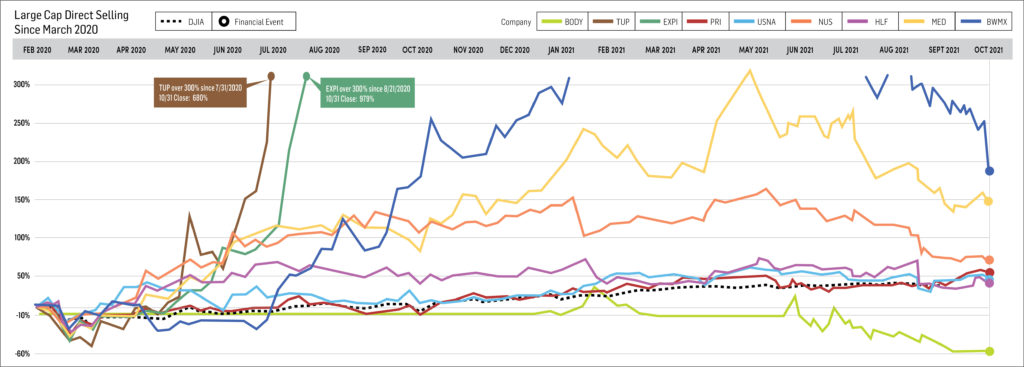

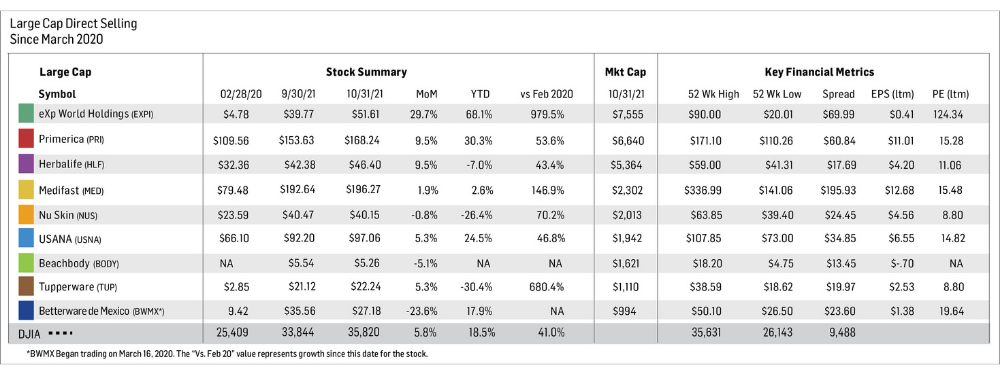

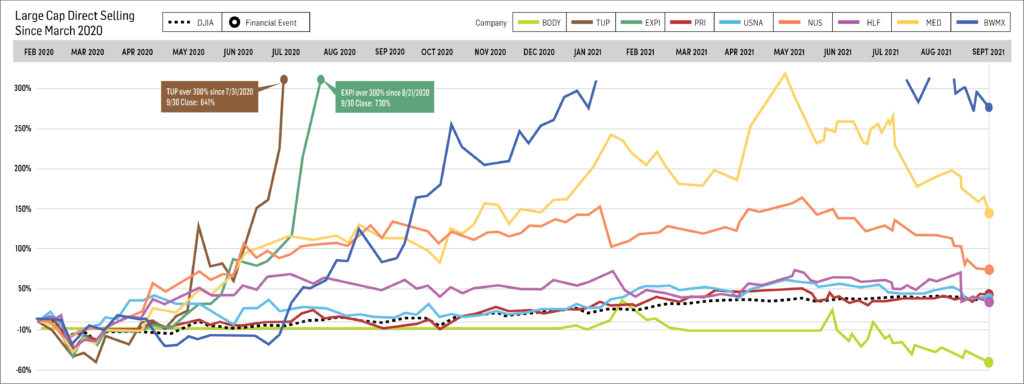

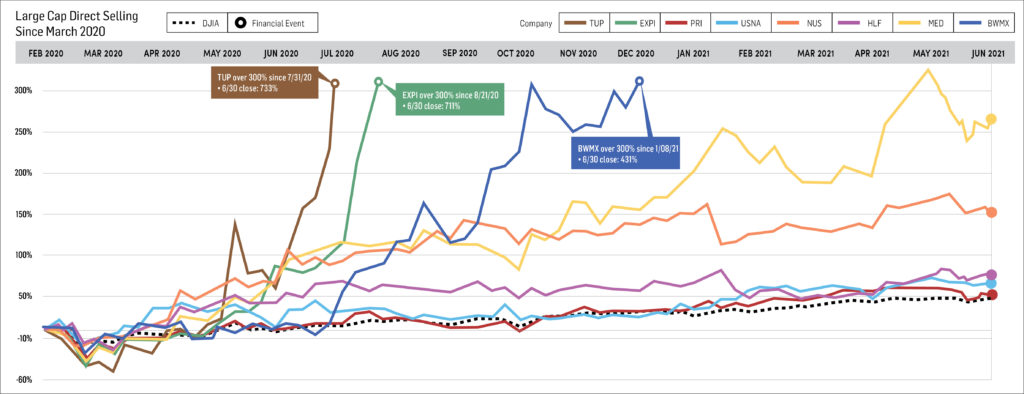

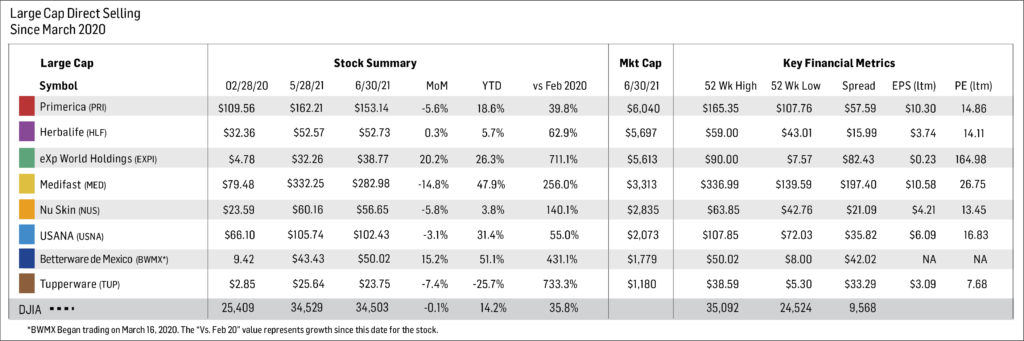

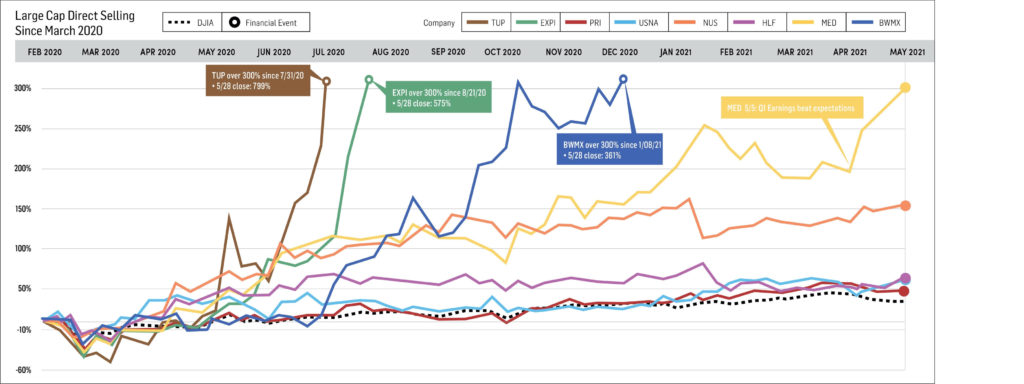

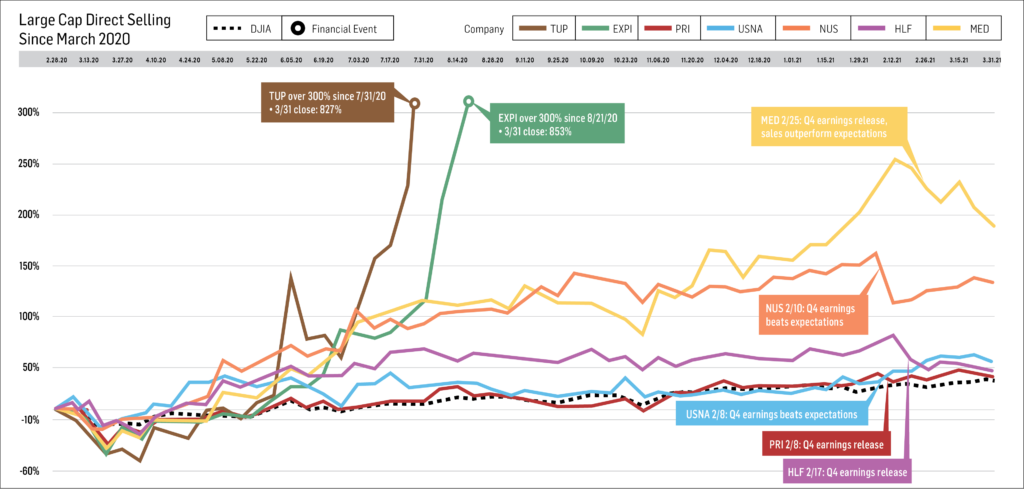

Below are two summary diagrams on the direct selling large cap companies.

The Real Brokerage Inc. (NASDAQ: REAX) is a technology-driven, asset-light real estate brokerage that empowers agents through a cloud-based platform, AI-enabled tools and integrated fintech solutions. Founded in 2014, the company operates across the United States and Canada, utilizing an independent contractor model and performance-based compensation structure that aligns with direct selling adjacent distribution frameworks.

During February 2026, Real’s narrative remained centered on platform expansion, agent-led governance and continued team recruitment rather than on any single headline financial release. On February 11 the company appointed agent leader Ken Pozek to its Board of Directors, a move that reinforced management’s emphasis on agent representation and long-term alignment with the field. Later in the month, Real also announced that Bachman Realty Group joined the platform, adding 65 agents and further strengthening the company’s footprint in the Dallas-Fort Worth and Houston markets.

These developments suggest that February was another month of steady execution against Real’s quality-at-scale strategy. Rather than pursuing growth solely through broad-based recruitment, the company continued to attract established, productive teams that can deepen density in strategic markets while leveraging Real’s technology stack, including its brokerage, mortgage, title and wallet ecosystem. That operating approach remains consistent with the growth profile highlighted previously by Direct Selling News, which has described Real as a rapidly scaling, agent-centric platform that has continued to expand its network despite a still-challenging housing backdrop.

Looking ahead, the February developments positioned Real well heading into its early March earnings release. Strong fourth-quarter and full-year 2025 results, highlighted by fourth-quarter revenue of $505.1 million, representing 44% year-over-year growth, along with gross profit of $39 million and adjusted EBITDA of $14.2 million, underscored the company’s solid operating momentum heading into March. The company’s February developments support a constructive view of Real’s platform expansion, recruiting strength and long-term scalability.

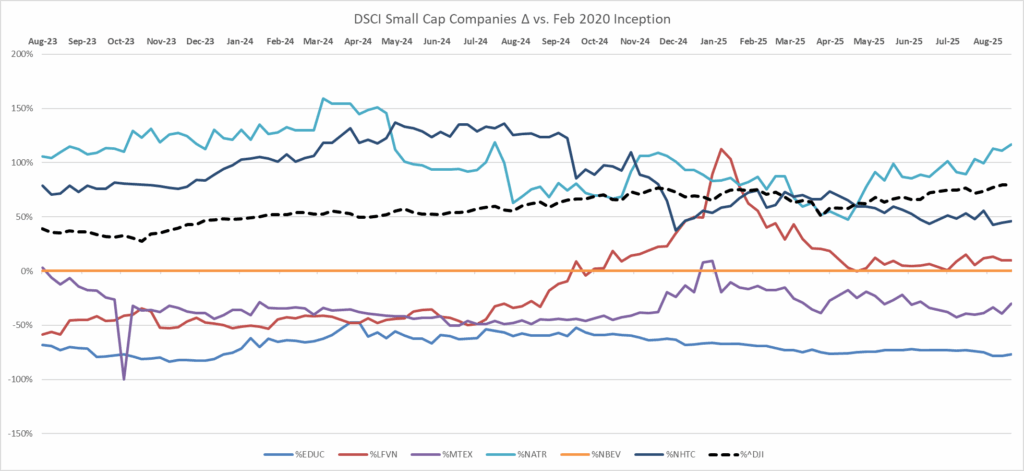

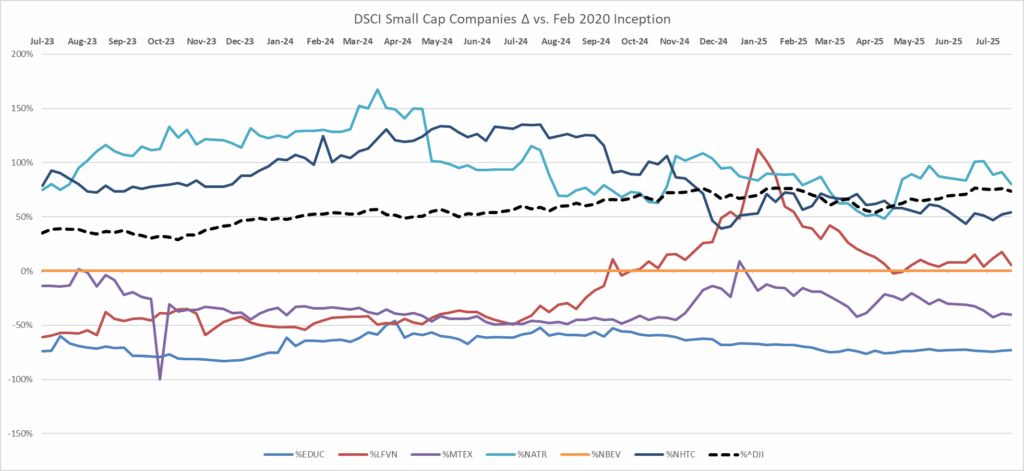

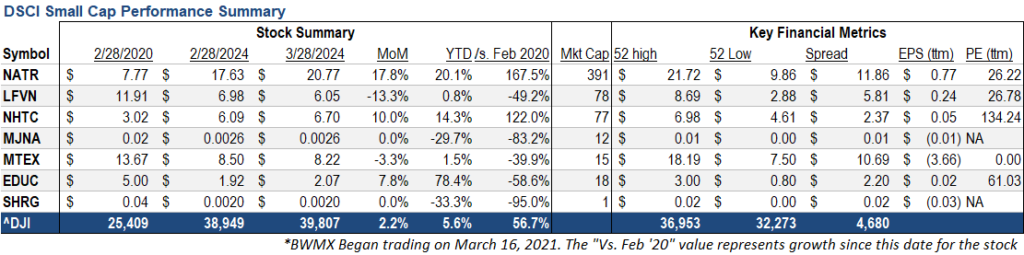

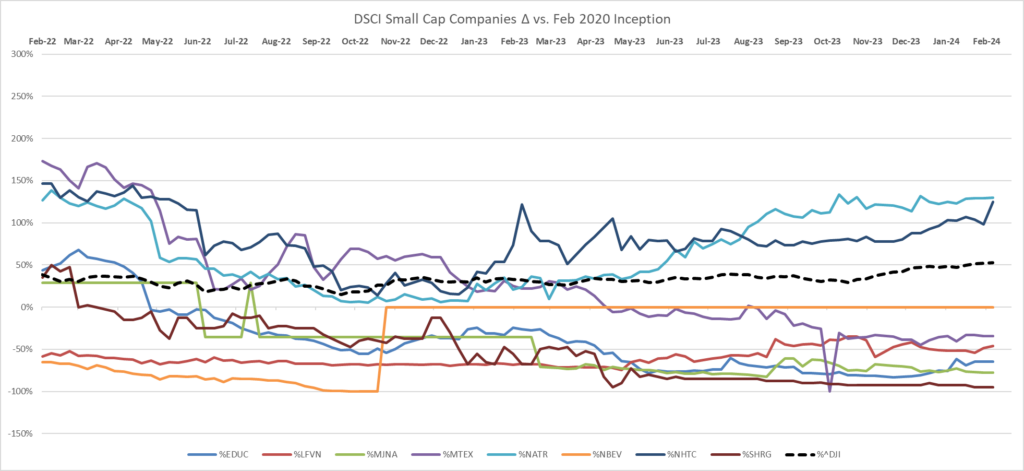

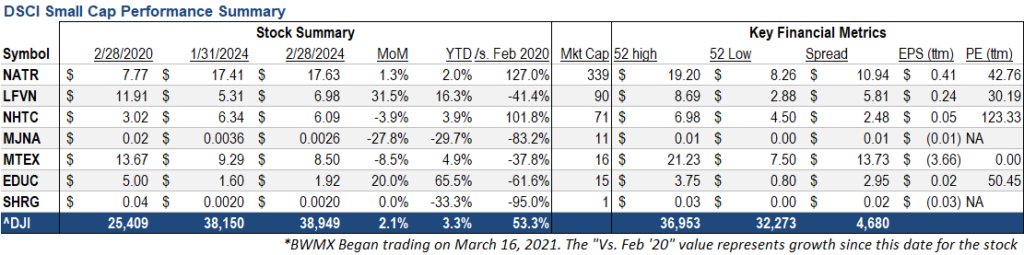

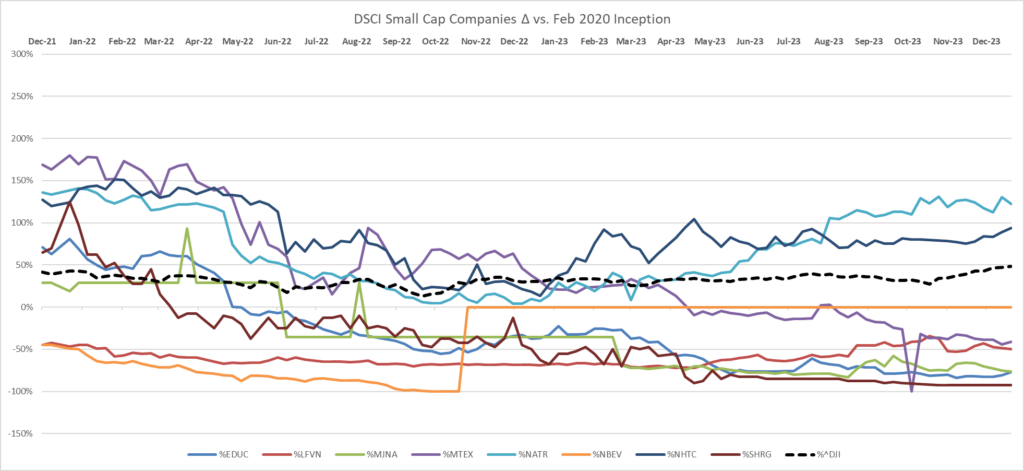

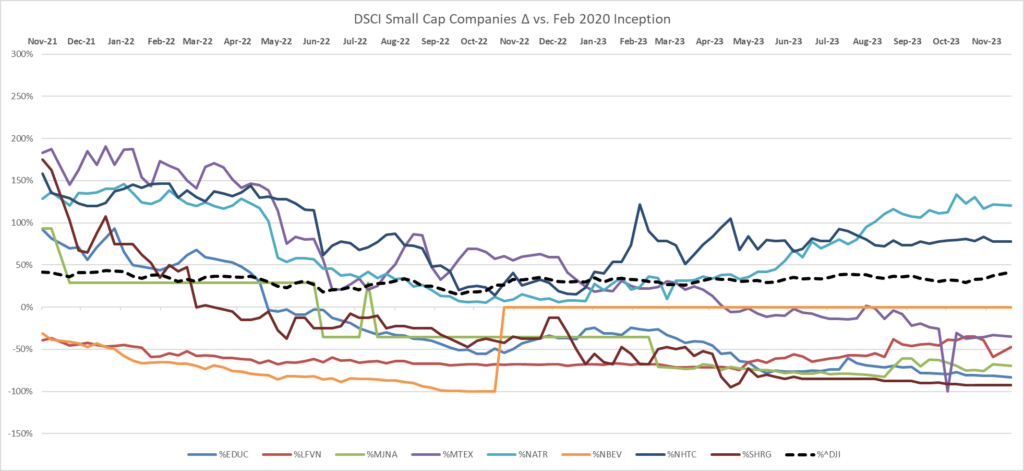

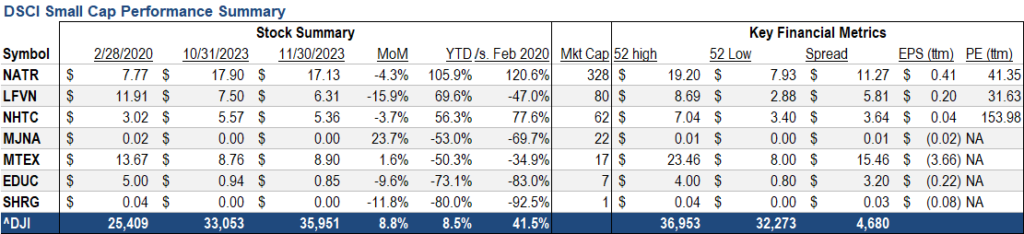

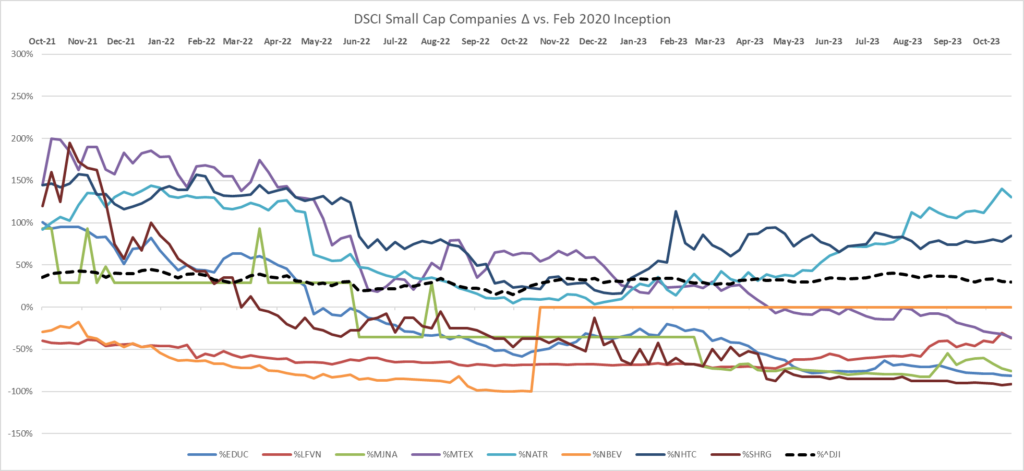

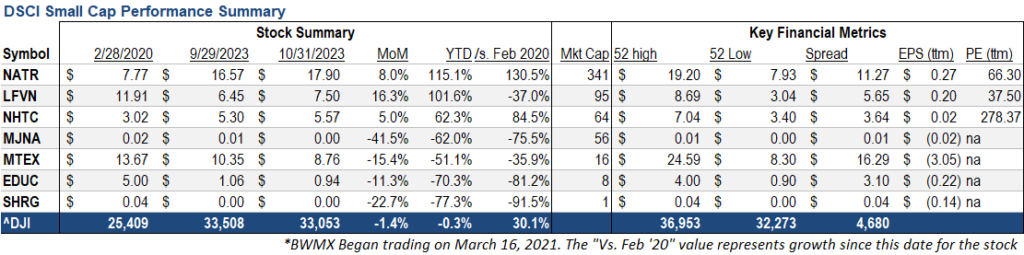

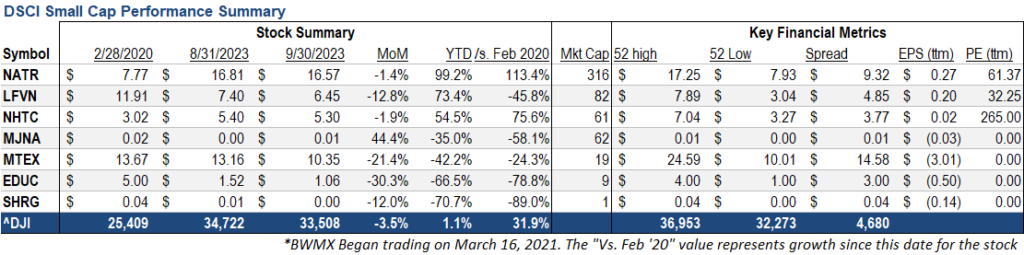

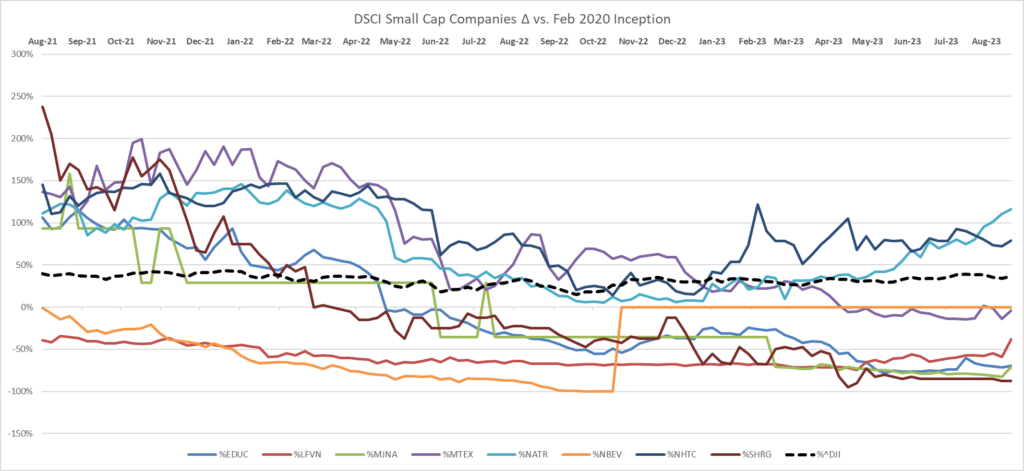

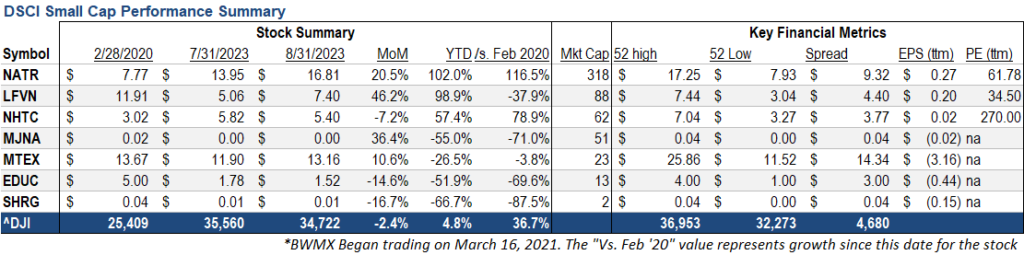

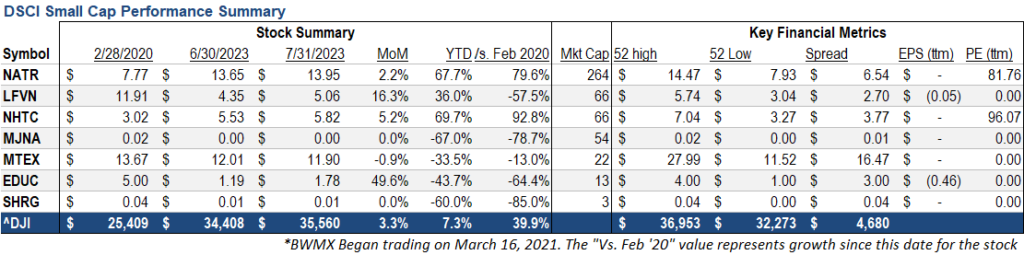

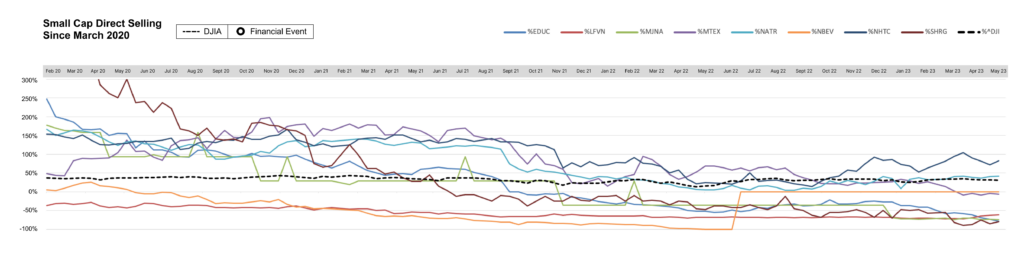

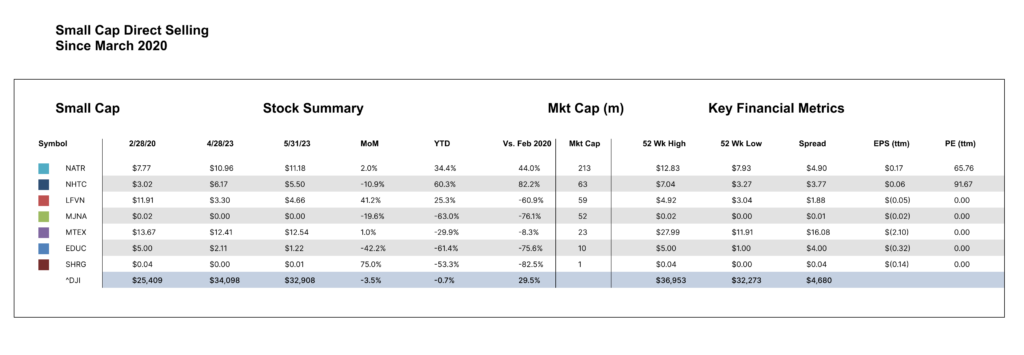

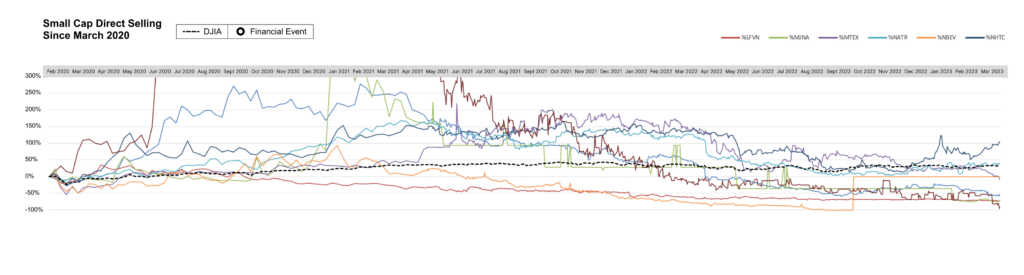

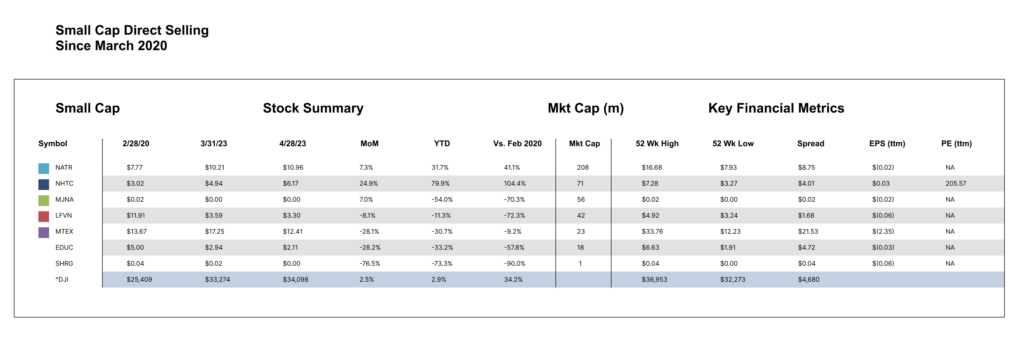

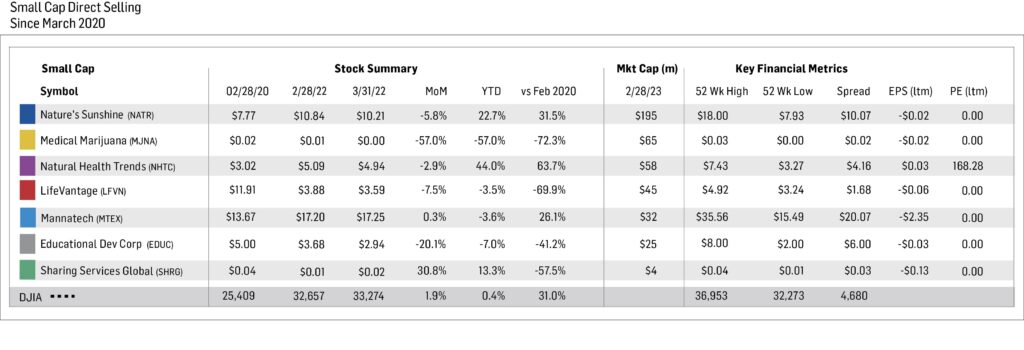

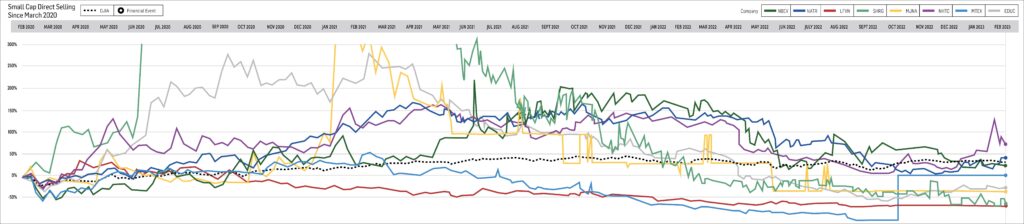

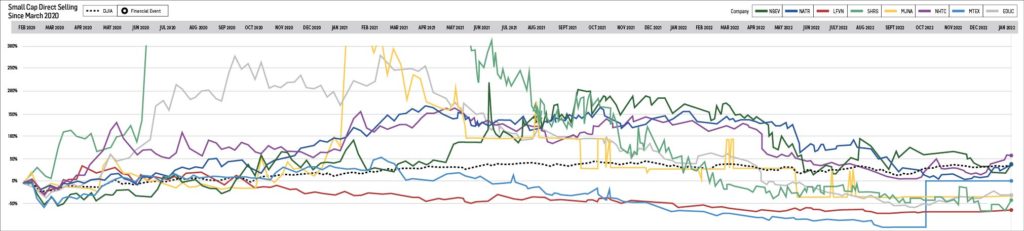

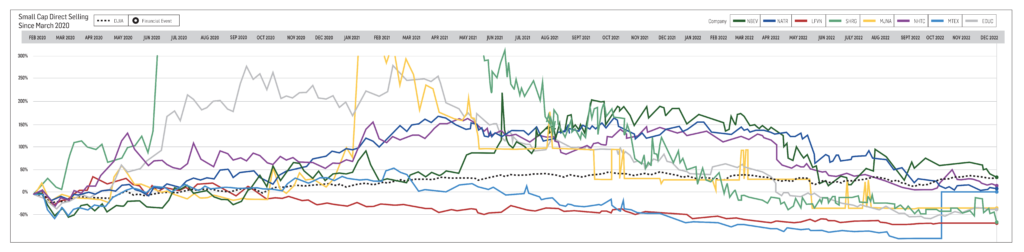

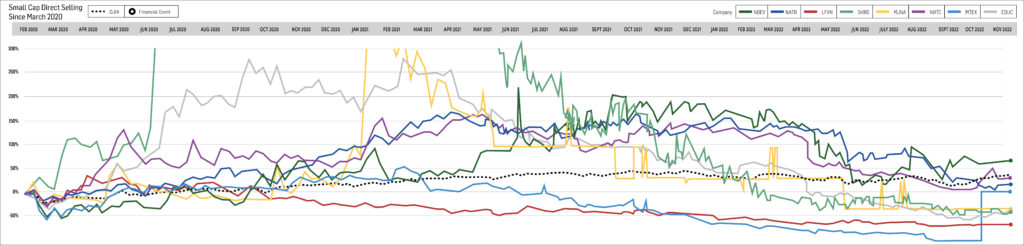

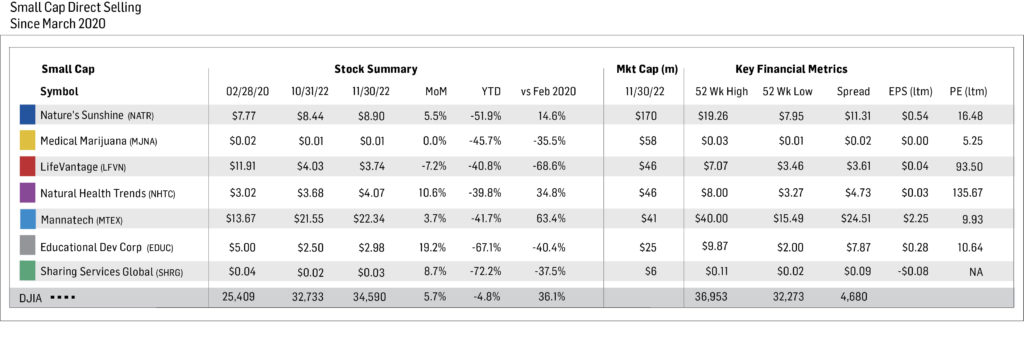

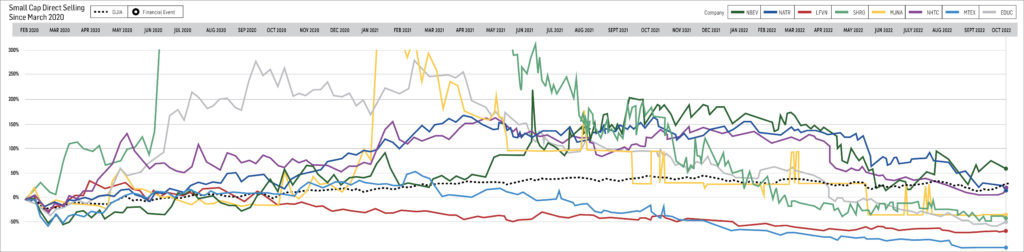

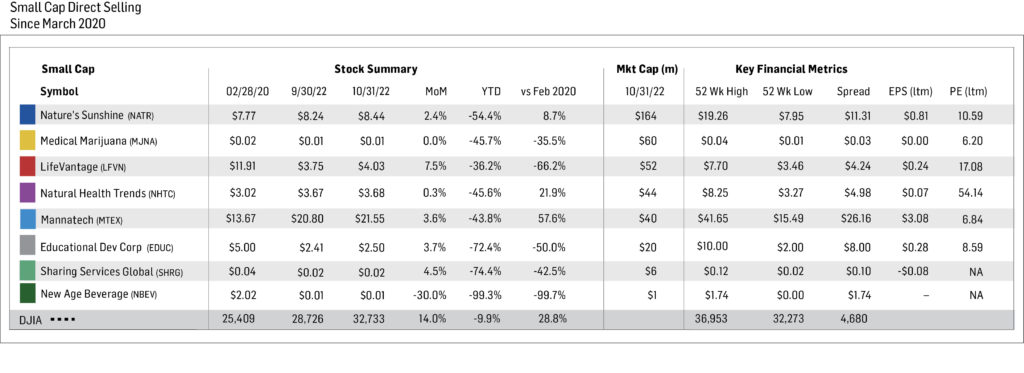

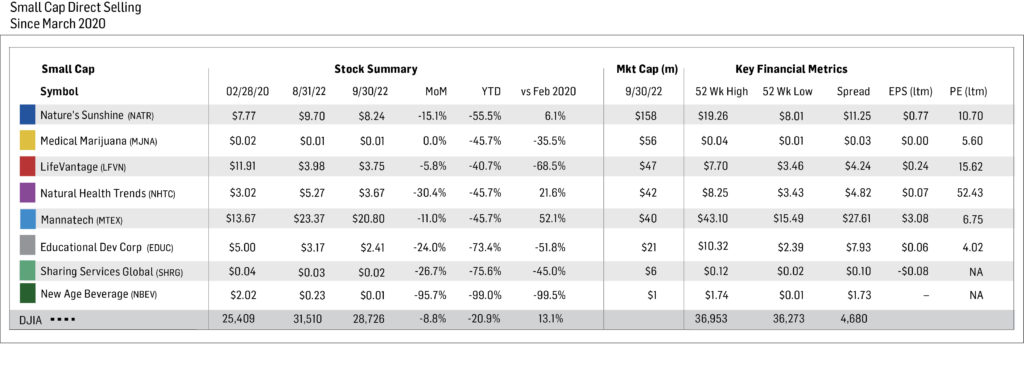

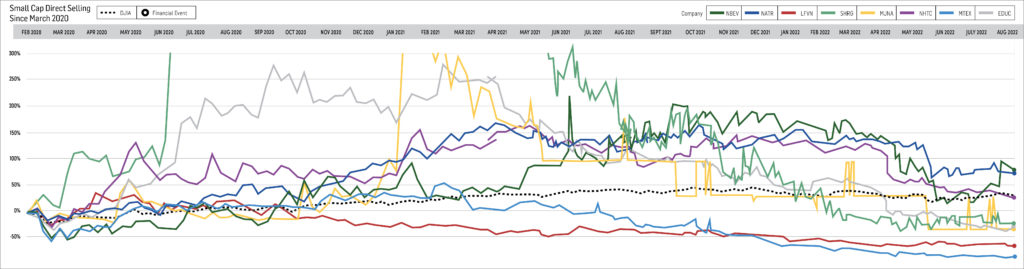

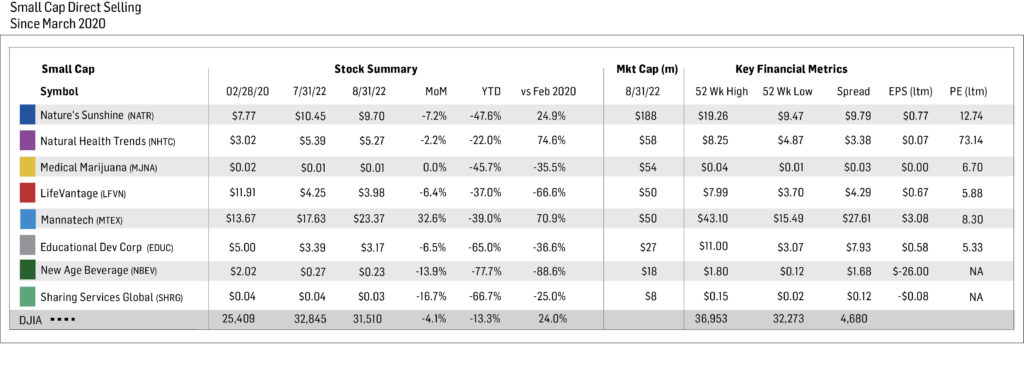

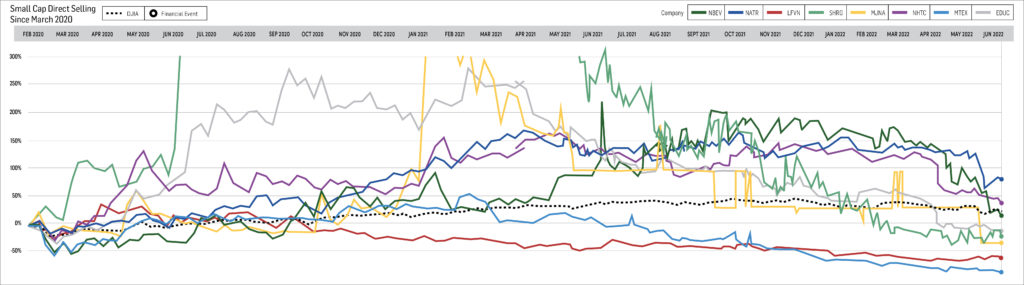

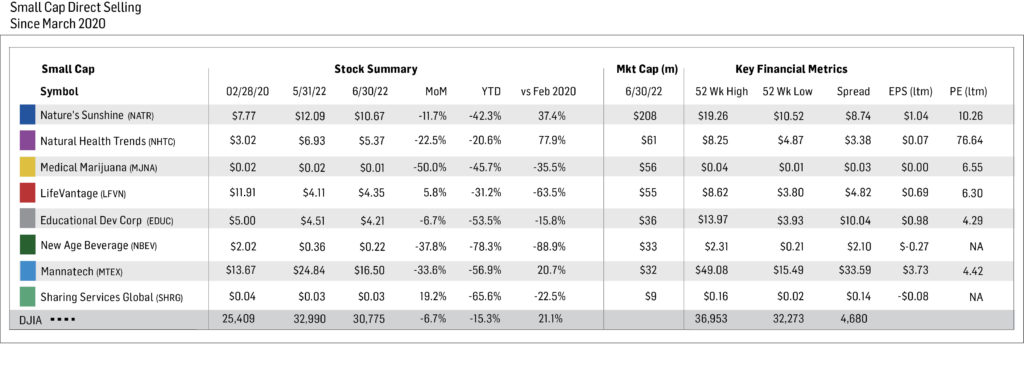

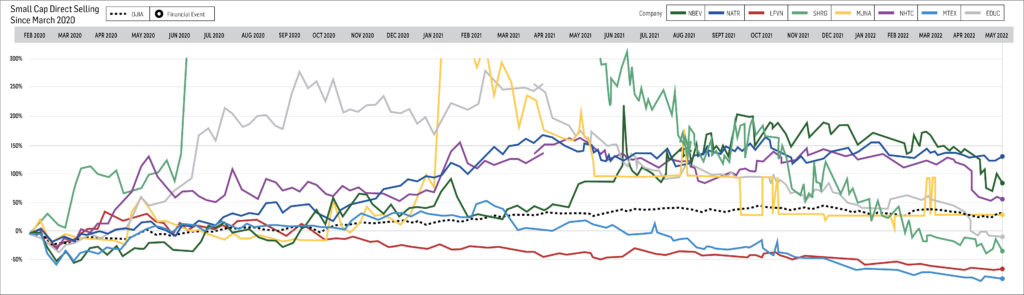

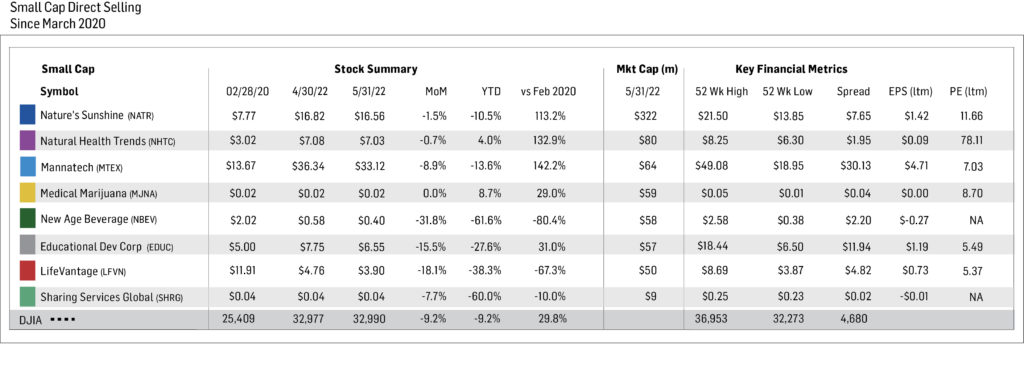

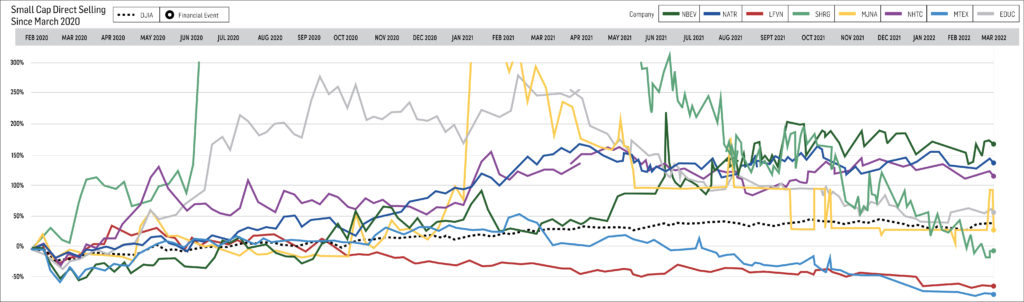

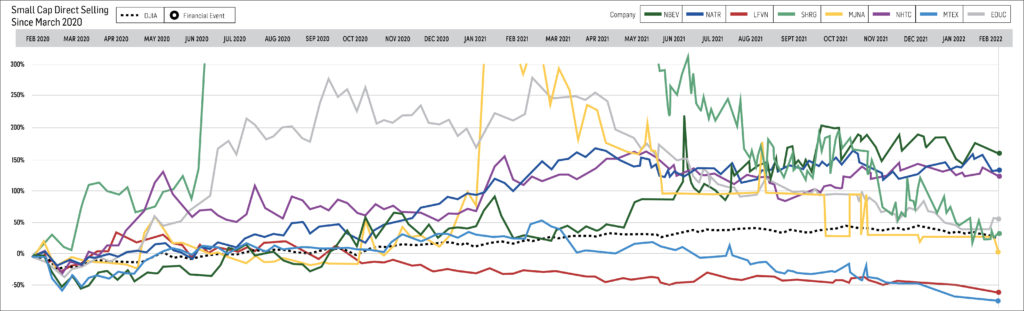

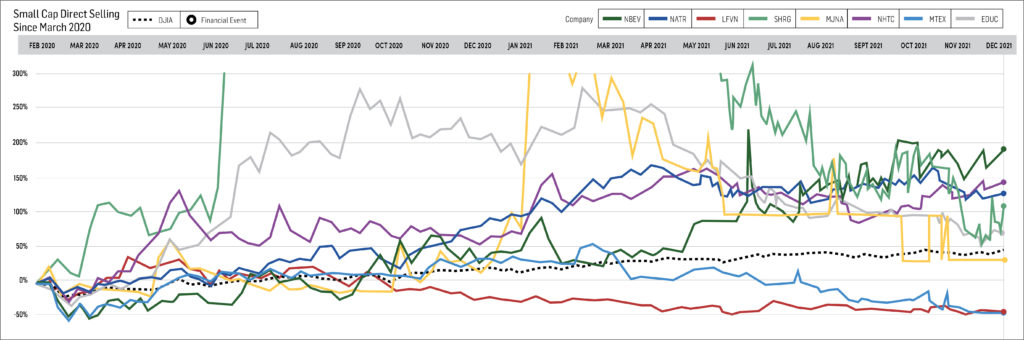

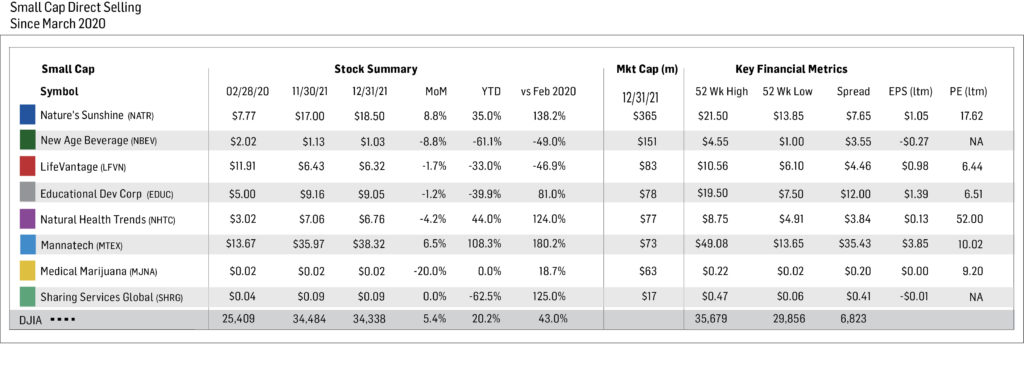

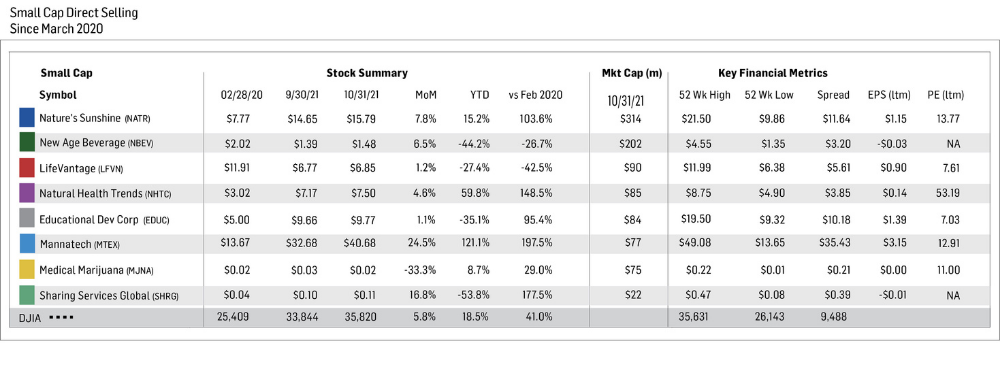

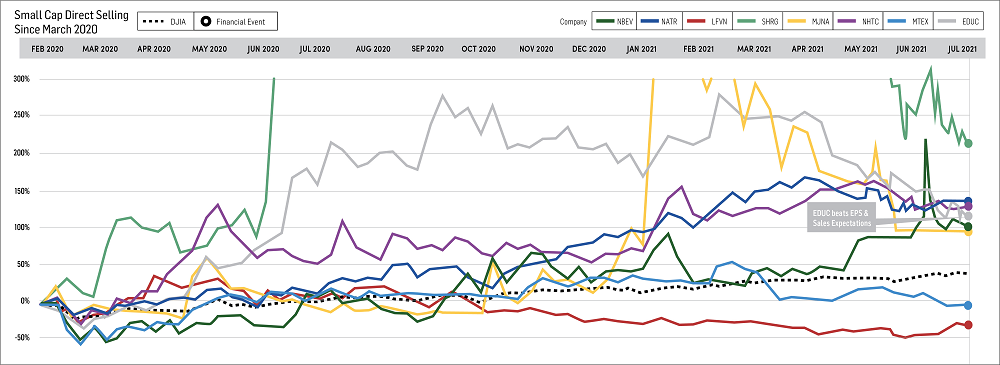

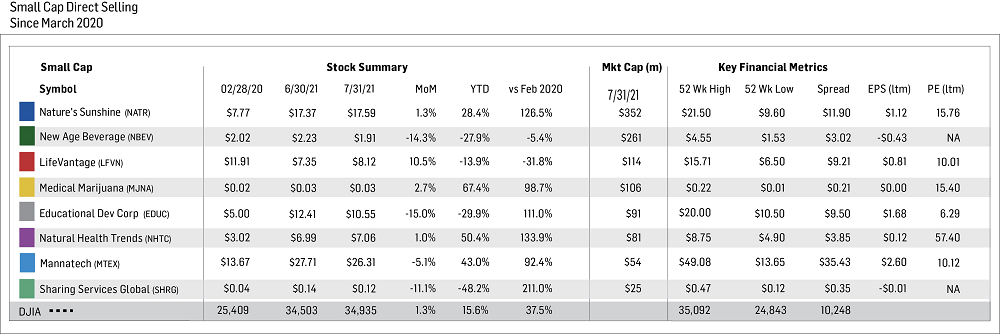

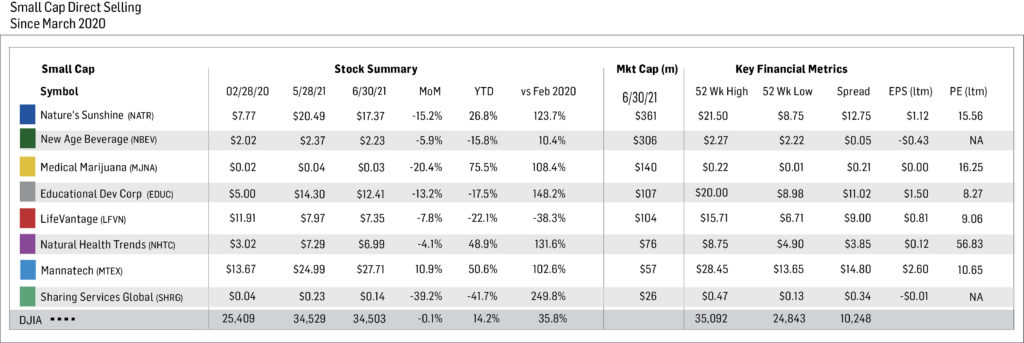

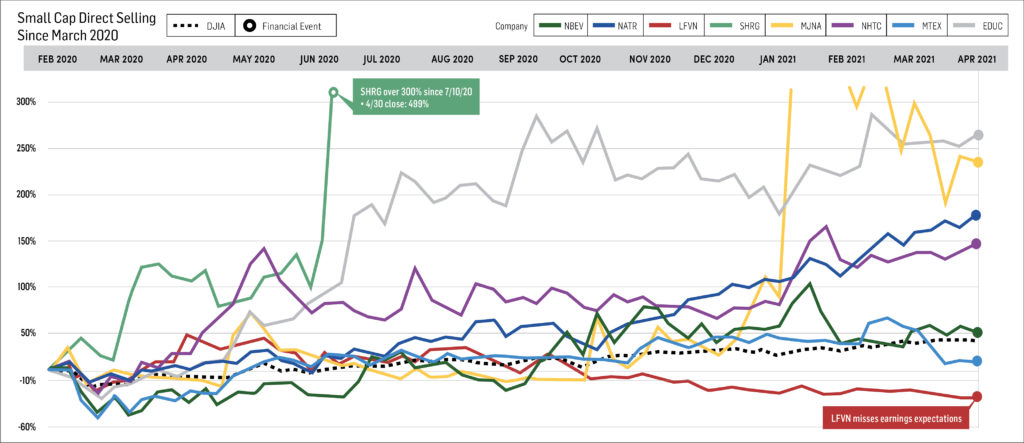

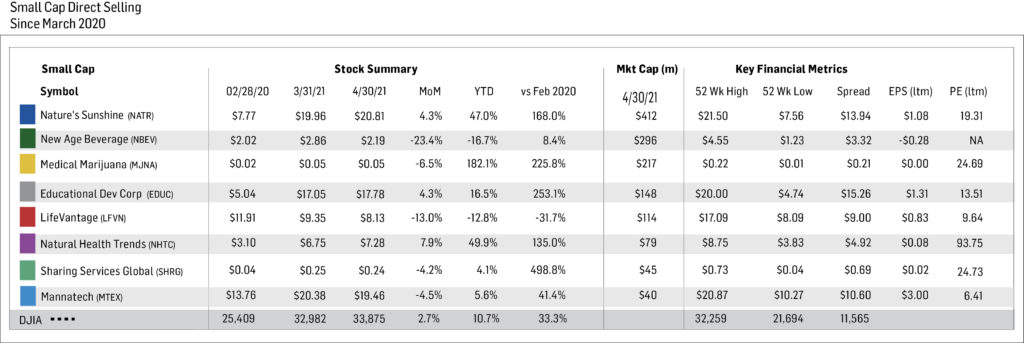

Small Cap

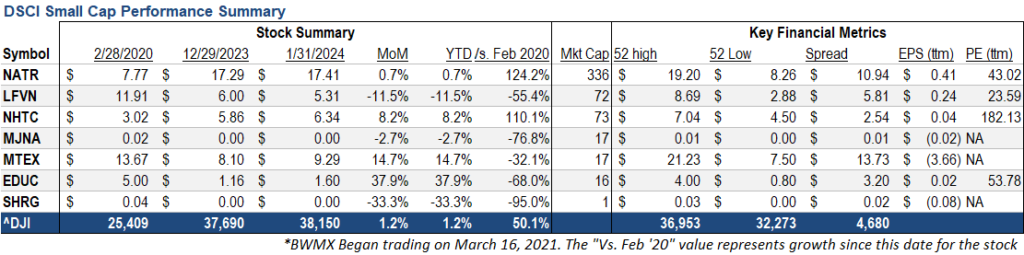

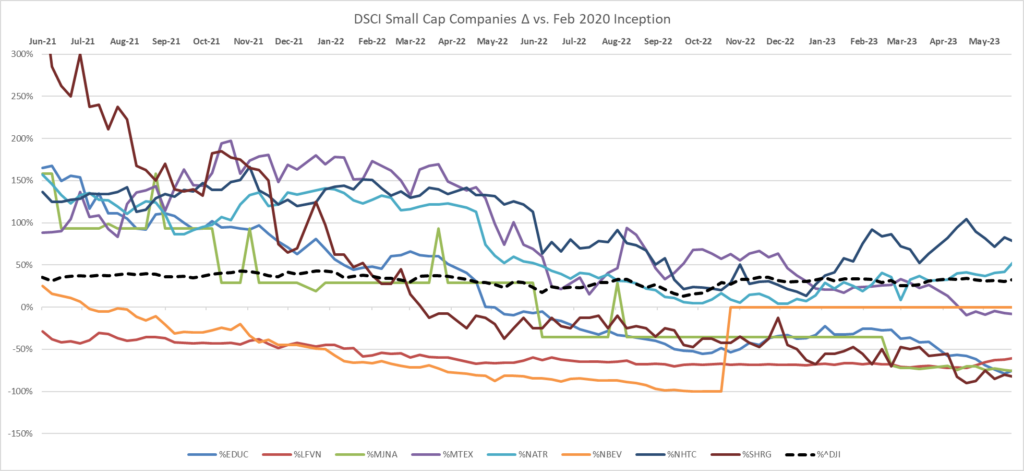

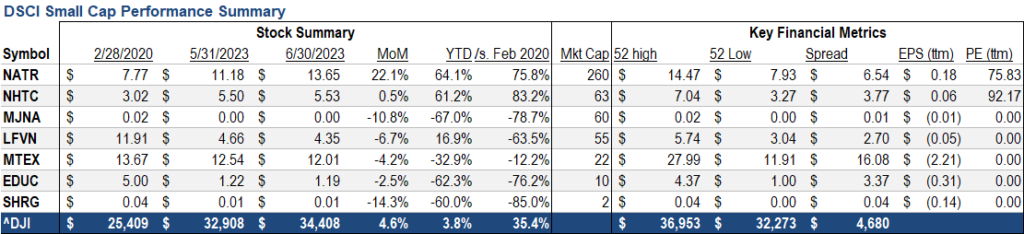

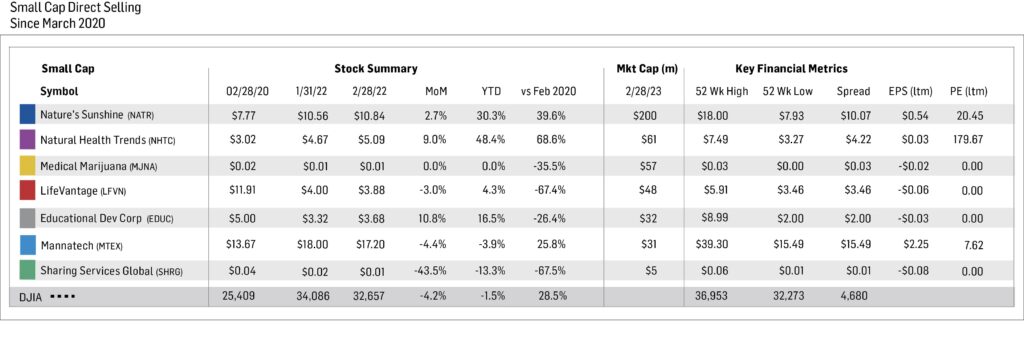

Below is the February information for the two largest small cap companies, Nature’s Sunshine and LifeVantage.

Nature’s Sunshine Products, Inc. (NASDAQ: NATR), a natural health and wellness company, manufactures and sells nutritional and personal care products in Asia, Europe, North America, Latin America and internationally. The company provides general health products related to blood sugar support, bone health, cellular health, cognitive function, joint health, mood, sexual health, sleep, sports and energy and vision; immune products; cardiovascular products; and digestive products. It also offers personal care products, including oils and lotions, aloe vera gel, herbal shampoo, herbal skin treatment, toothpaste and skin cleanser products, as well as weight management products. The company provides its products under the Nature’s Sunshine Products and Synergy WorldWide brands directly to customers and to a sales force of independent consultants. Nature’s Sunshine Products, Inc. was founded in 1972 and is headquartered in Lehi, Utah.

In February 2026, Nature’s Sunshine shares increased 9.8% compared to January, ending the month at $27.68. Year-to-date, the stock is up 28.3%, and since February 2020 it has gained 256.4%. Market capitalization stands at approximately $466 million. The stock traded near its 52-week high of $28.14, with a 52-week low of $11.01, while trailing EPS stands at $0.81 and the stock trades at approximately 32.6x trailing earnings.

Investor sentiment remained constructive during February as the company approaches the release of its fourth-quarter and full-year 2025 financial results. Recent operating updates highlighted continued momentum in revenue growth, improving margins, and a solid balance sheet position with no outstanding debt. These factors have supported positive sentiment toward the company’s operational trajectory heading into the new fiscal year.

LifeVantage Corporation (NASDAQ: LFVN) engages in the identification, research, development, formulation and sale of advanced nutrigenomic activators, dietary supplements, nootropics, pre- and probiotics, weight management, and skin and hair care products. It offers Protandim, a dietary supplement; LifeVantage Omega+, a dietary supplement that combines DHA and EPA Omega-3 fatty acids, Omega-7 fatty acids, and vitamin D3; LifeVantage ProBio, a dietary supplement to support gut health; LifeVantage IC Bright, a supplement to support eye and brain health, reduce eye fatigue and strain, supports cognitive functions, and support normal sleep patterns; LifeVantage Daily Wellness, a dietary supplement designed to strengthen immune health; LifeVantage Rise AM & Reset PM System that provides the body with the right nutrients; LifeVantage D3+, a dietary supplement that provides vitamin D3, vitamin K2, magnesium, calcium and other trace minerals to support a balanced immune system, strong bones and cardiovascular health; PhysIQ Fat Burn to support weight management; PhysIQ Prebiotic is a dietary supplement designed to support the good bacteria in the gut and a healthy microbiome; Petandim for Dogs, a supplement to combat oxidative stress in dogs; and Axio, a nootropic energy drink mix. The company also provides anti-aging skincare products, including liquid collagen, facial cleansers, eye cream, moisturizing cream, sunscreen, perfecting lotions, hand creams as well as hair care products such as invigorating shampoos, nourishing conditioners and scalp serums under the TrueScience brand name. It sells its products through its website and network of independent consultants in the United States, Mexico, Japan, Australia, Hong Kong, Canada, Thailand, the United Kingdom, The Netherlands, Germany, Taiwan, Austria, Spain, Ireland, Belgium, New Zealand, Singapore and The Philippines. The company also launched Evolve Compensation Plan and other LV360 initiatives into the Philippines, Taiwan, Hong Kong, and Singapore. The company is based in Lehi, Utah.

In February 2026, LifeVantage shares declined 13.1% compared to January, closing the month at $4.61. The stock is down 25.2% year-to-date and 61.3% since February 2020. Market capitalization is approximately $60 million. The stock’s 52-week range is $3.90 to $17.64, with trailing EPS of $0.60 and a trailing P/E of approximately 7.9x.

The decline followed weaker fiscal Q2 2026 results reported earlier in February. Revenue for the quarter ended December 31, 2025 totaled $48.9 million, representing a 27.8% year-over-year decline, although sales improved modestly on a sequential basis. Management attributed the decline primarily to lower sales of the MindBody GLP-1 System, partially offset by growth in other product categories following the LoveBiome acquisition. Despite the softer revenue environment, the company announced a $60 million share repurchase authorization, signaling management’s confidence in the long-term outlook.

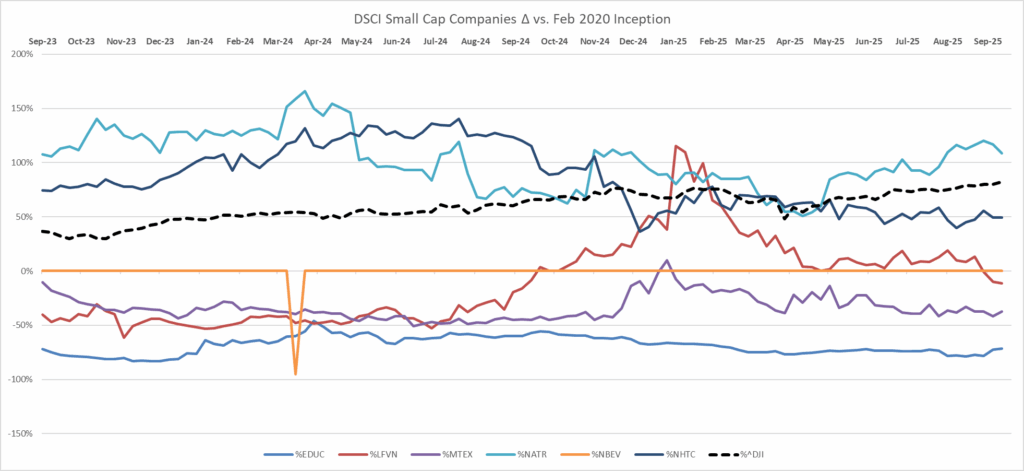

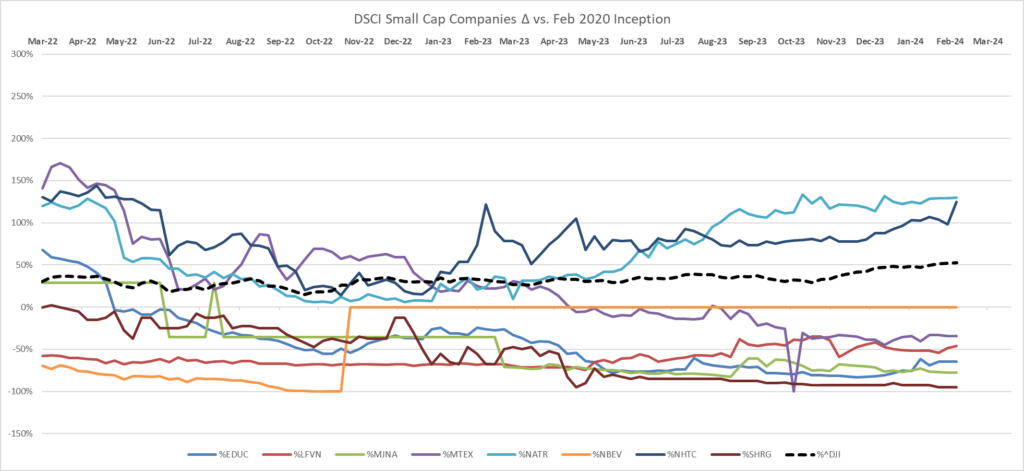

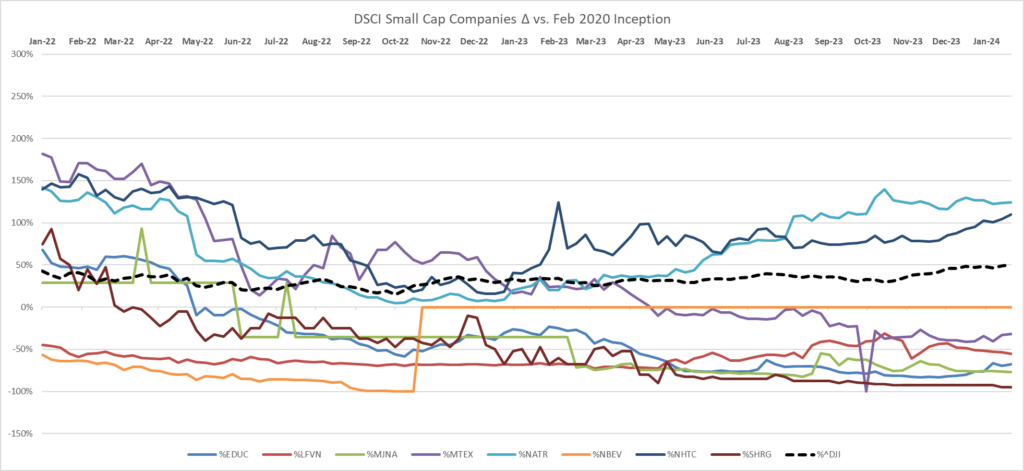

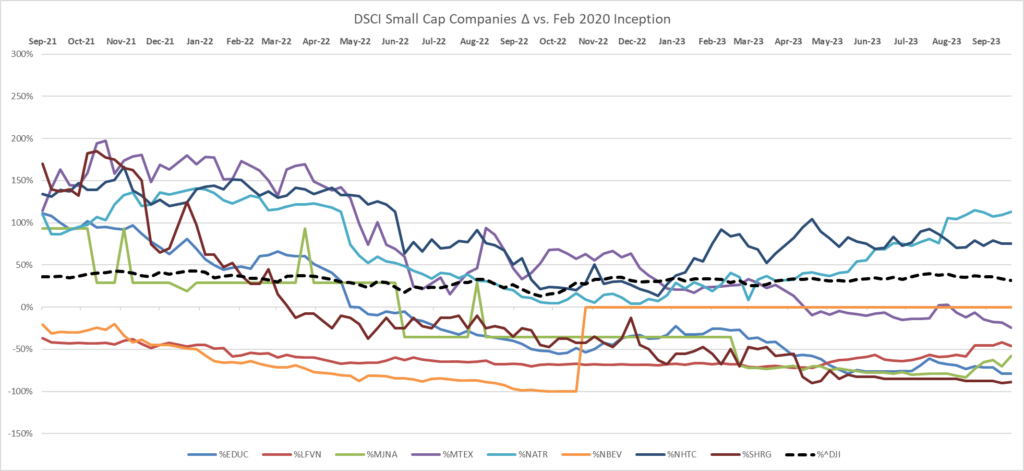

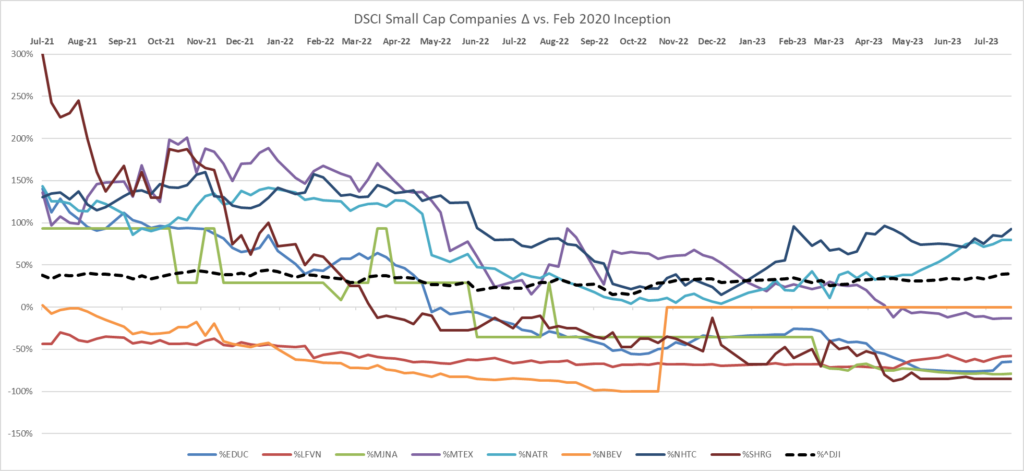

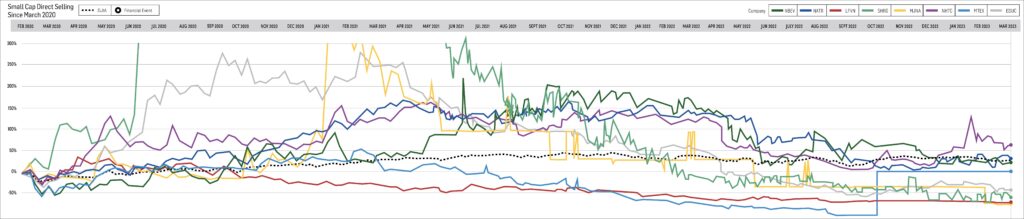

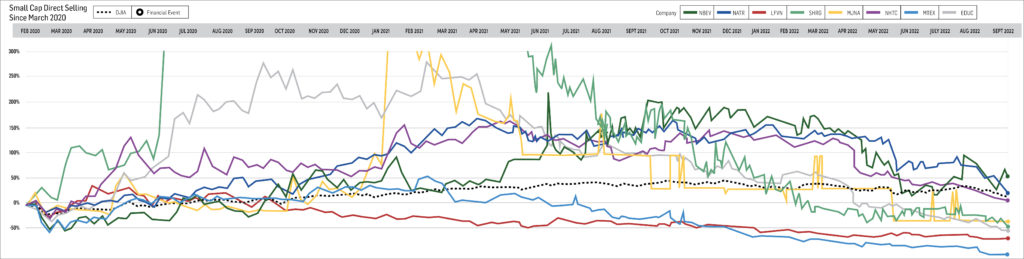

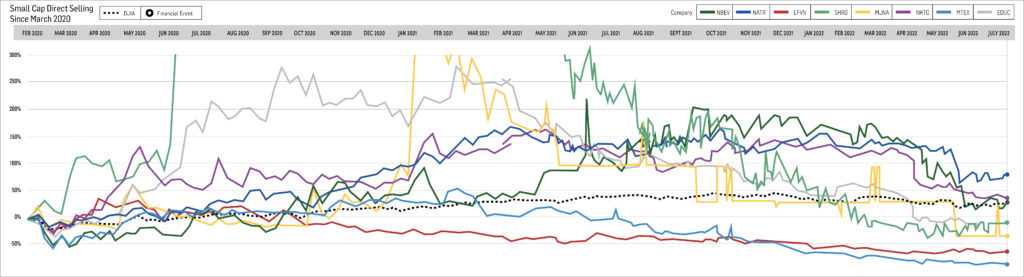

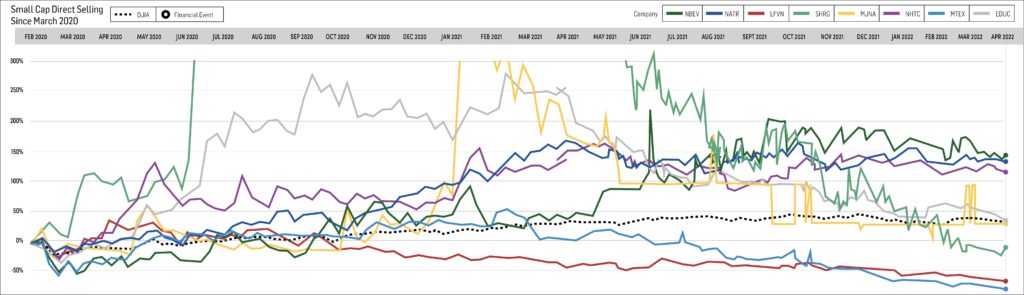

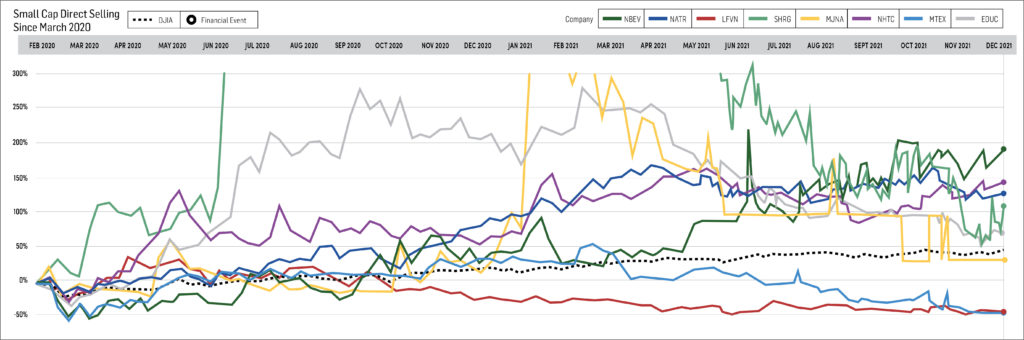

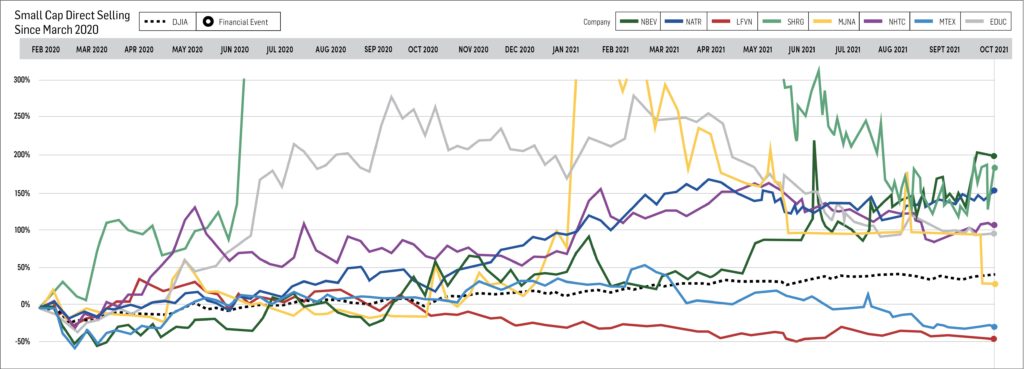

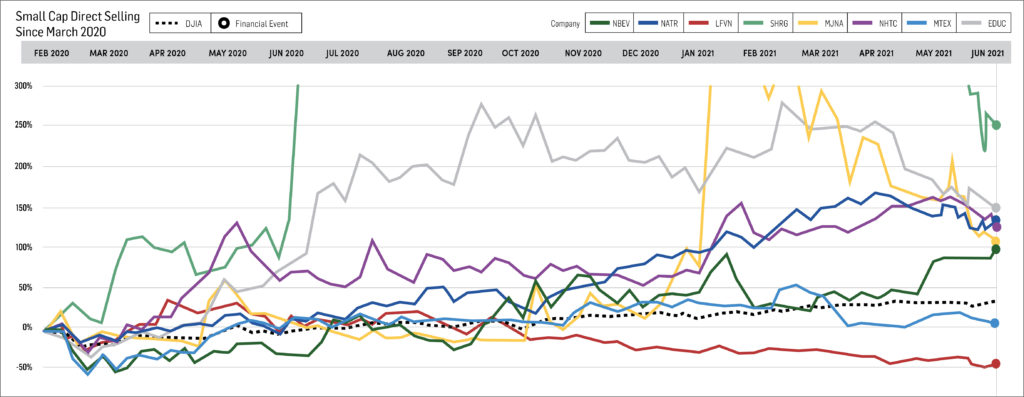

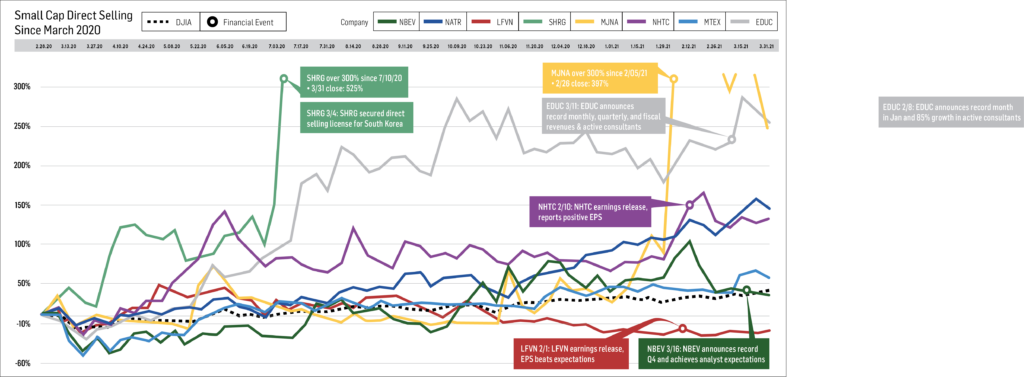

Below are two summary diagrams on the direct selling small cap companies.

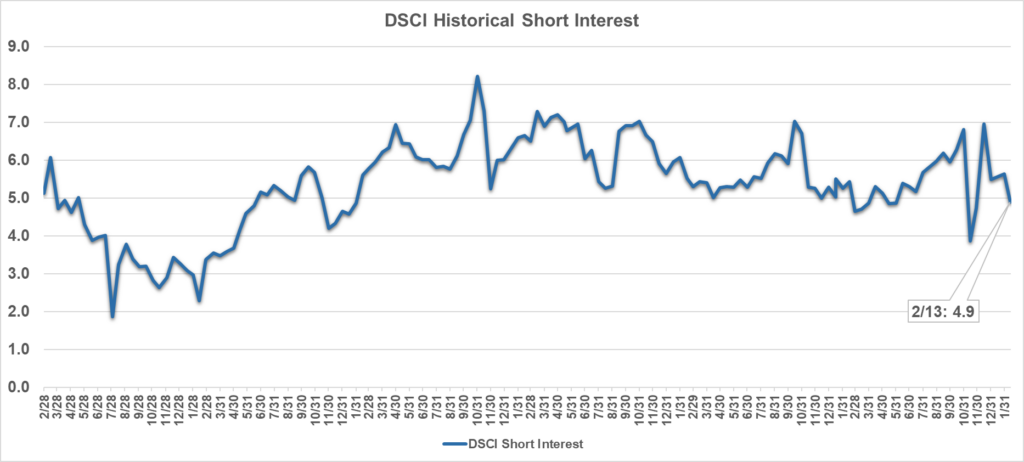

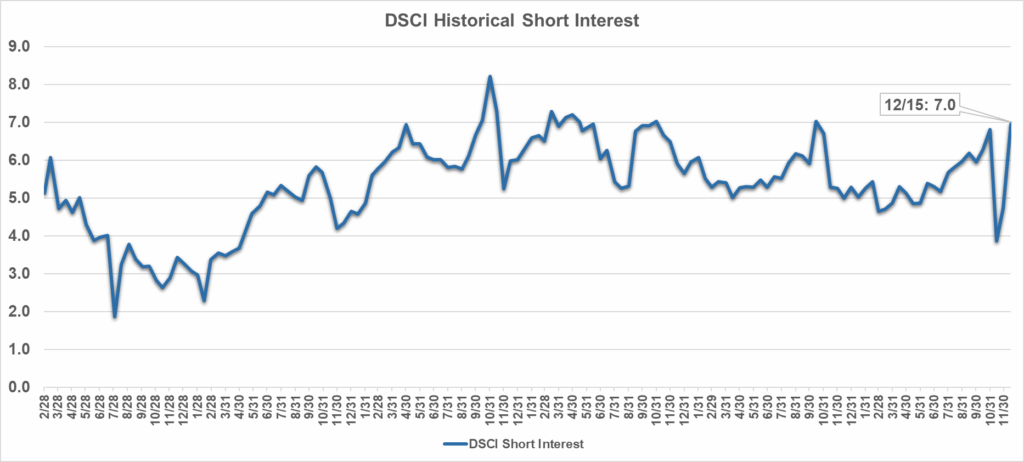

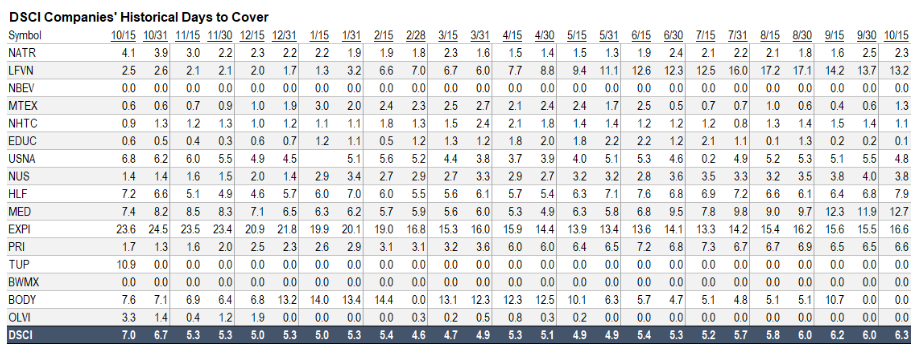

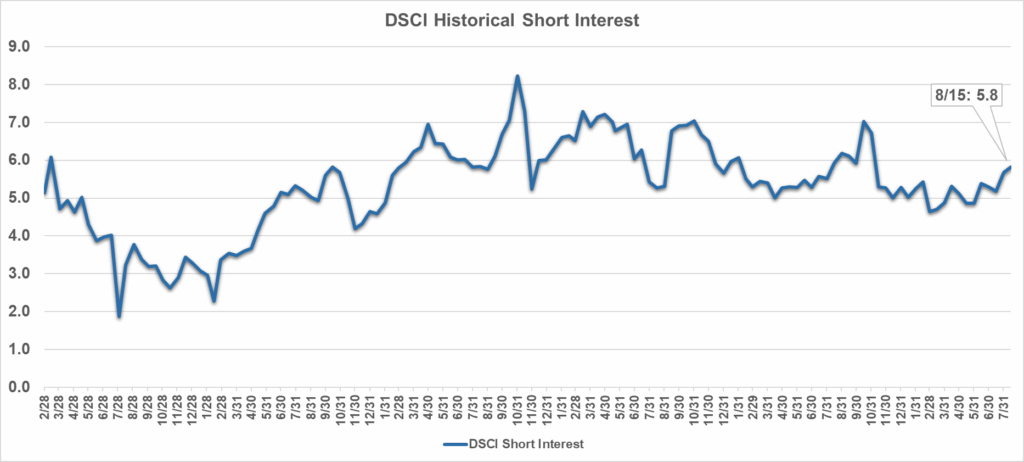

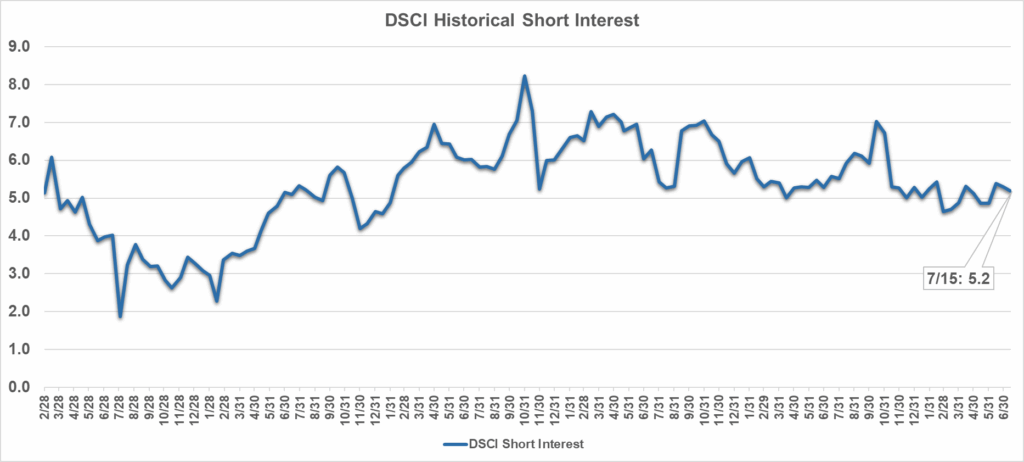

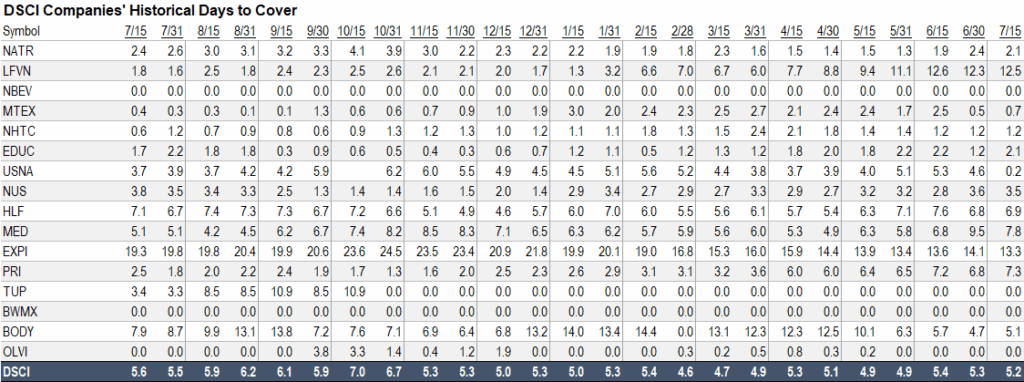

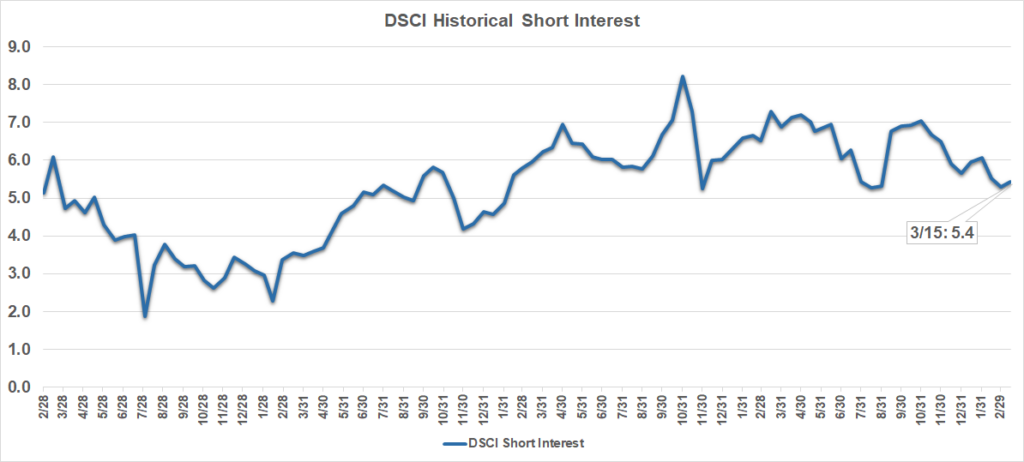

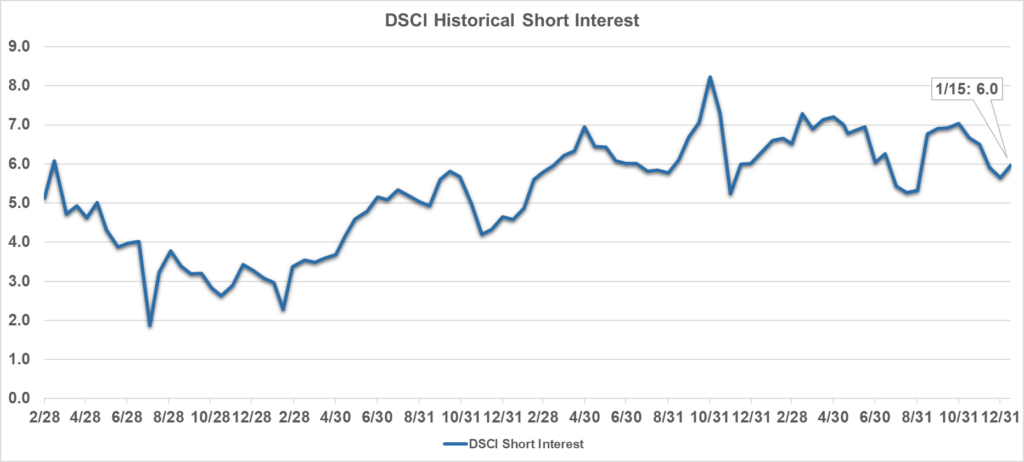

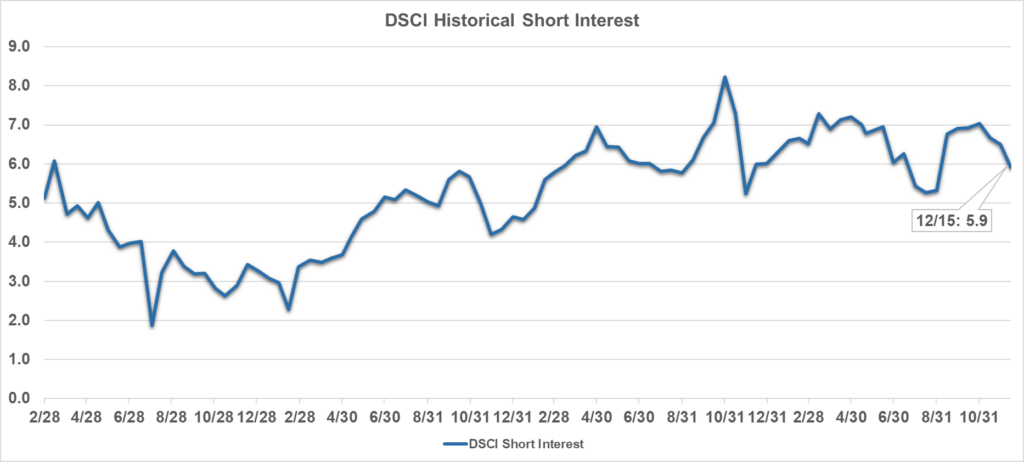

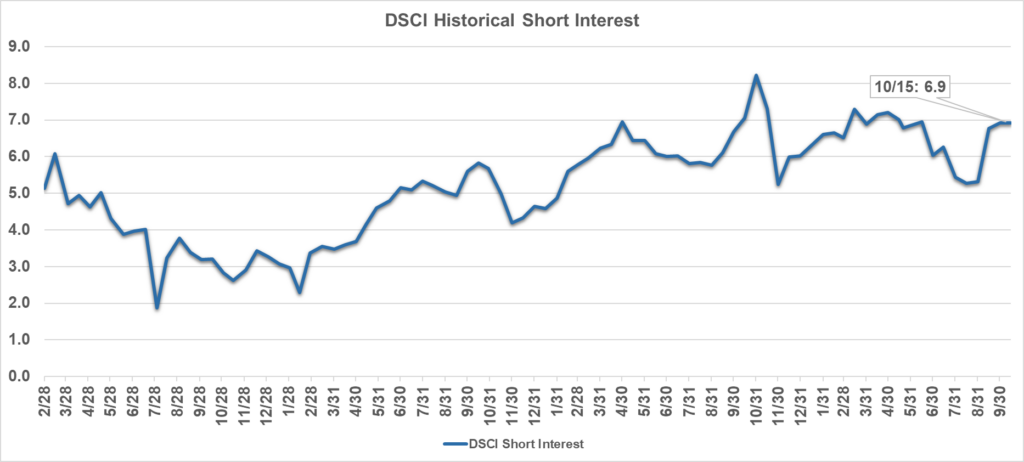

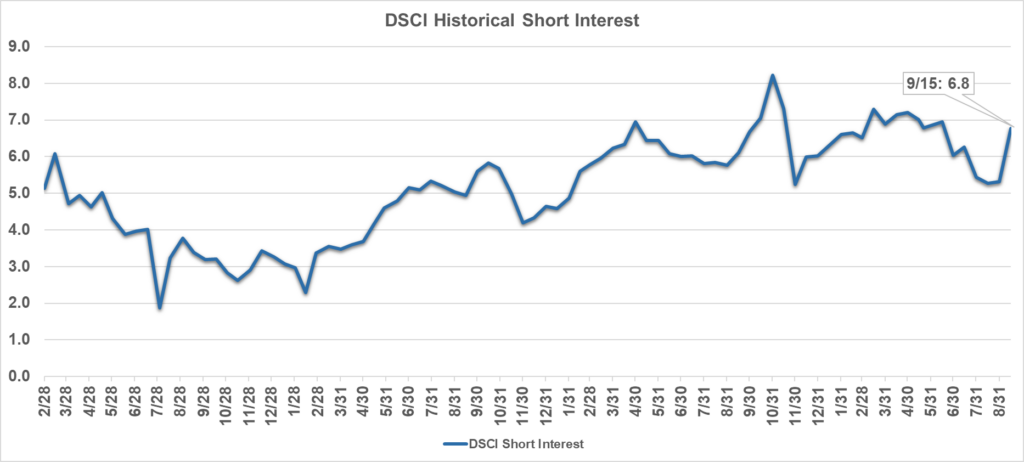

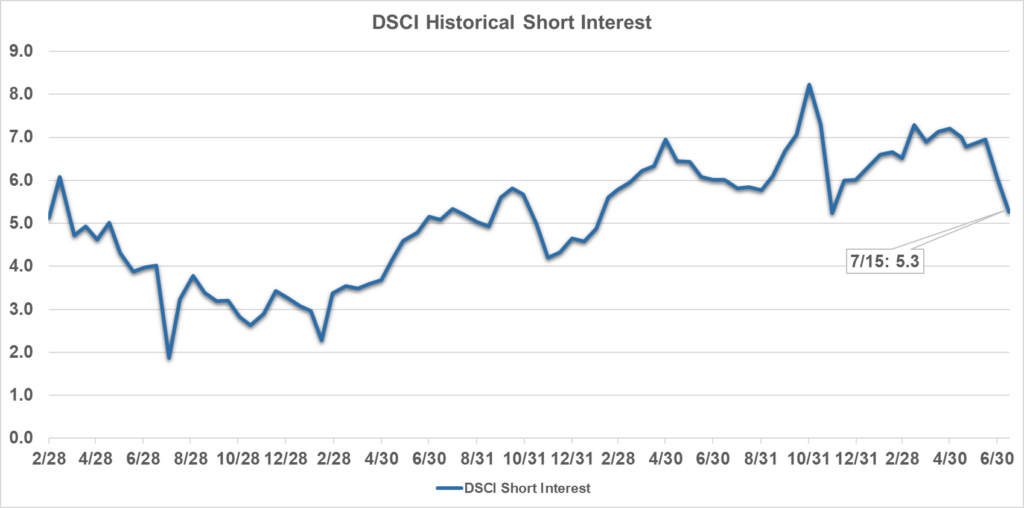

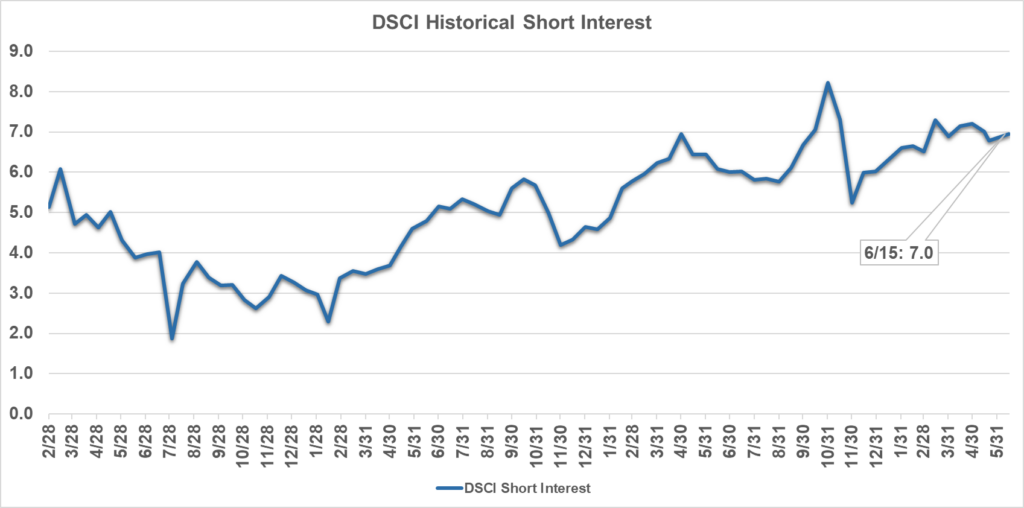

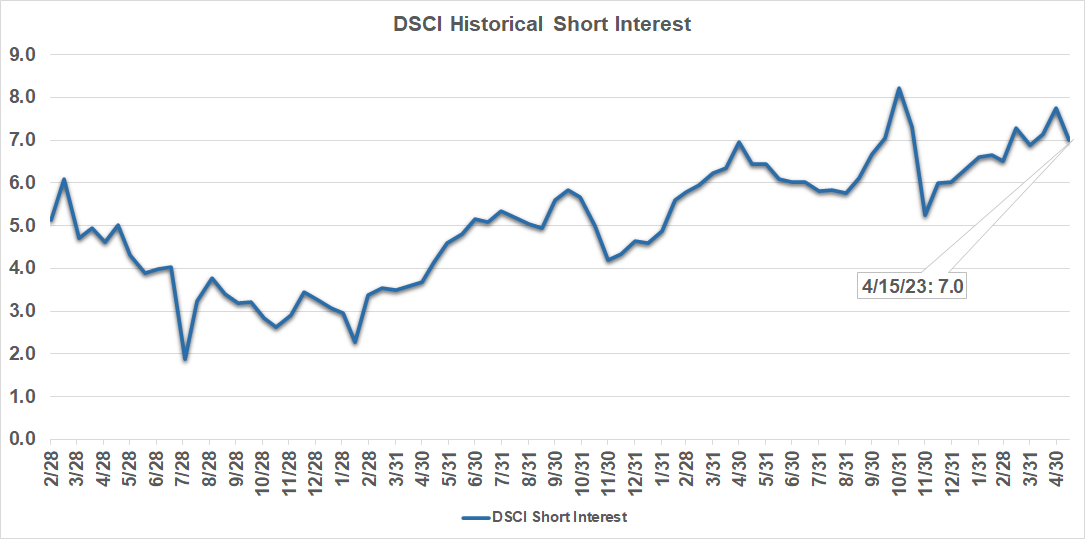

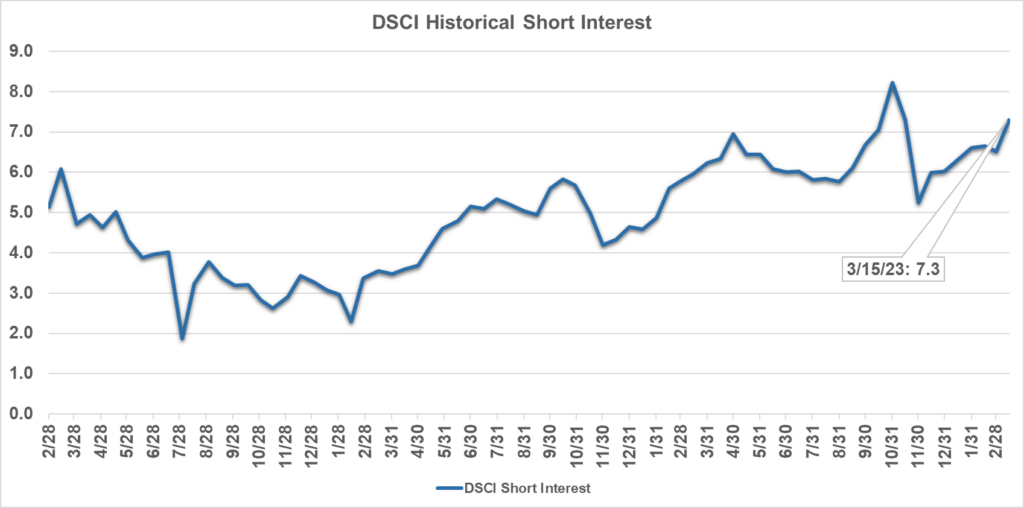

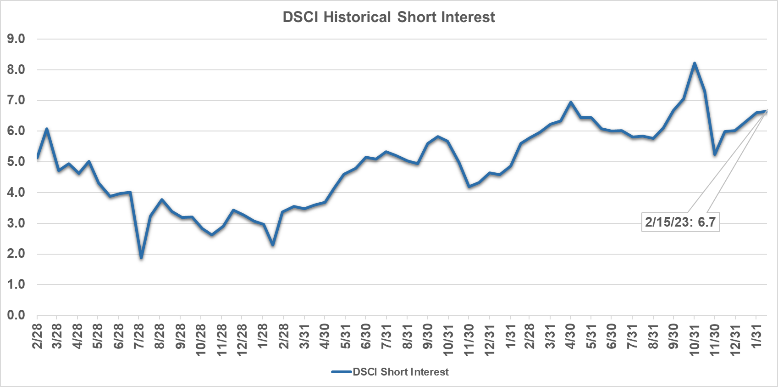

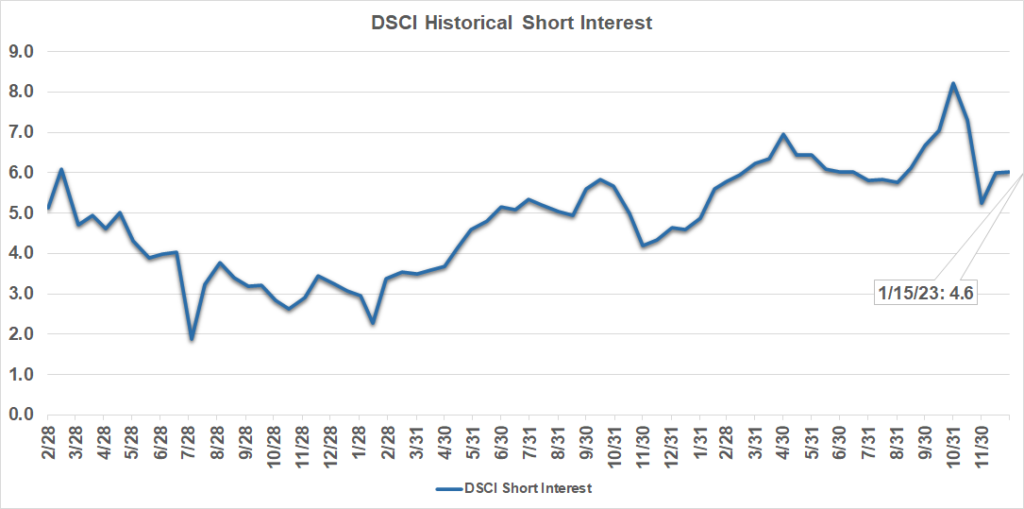

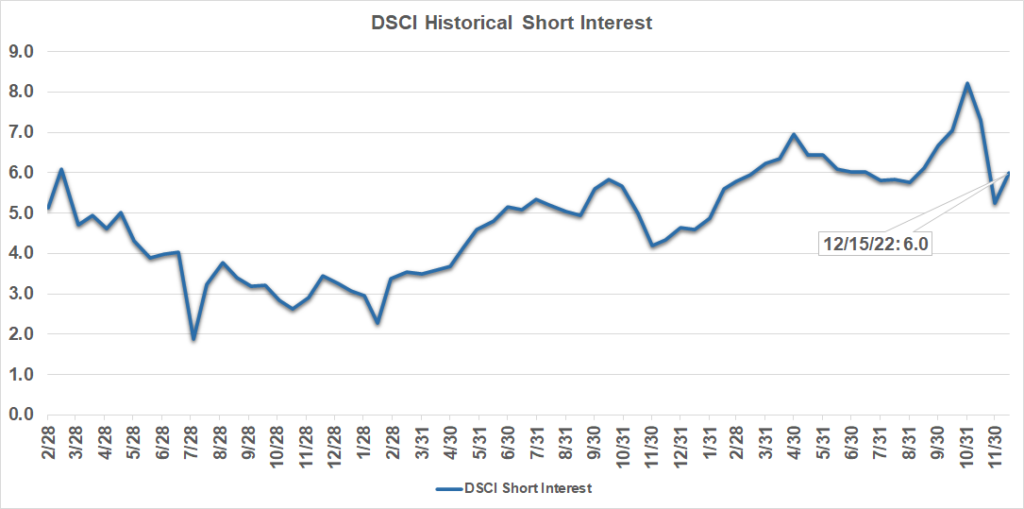

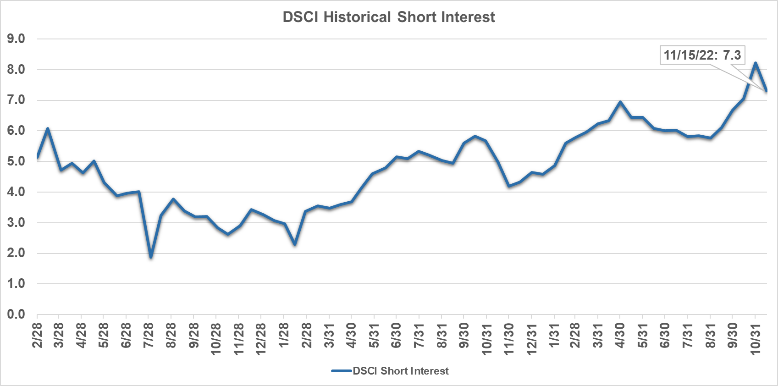

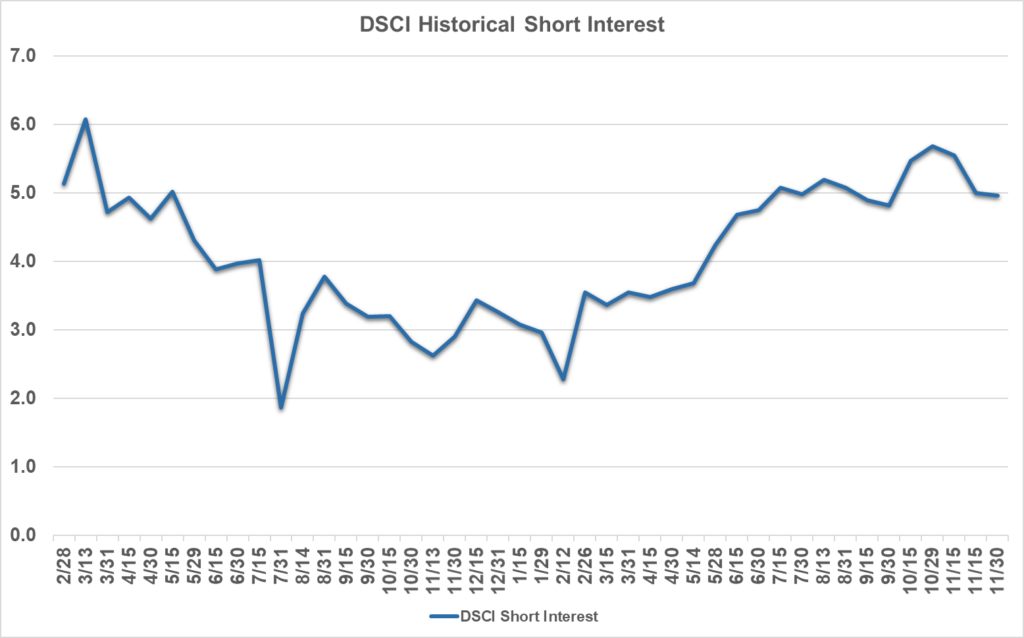

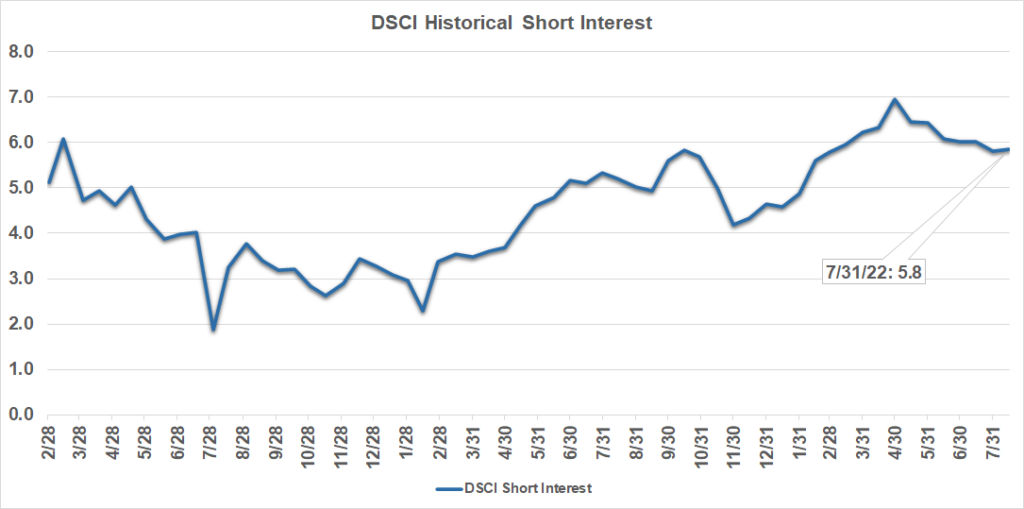

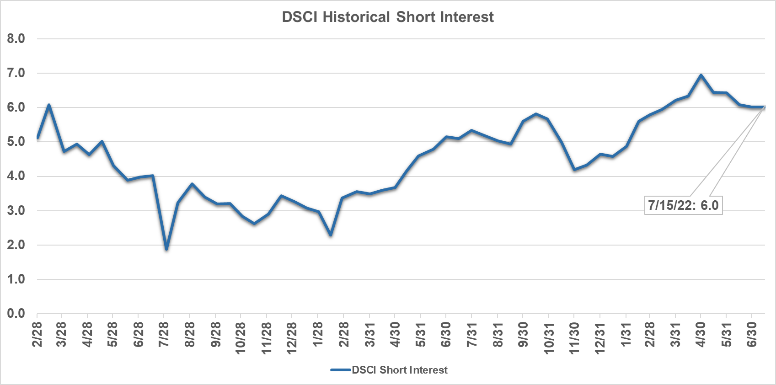

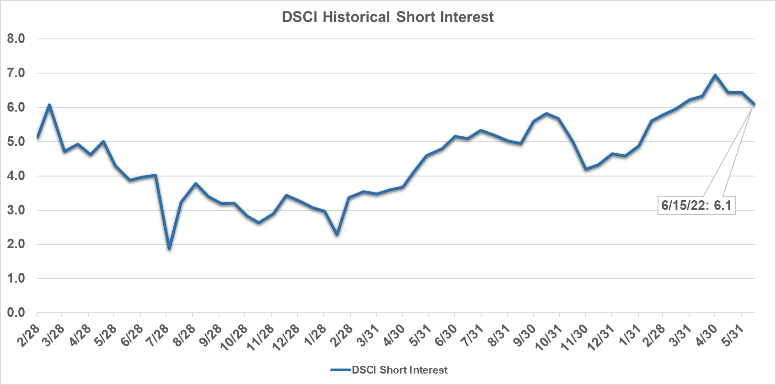

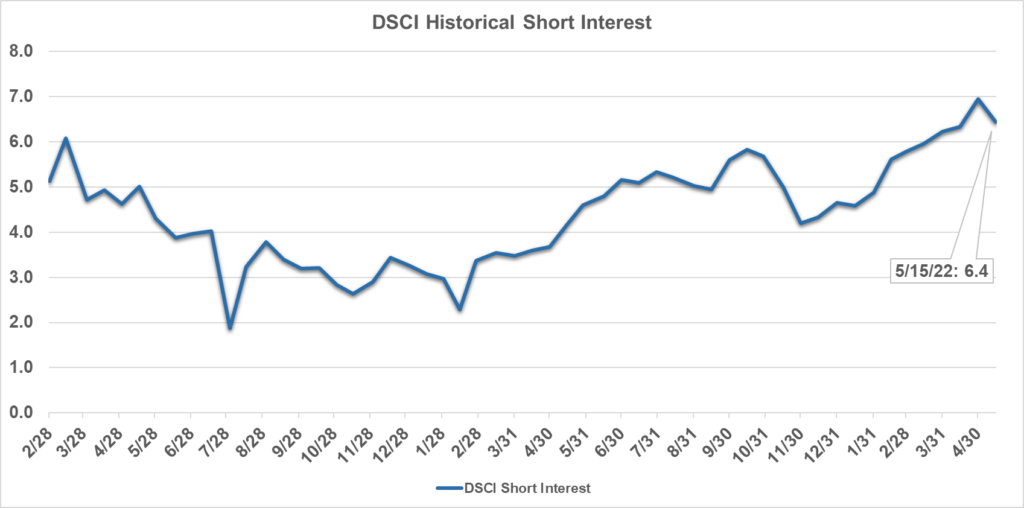

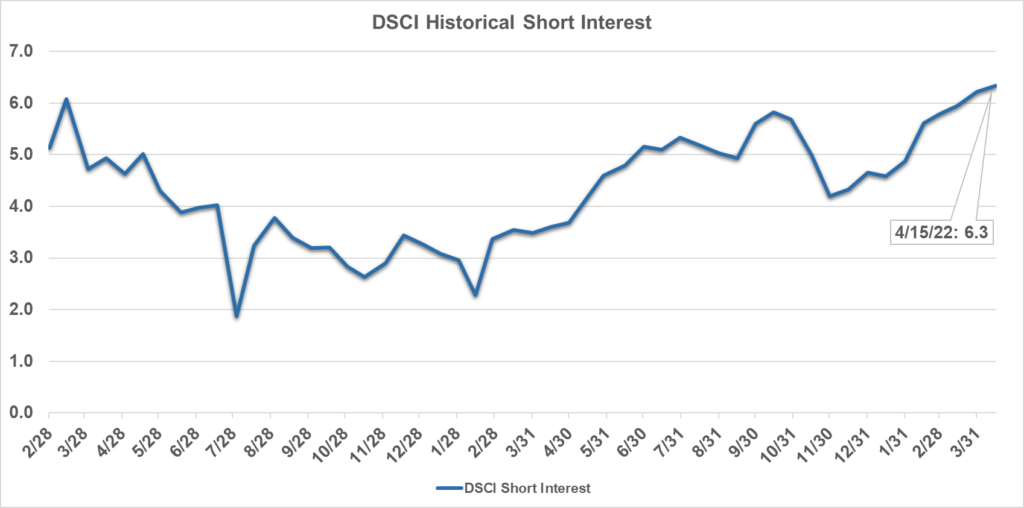

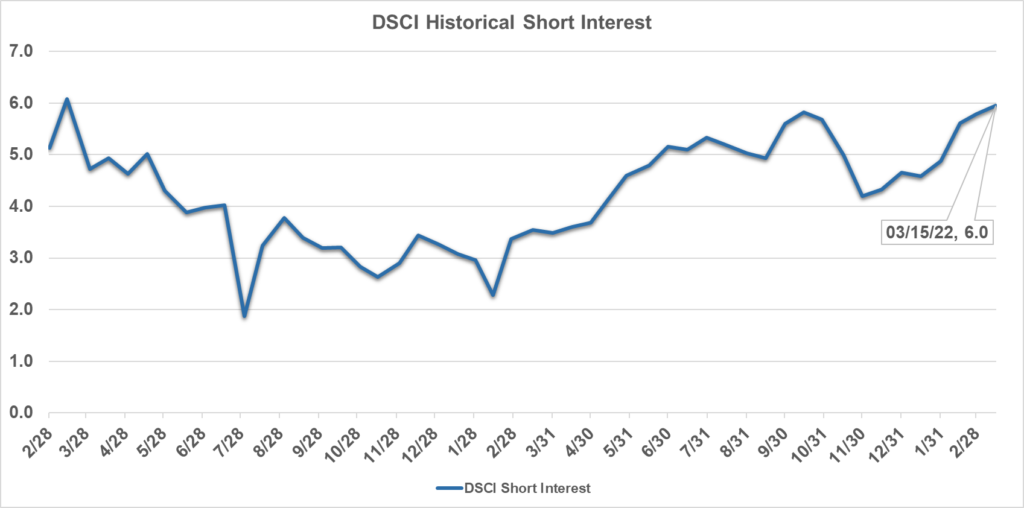

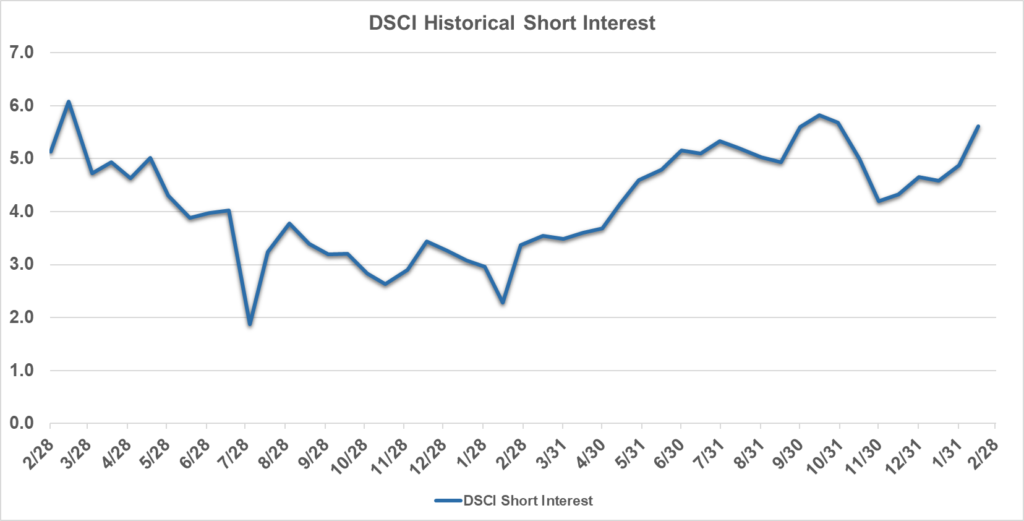

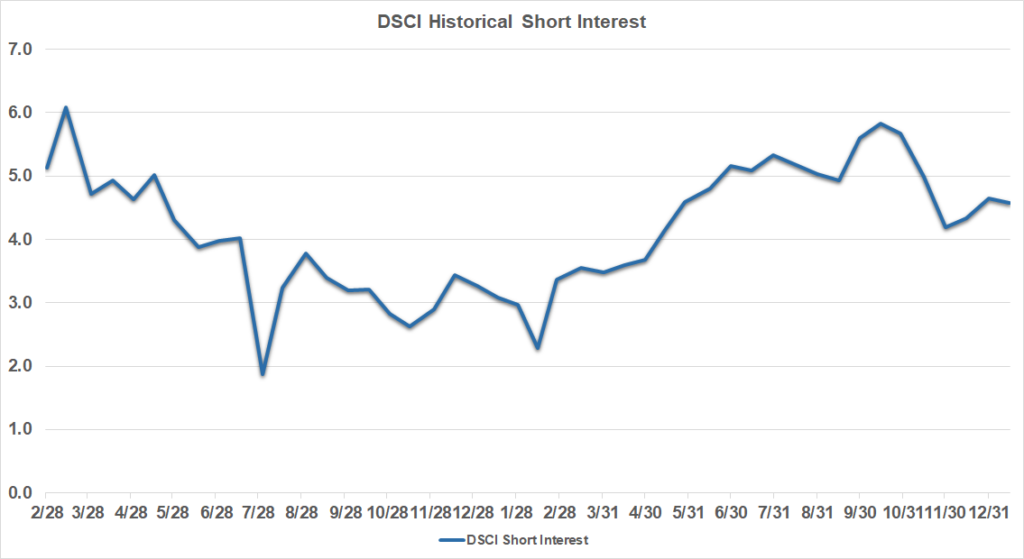

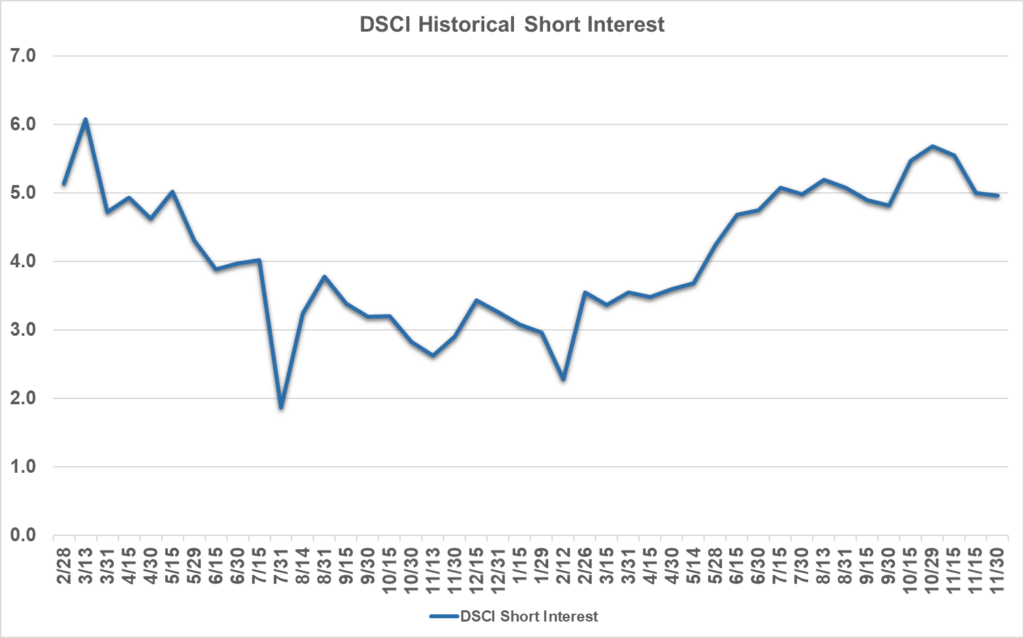

Short Interest Data & Analysis

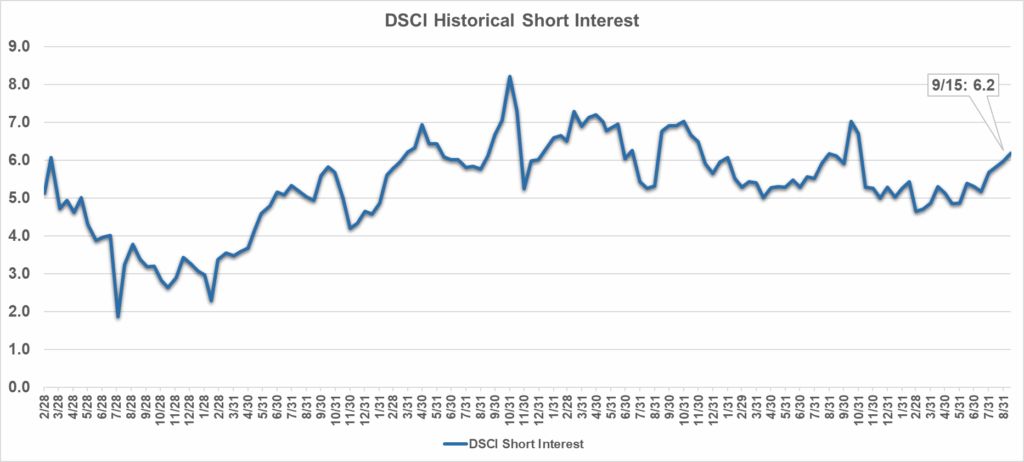

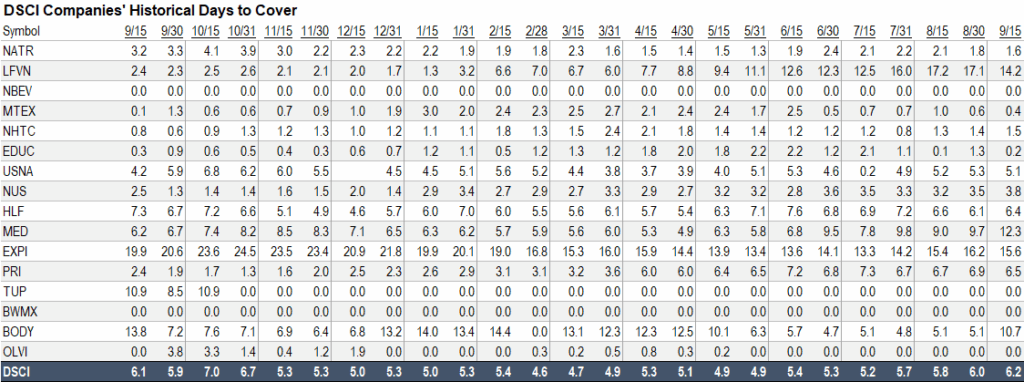

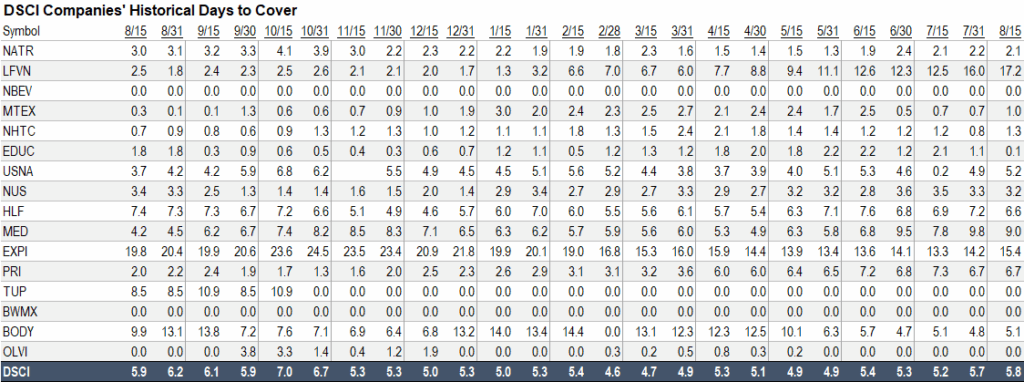

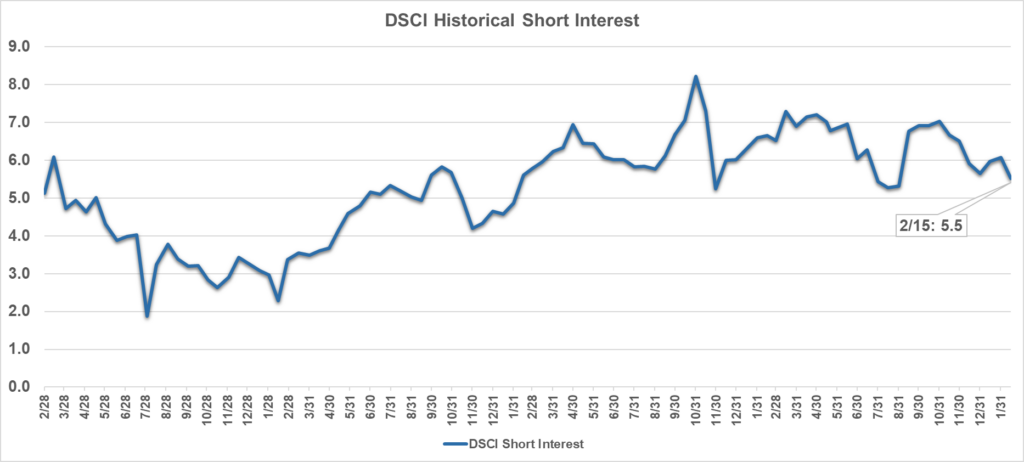

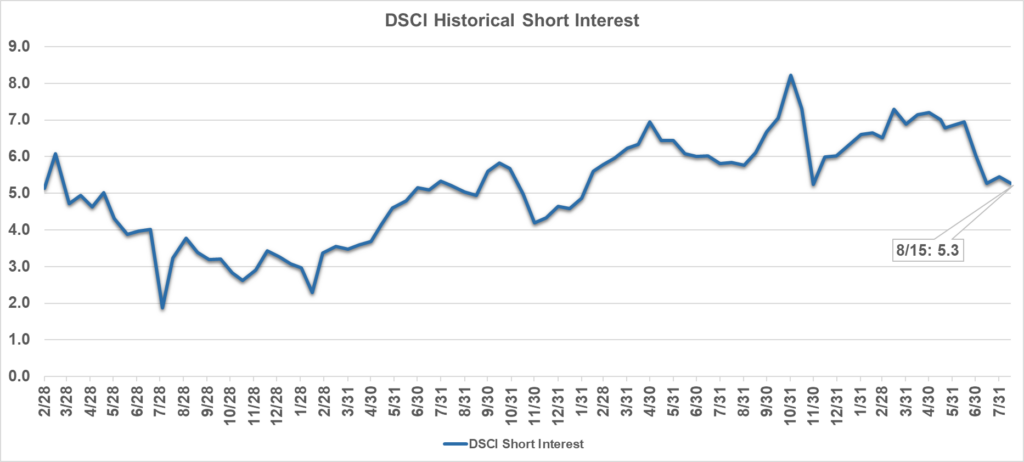

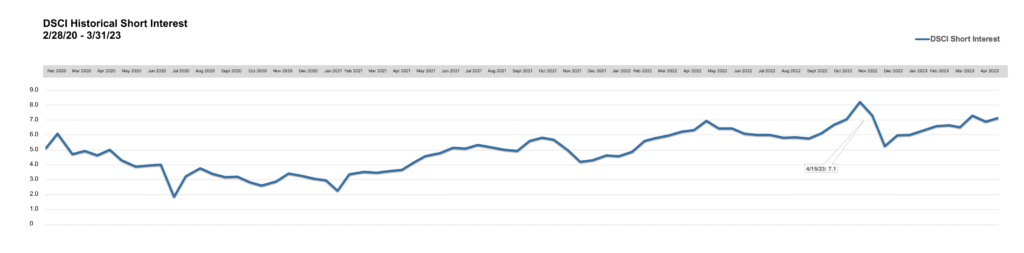

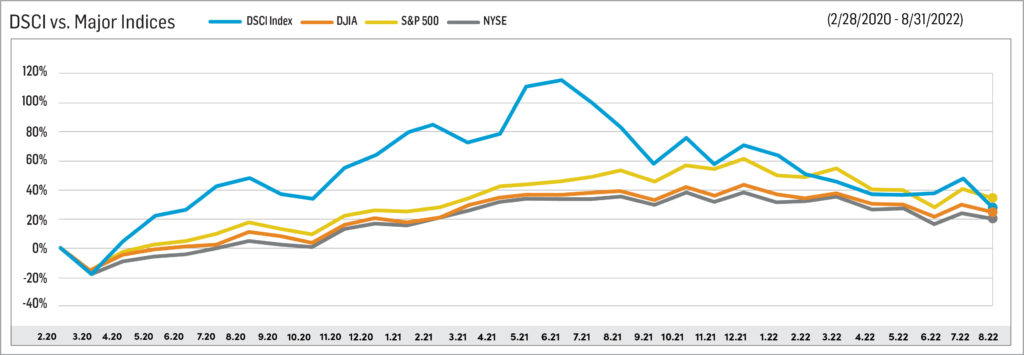

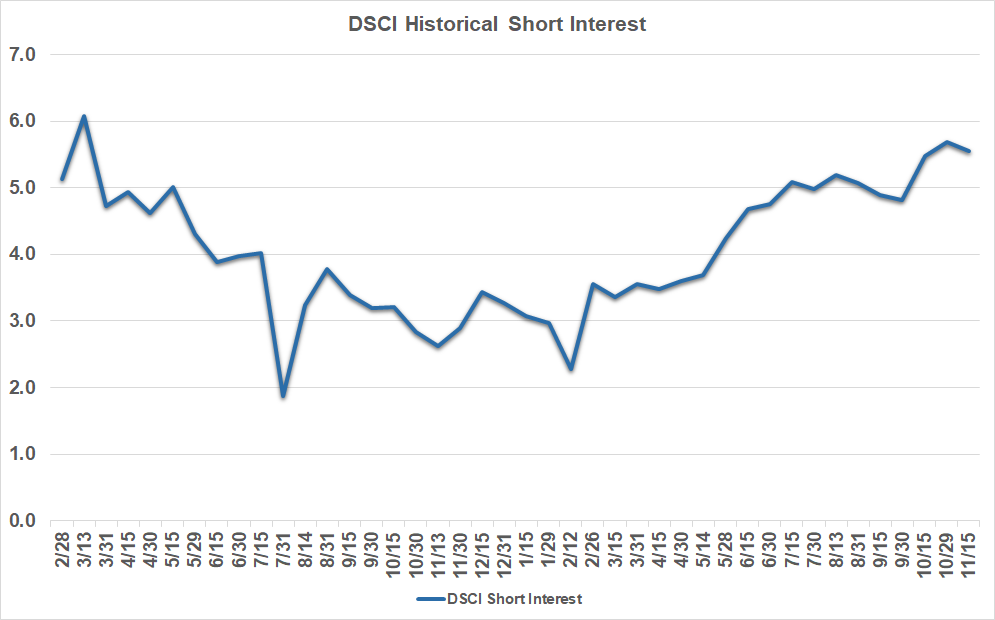

The following chart is an aggregate index of “days to cover” among the entire tracking set. Days to cover (DTC) is a measurement determined by dividing the total outstanding short interest by average daily trading volume.

As indicated in the chart, short interest in DSCI stocks was 4.9 days as of February 13, 2026. Short interest can be a difficult indicator to analyze. On the one hand, an increase in short interest can be a bearish sign in that it indicates an increased view among investors that a stock is likely to decline based on any number of factors, such as a belief that the company’s fundamentals are deteriorating or that it has run too far, too fast. On the other hand, as a stock moves higher, a significant short interest can serve as extra fuel on the fire as investors scramble to “buy to cover” their short positions and mitigate losses.

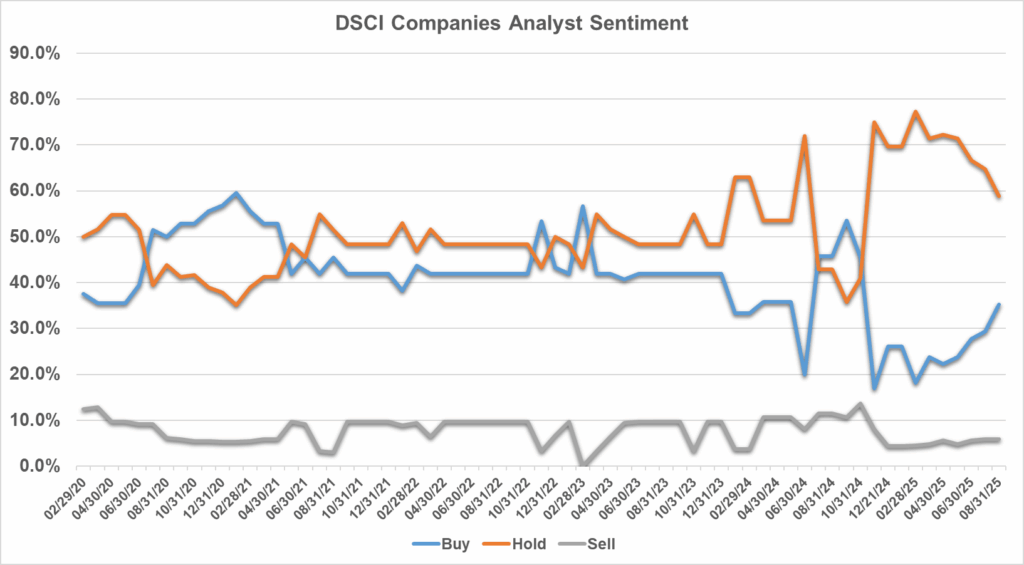

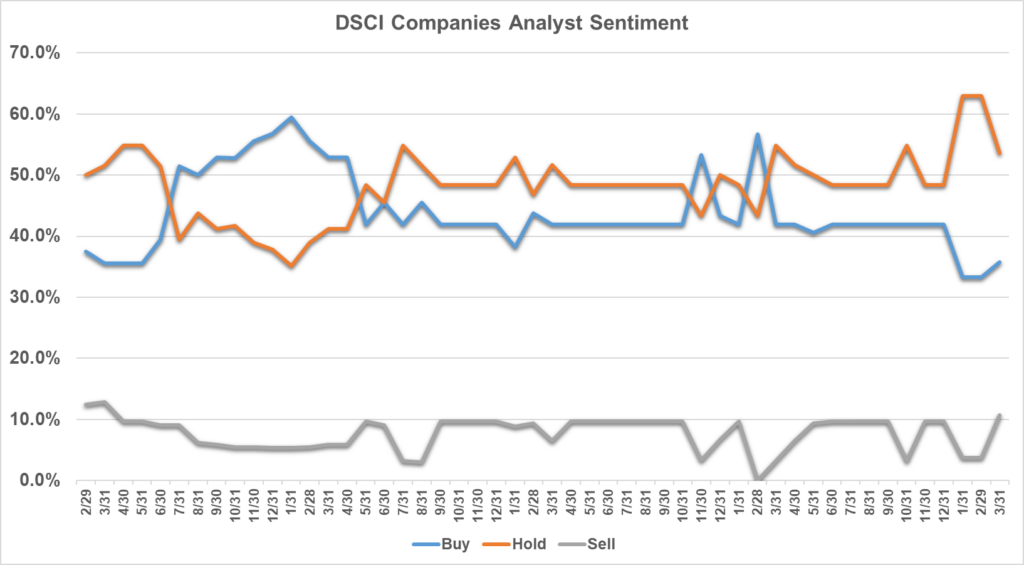

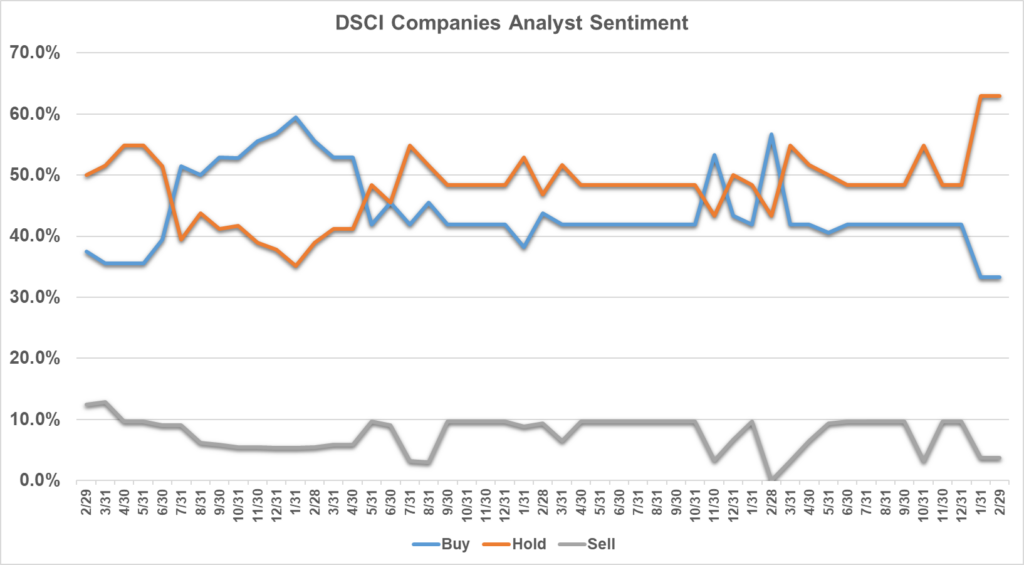

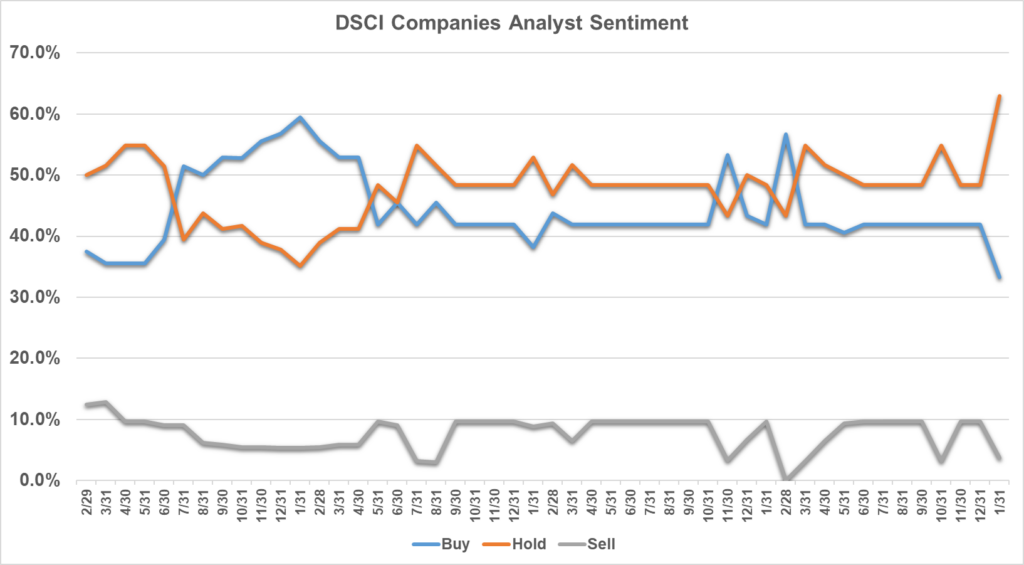

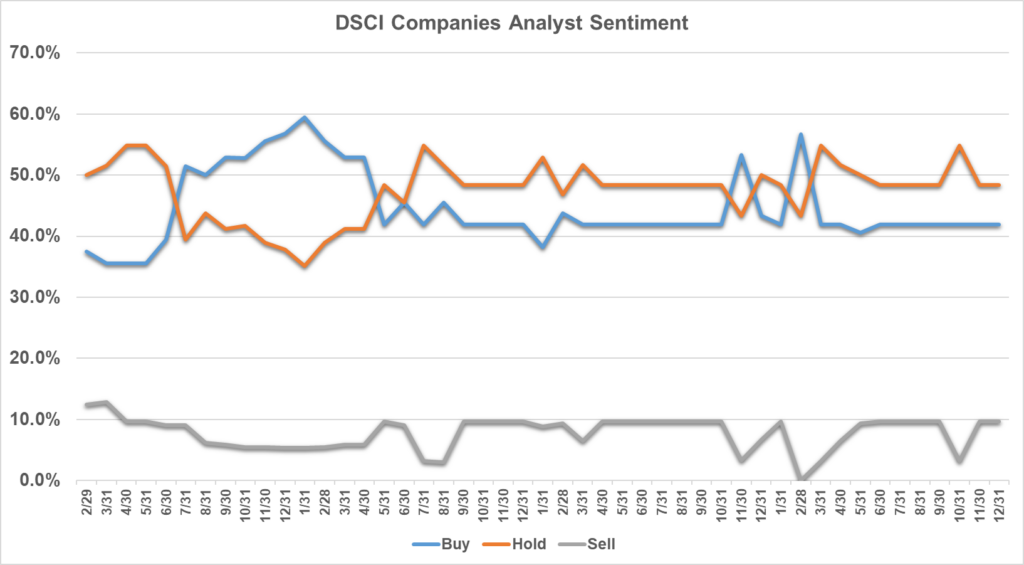

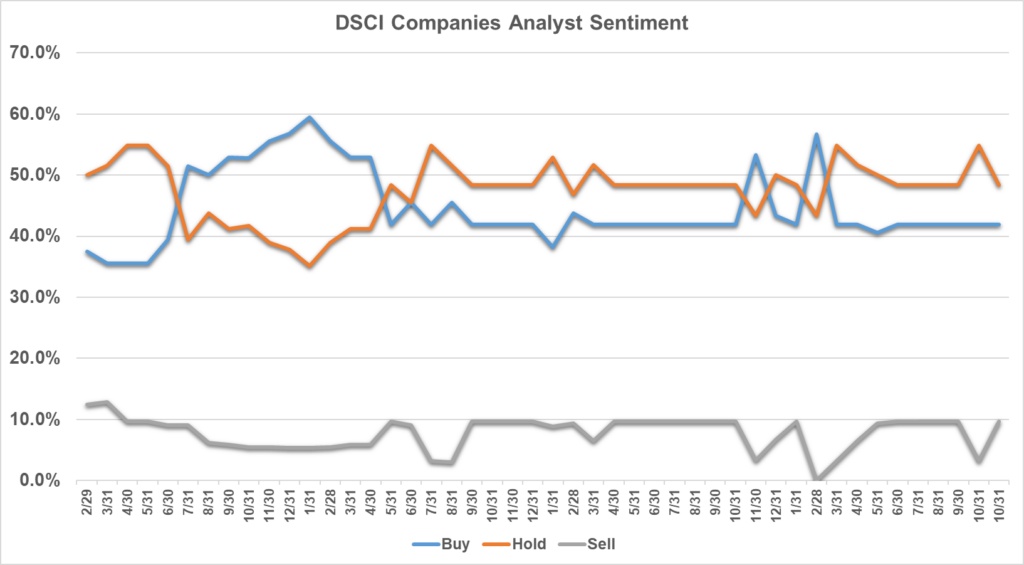

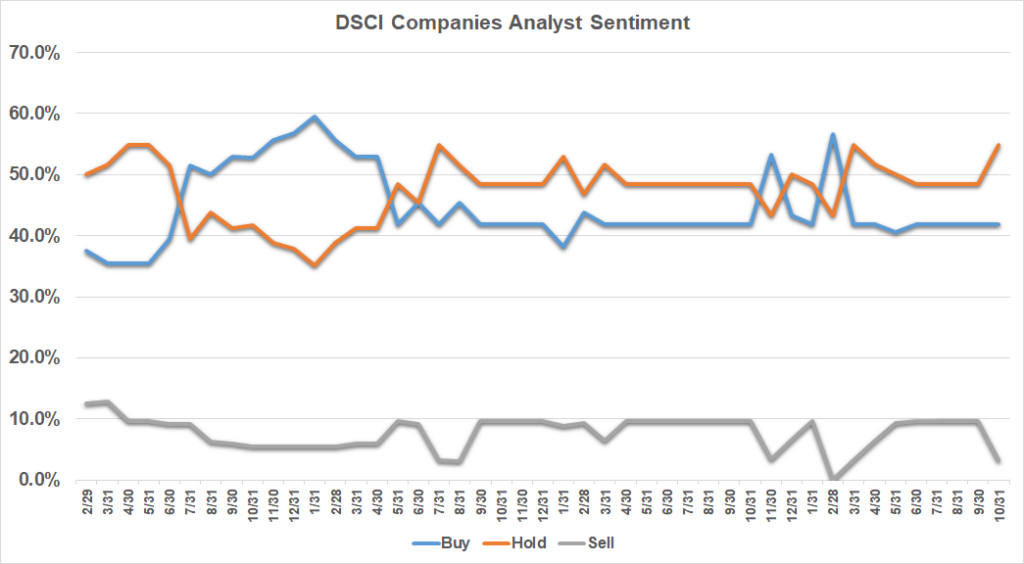

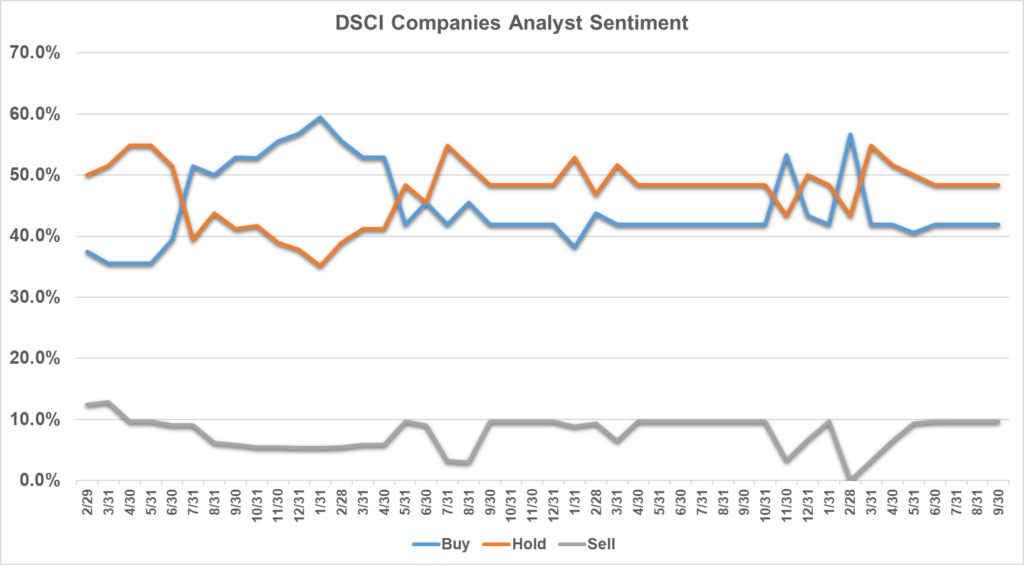

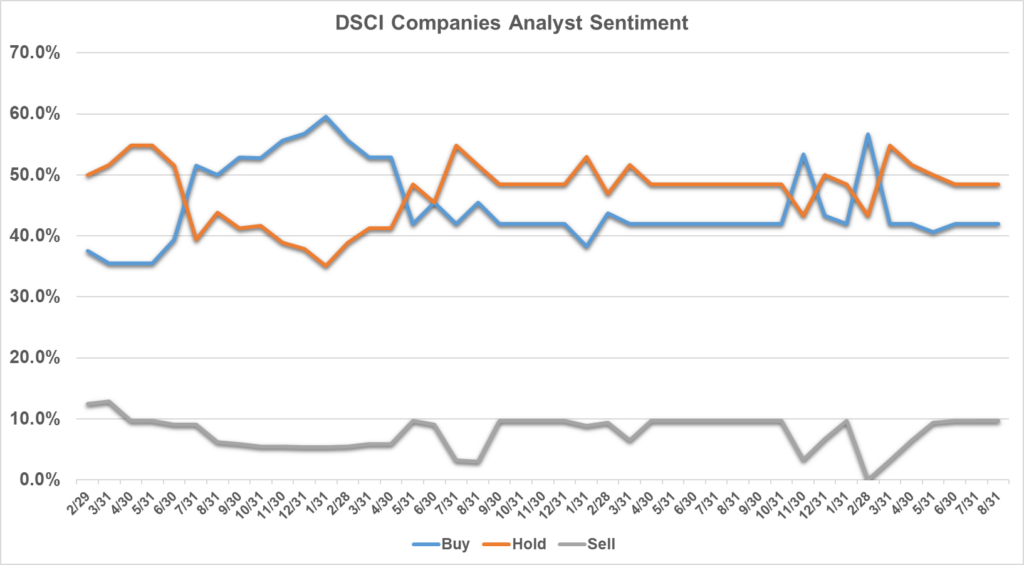

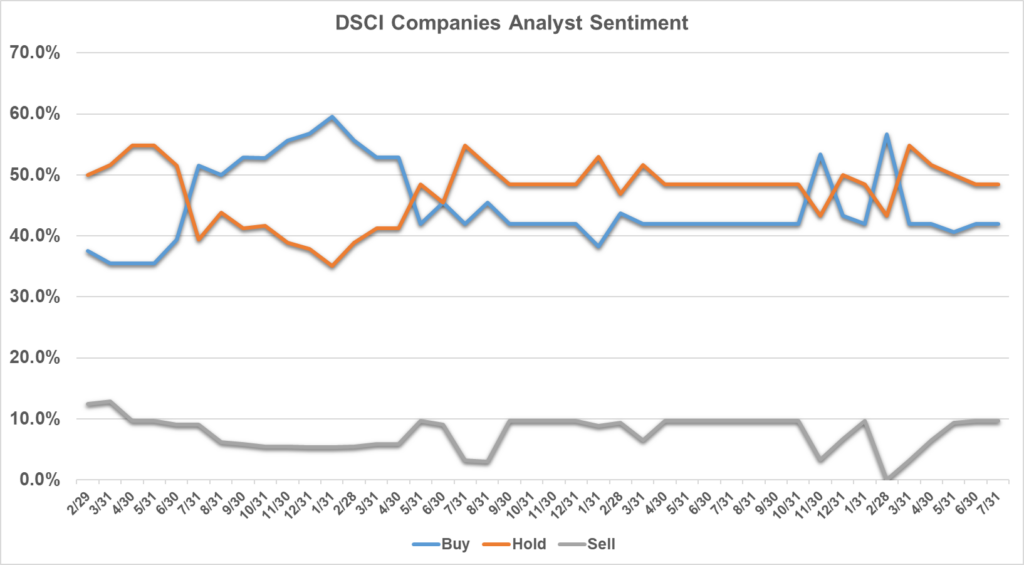

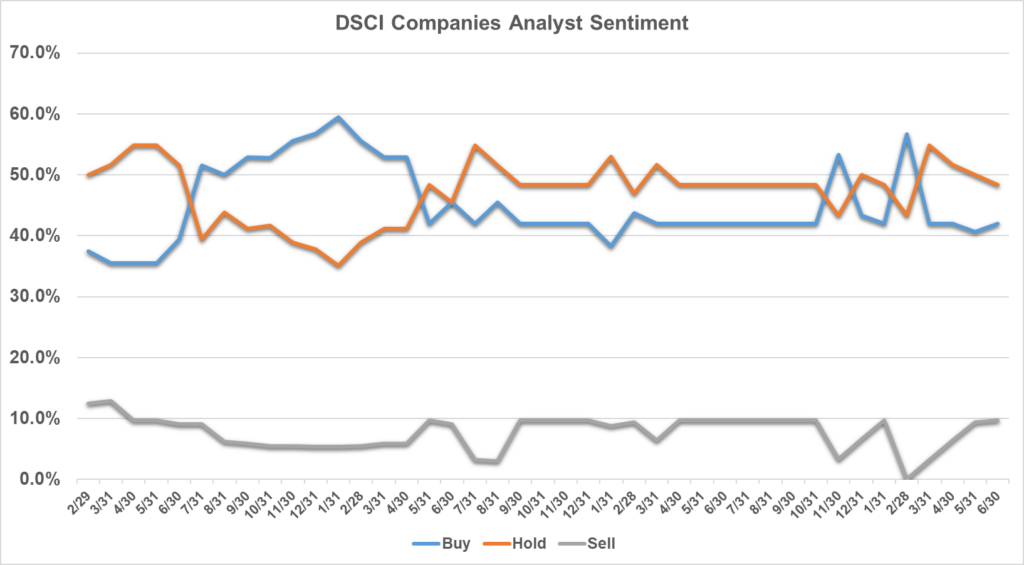

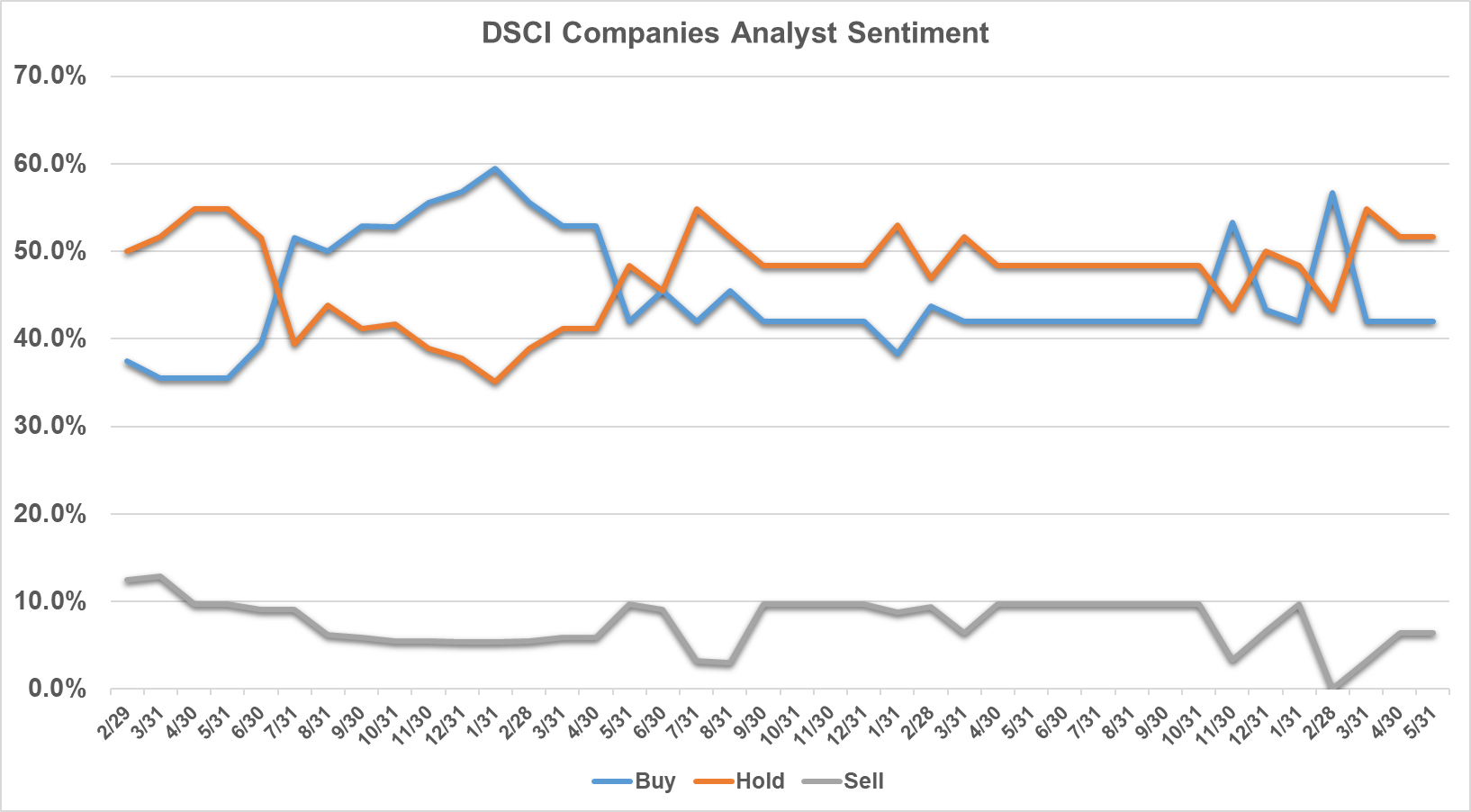

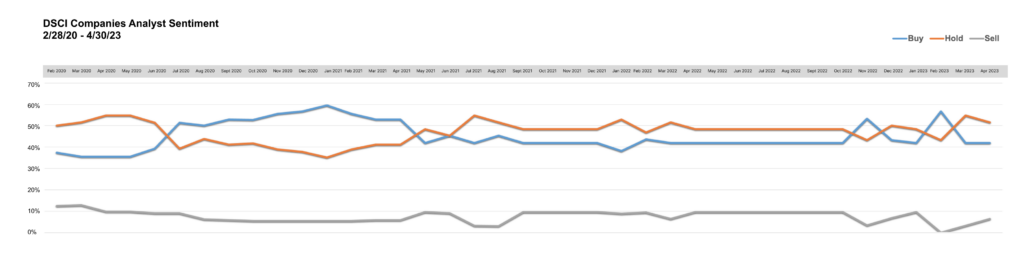

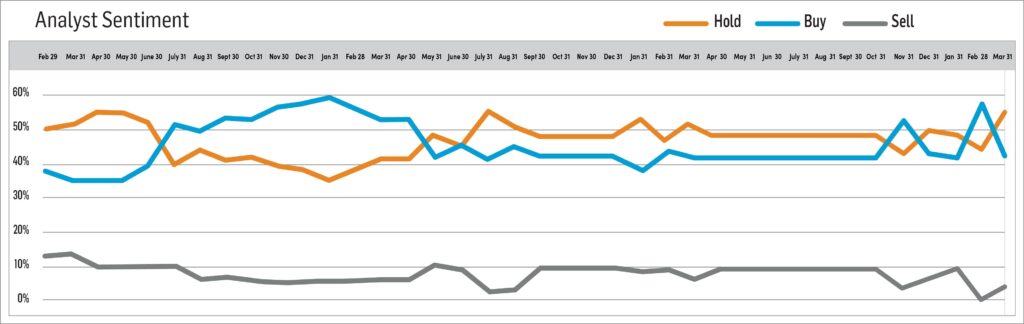

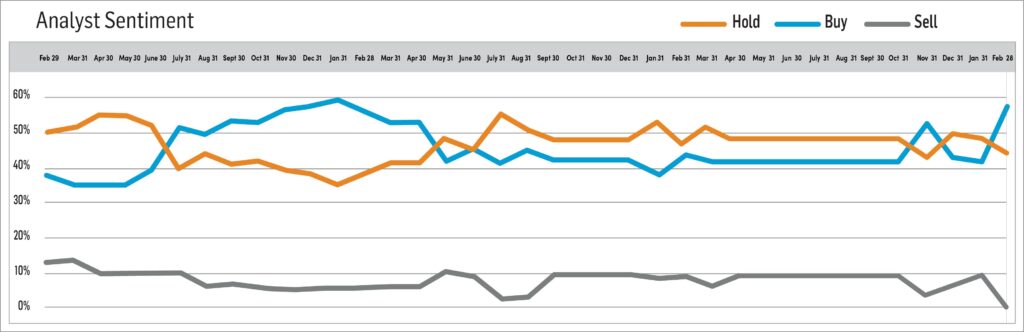

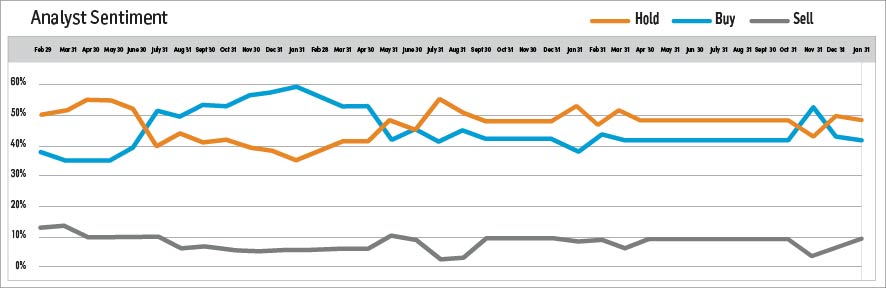

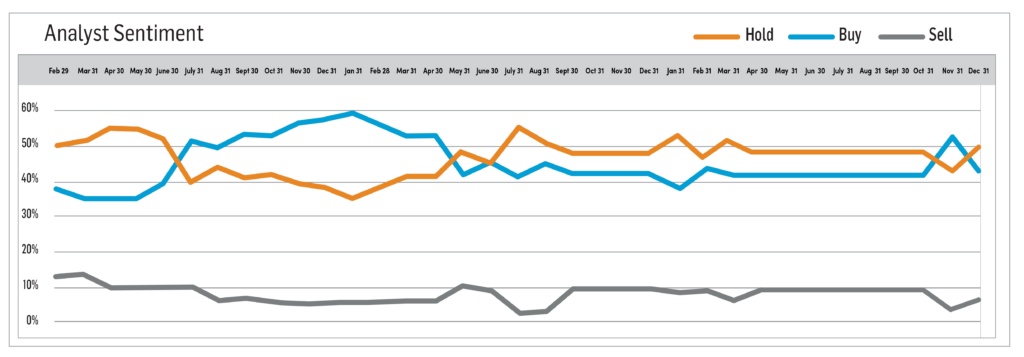

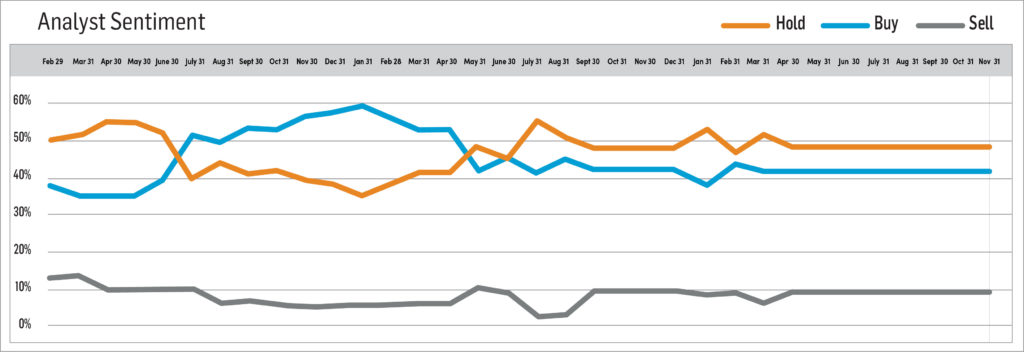

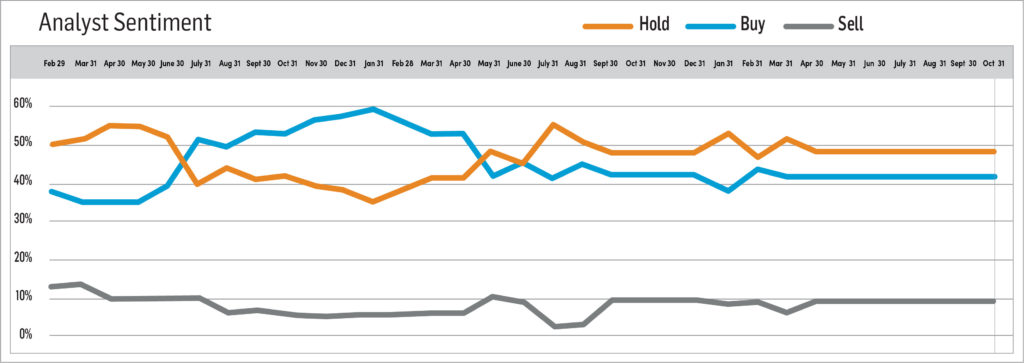

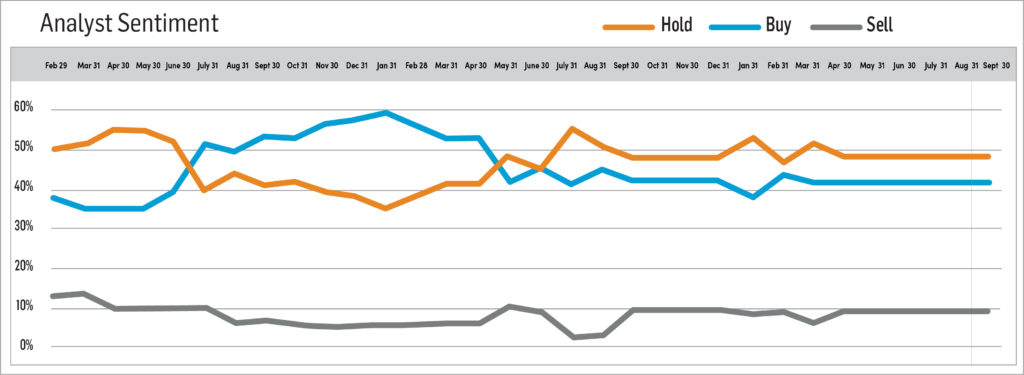

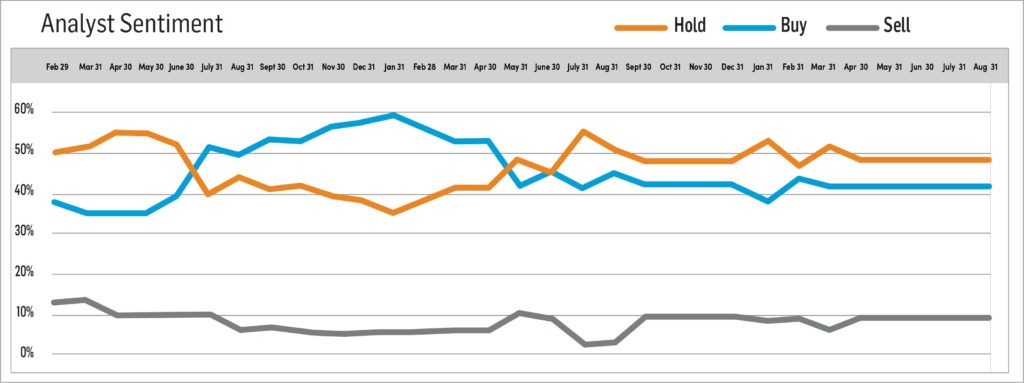

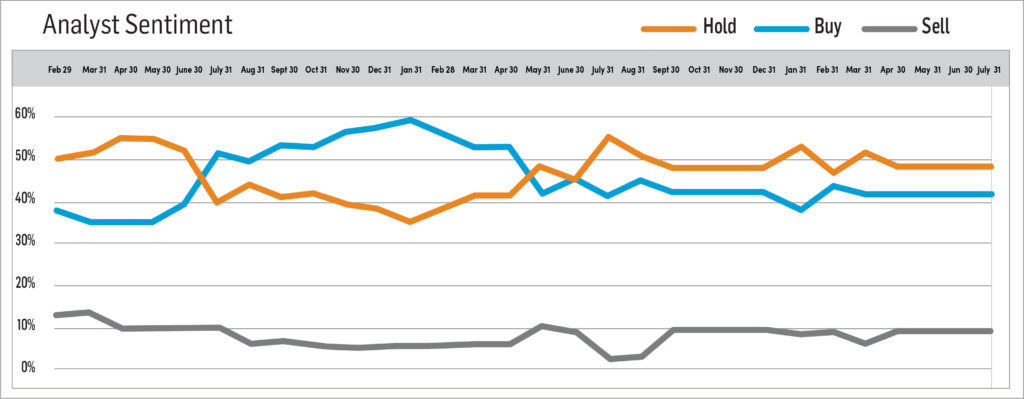

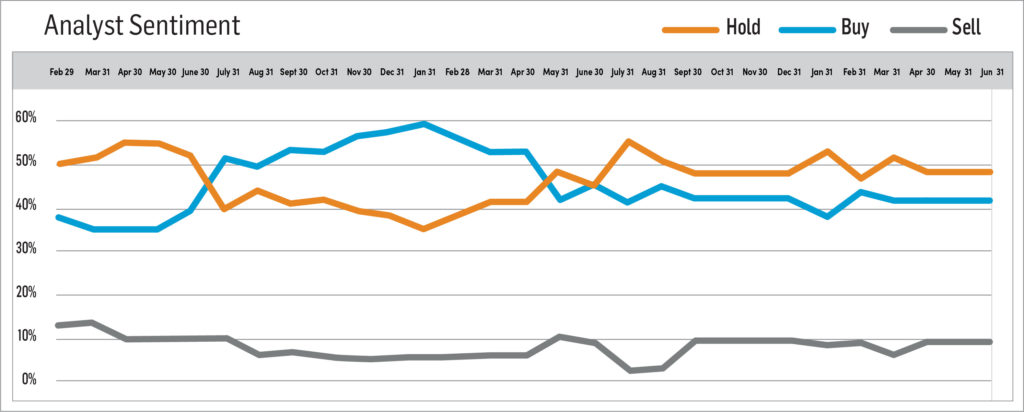

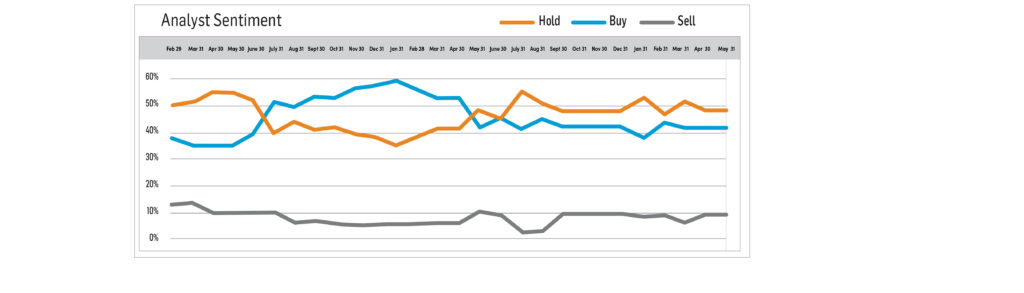

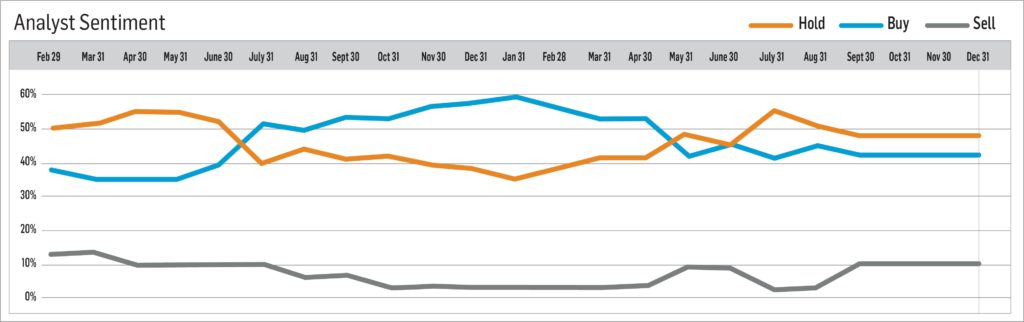

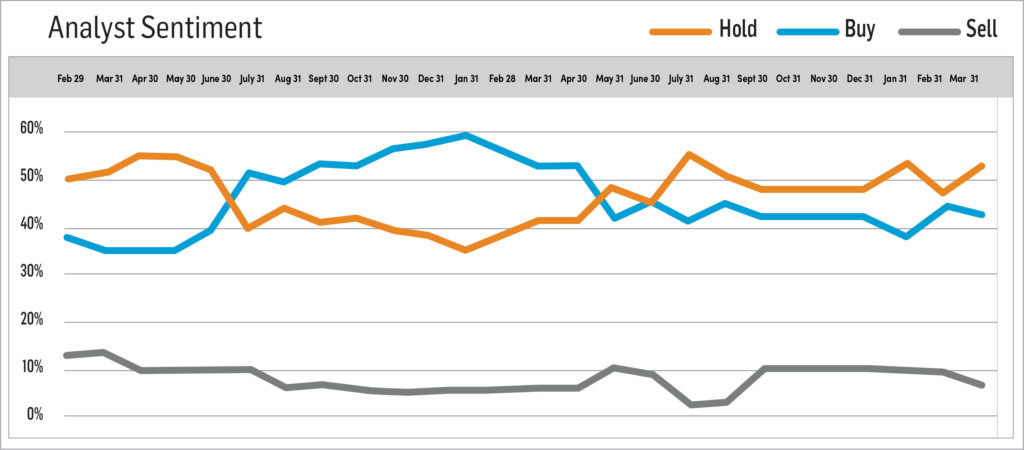

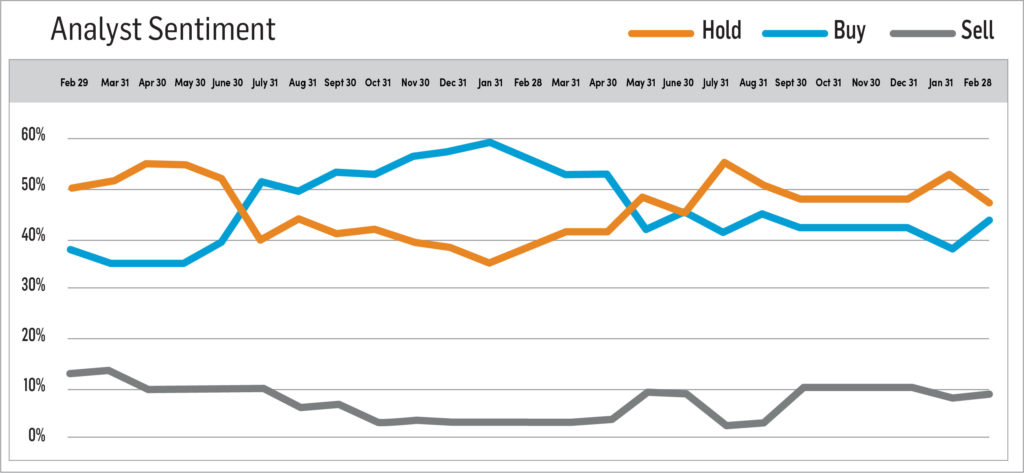

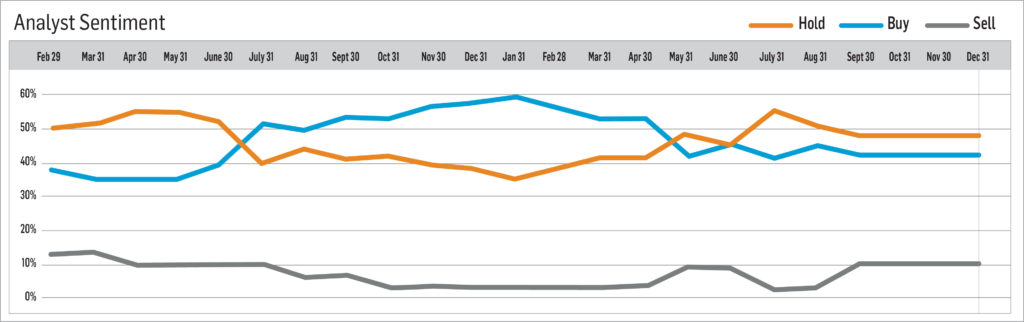

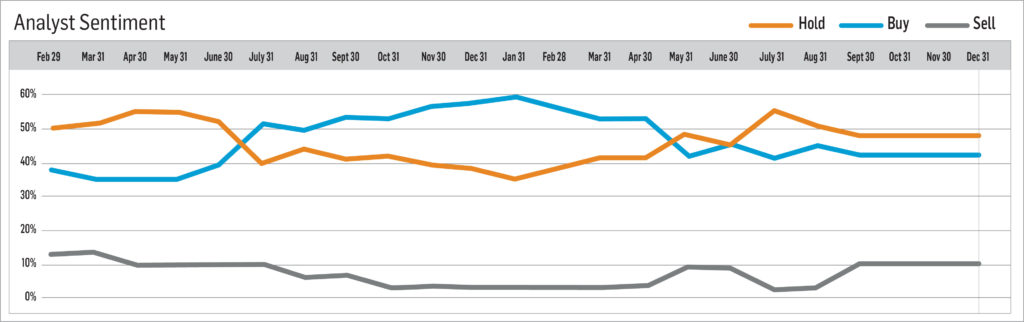

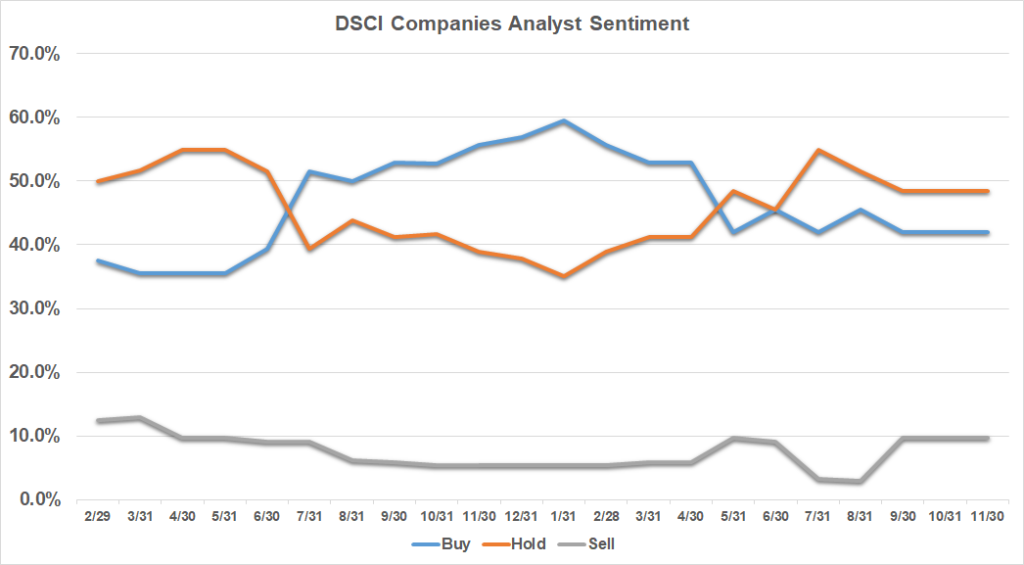

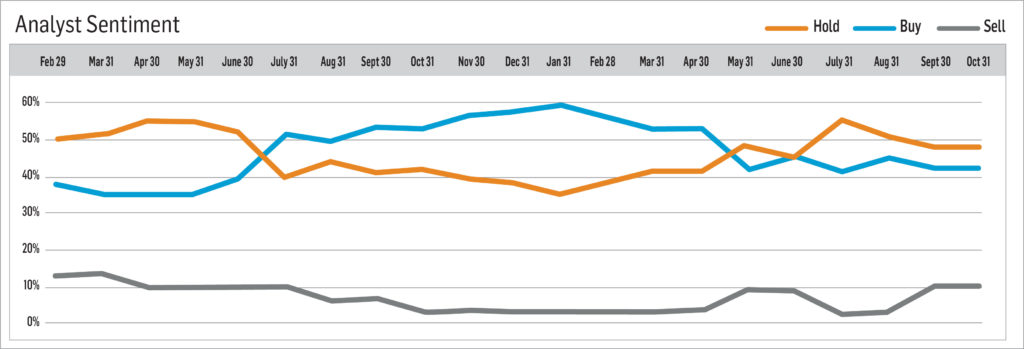

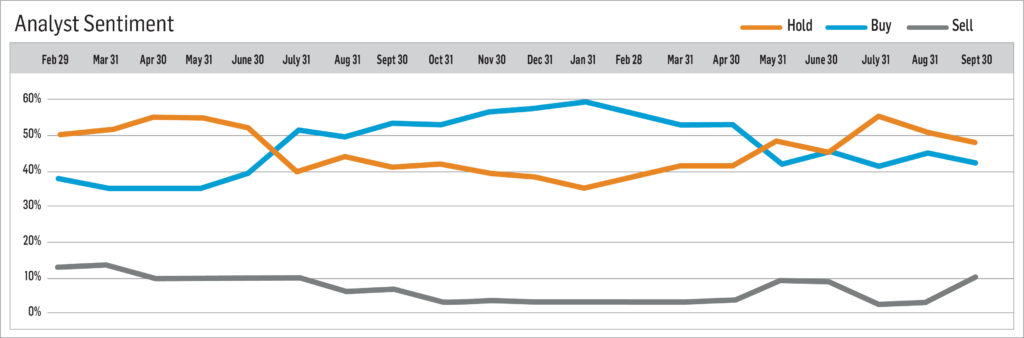

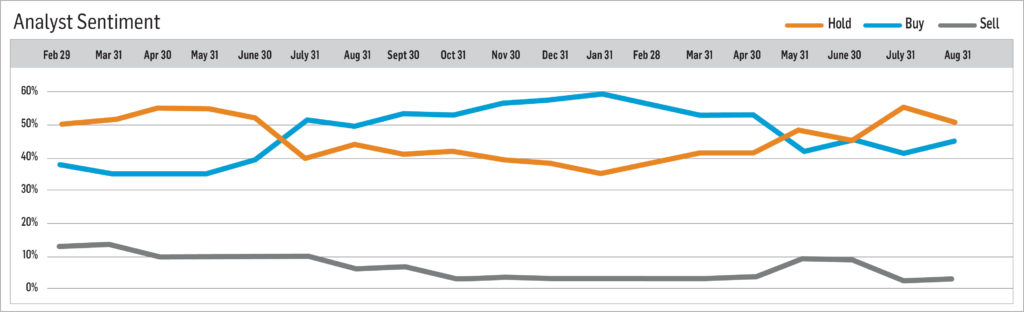

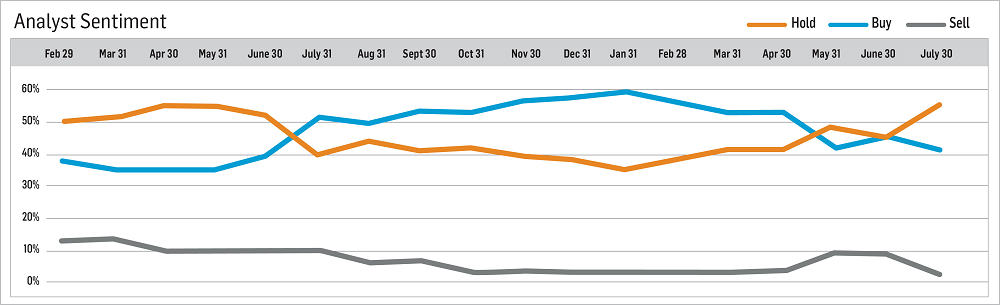

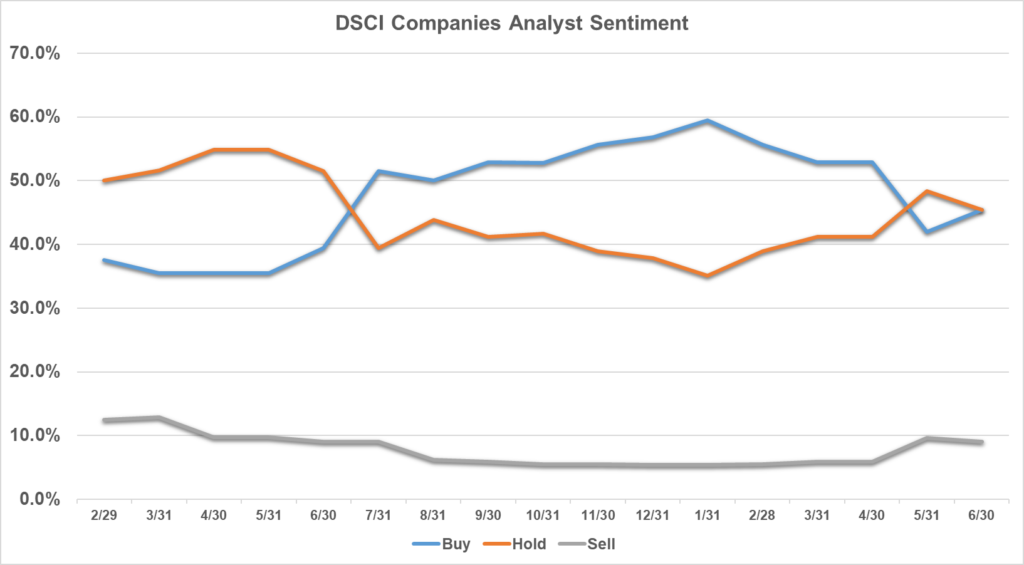

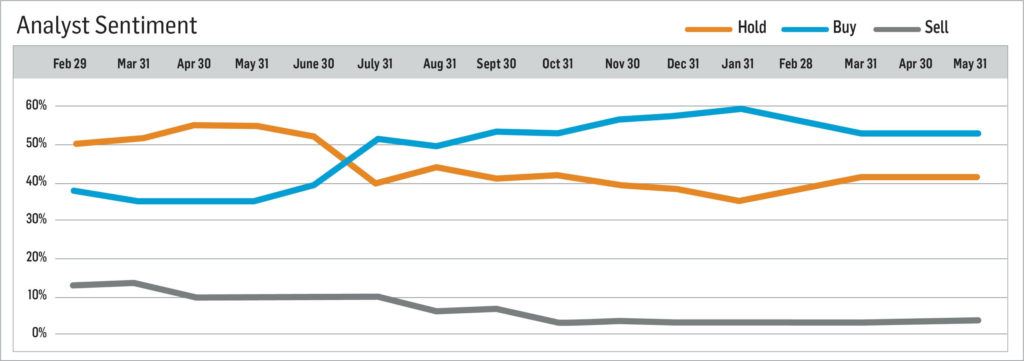

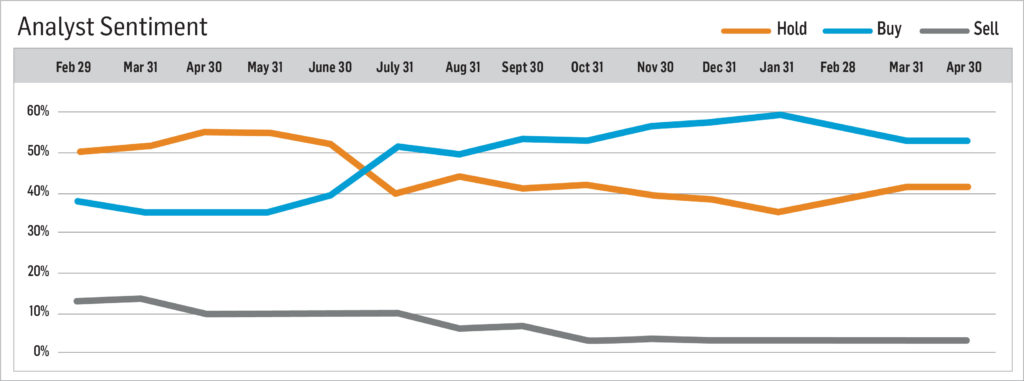

Analyst Sentiment Index

The DSCA Analyst Sentiment Index is a consensus tracking tool that aggregates and averages the recommendations of all covering analysts across all public direct selling companies.

-

January 2026

Brought to you by Direct Selling Capital Advisors

Direct Selling Index Mirrors the DJIA for the Month of January 2026

The Direct Selling Capital Advisors Direct Selling Index (DSCI) increased by 1.7% in January compared to December 2025. The DJIA increased by 1.63% over the same period. Over the first month of 2026, the DSCI recorded a modest increase of 1.7%. When comparing the DSCI to the DJIA since the inception of the DSCI, the DSCI’s cumulative return is 92.4%.

Market and Economic Environment

US equity markets opened 2026 with cautious optimism, delivering modest gains amid continued macroeconomic uncertainty. January trading was characterized by intermittent volatility as investors balanced expectations of potential Federal Reserve rate cuts later in the year against persistent inflation concerns and geopolitical developments. Despite several risk-off episodes during the month, major indices largely ended January slightly higher, supported by selective earnings strength and improving market breadth.

Economic data released during January painted a mixed picture. Inflation showed further signs of moderation, though price pressures remained above the Federal Reserve’s long-term target. Labor market indicators suggested gradual cooling with payroll growth slowing and job openings trending lower, reinforcing expectations that monetary policy easing could begin in the first half of 2026. Fixed income markets reflected this outlook, as longer term Treasury yields remained range bound and credit spreads stayed relatively tight, signaling continued confidence in corporate balance sheets.

Equity leadership rotated during the month with value-oriented and cyclical sectors outperforming high-growth technology names, which faced profit-taking and valuation sensitivity following strong prior-year performance. Investor sentiment remained constructive but selective, favoring companies demonstrating earnings visibility, cost discipline and balance sheet strength.

Direct Selling Industry Developments

The direct selling industry entered 2026 exhibiting continued structural resilience despite broader economic uncertainty. Industry data and company disclosures reinforced the durability of core product categories, particularly wellness, nutrition and personal care, which continued to demonstrate stable consumer demand amid cautious discretionary spending.

Publicly traded direct selling companies experienced varied performance during January, reflecting company-specific fundamentals rather than broad sector weakness. Investor attention increasingly focused on operational execution, margin management and geographic diversification. Companies that communicated clear progress on cost controls, supply chain efficiency and digital engagement strategies generally experienced more favorable sentiment.

Technology-enabled transformation remained a defining theme across the sector. Companies continued to expand mobile commerce capabilities, enhance distributor-facing digital tools and integrate social commerce features, supporting productivity and engagement while reducing reliance on traditional in-person sales models. This evolution further underscored the industry’s gradual shift toward omnichannel strategies that blend direct selling with broader ecommerce and retail approaches.

Direct Selling Capital Advisors Index (DSCI)

The Direct Selling Capital Advisors Index (DSCI) posted a positive return in January, broadly mirroring the performance of the broader equity markets. The index benefited from relative stability among large-cap direct selling constituents and selective gains among companies demonstrating improving earnings visibility and operational momentum.

Compared with broader benchmarks, the DSCI exhibited lower volatility during periods of market stress, reinforcing the perception of direct selling equities as relatively defensive within the small- and mid-cap universe. Trading activity was measured, as investors continued to evaluate sector positioning following year-end rebalancing and ahead of upcoming earnings releases.

Since its inception, the DSCI has continued to deliver strong cumulative performance relative to traditional market indices, reflecting the long-term growth potential and resilience of publicly traded direct selling companies.

Looking Forward—Strategic Outlook

As 2026 begins, the direct selling sector faces a combination of macroeconomic uncertainty and company-specific opportunity. Key themes expected to influence near-term performance include:

- Macroeconomic sensitivity: Consumer confidence, labor market trends and interest rate policy will remain important drivers of demand, particularly for discretionary product categories.

- Digital and omnichannel execution: Companies that successfully integrate mobile ordering, social commerce, loyalty programs and data-driven distributor tools are likely to enhance productivity and retention.

- Earnings discipline and investor confidence: Continued focus on margin management, balance sheet improvement and execution against strategic initiatives will be critical in sustaining positive investor sentiment.

- Regulatory awareness: While no material regulatory changes emerged in January, evolving compliance standards across global markets remain an ongoing consideration.

Overall, January 2026 reinforced the view that while near-term volatility may persist, the direct selling sector remains structurally resilient, supported by adaptable business models, loyal customer bases and ongoing innovation.

Large Cap

Note: For the purposes of this report, Direct Selling Capital considers companies with a market capitalization in excess of $1 billion “Large Cap.”

Betterware de Mexico (NASDAQ: BWMX), founded in 1995, Betterware de Mexico is the leading direct-to-consumer company in Mexico focused on innovative products related to household organization, practicality, space-saving and hygiene. Through the acquisition of JAFRA on April 7, 2022, the company expanded into the beauty market in Mexico and the US, offering fragrances, color cosmetics, skincare and toiletries. The combined business operates an asset-light model with low capital expenditure, consistent profitability, double-digit revenue growth and strong free cash flow generation. Today, Betterware distributes its products in both Mexico and the United States.

In January 2026, Betterware’s share price increased approximately 26.4% month-over-month, marking a strong rebound from year-end trading and reflecting renewed investor confidence. Year-to-date, the stock is up 26.4%, positioning BWMX as one of the stronger performers within the direct selling sector early in the year. Since the inception of the Direct Selling Capital Advisors Direct Selling Index (DSCI) on February 1, 2020, BWMX has generated a total return of 90.7%, highlighting substantial long-term shareholder value creation.

Operational momentum entering 2026 remained solid. Recent results continued to reflect disciplined cost management, favorable product mix and ongoing synergies from the JAFRA integration. The company’s asset-light operating model and focus on margin preservation supported consistent EBITDA generation and healthy free cash flow, reinforcing its ability to fund growth initiatives while maintaining shareholder return programs.

While macroeconomic pressures and consumer demand variability in Mexico persist, Betterware’s diversified portfolio across home organization and beauty has helped stabilize revenue trends. Management’s continued emphasis on geographic expansion across Latin America—including preparation for entry into Colombia—along with investments in distributor productivity and digital tools, underscores the company’s focus on sustainable long-term growth.

Nu Skin Enterprises, Inc. (NYSE: NUS), together with its subsidiaries, engages in the development and distribution of various beauty and wellness products worldwide. It offers skincare devices, cosmetics and other personal care products, including ageLOC LumiSpa and ageLOC LumiSpa iO; and nutrition skincare products. The company also provides wellness products, such as LifePak nutritional supplements, ageLOC TR90 weight management system and Beauty Focus Collagen+.

In addition, it is involved in the research and product development of skincare products and nutritional supplements. The company sells its products under the Nu Skin, Pharmanex and ageLOC brands through retail stores, website, digital platforms and independent direct sellers and marketers, as well as a service center. Nu Skin Enterprises, Inc. was founded in 1984 and is headquartered in Provo, Utah.

In January 2026, Nu Skin’s stock increased 10.3% month-over-month, building on the recovery seen late last year. For the year-to-date, the stock is up 10.3%. Despite this positive start to 2026, the stock remains approximately 55% below its level at the inception of the Direct Selling Capital Advisors Direct Selling Index (DSCI) in February 2020, reflecting the long-term headwinds the company is working to overcome. The stock traded within a 52-week range of a high of $14.62 and a low of $5.32.

Momentum during January was largely fueled by renewed investor optimism following the company’s strategic presentation at the ICR Conference on January 12. Management utilized this platform to outline its 2026 roadmap, specifically highlighting the upcoming launch of the Prysm iO intelligent wellness device and the pre-market expansion steps into India. These initiatives bolstered confidence in the company’s ability to pivot toward high-growth opportunities despite broader sector challenges. Additionally, the market reacted favorably to the company’s valuation, which many analysts signaled had decoupled from intrinsic value given the company’s solid balance sheet and net cash positive position carried over from 2025.

Operational execution remained focused on preparing for the commercial rollout of new digital-first initiatives. Following the aggressive portfolio rationalization in late 2025, the company continued to refine its inventory and supply chain to support the targeted release of Prysm iO. Regionally, the company maintained aggressive promotional activities in key Asian markets, such as the “Triple Up” welcome privileges launched in Hong Kong, to stimulate distributor engagement. While Latin America continues to show promise, visibility into a consumer spending recovery in Mainland China and North America remains limited entering the first quarter.

Governance and shareholder alignment continue to be critical themes as the company approaches its next earnings cycle. With the Q4 and full-year 2025 financial results scheduled for release in mid-February, investor focus has shifted to whether the “net cash” financial health and reduced debt load ($209 million) can be sustained alongside the capital investments required for the India expansion. While macro-risks persist, Nu Skin’s double-digit gain in January suggests the market is cautiously pricing in a stabilization of the core business and potential upside from its 2026 innovation pipeline.

Herbalife Ltd. (NYSE: HLF) (formerly Herbalife Nutrition, Inc.) provides health and wellness products across North America, Latin America, EMEA, China and Asia Pacific. The company offers products in the areas of weight management; targeted nutrition; energy, sports and fitness; outer nutrition; and literature, promotional and other items.

It also provides weight management products, including meal replacement products, protein shakes, drink mixes, weight loss supplements, healthy snacks and metabolism boosting teas; targeted nutrition products, which comprise functional beverages and dietary and nutritional supplements that contain herbs, vitamins, minerals and other natural ingredients; outer nutrition products, such as facial skin, body and hair care products; and energy, sports and fitness products, including N-R-G tea and energy drink products.

In addition, it offers literature, promotional and other materials that comprise start-up kits, sales tools and educational materials. The company sells its products through sales representatives, independent service providers and company-operated retail stores and platforms. The company was formerly known as Herbalife Nutrition Ltd. and changed its name to Herbalife Ltd. in April 2023. Herbalife Ltd. was founded in 1980 and is headquartered in Los Angeles, California.

In January 2026, Herbalife’s stock rose by 33.7%, continuing its positive momentum from the previous year. Despite this significant recent rally, HLF remains down 46.7% since the establishment of the DSCI on February 1, 2020, reflecting the long-term recovery path the company is navigating. The stock traded within a 52-week range of a high of $17.93 and a low of $5.04.

Momentum during January was driven by an accelerated valuation re-rating as investors grew more confident in the durability of the “Herbalife 2.0” transformation. The market responded enthusiastically to continued signs of distributor stabilization and the company’s disciplined approach to capital allocation, which has kept net leverage ratios within the targeted range of approximately 2.8X. This sharp double-digit gain suggests that the heavy short interest in the stock may be unwinding in response to the improving fundamental backdrop established in late 2025.

Operational execution focused heavily on technology enablement. The company rolled out critical updates to its Pro2col app (v1.0.36), introducing enhanced device syncing for water and step tracking to deepen user engagement and distributor utility. These digital enhancements are central to the company’s strategy to modernize its direct selling model. Regionally, the company amplified its brand visibility in growth markets like India through new media initiatives, such as the “Live Your Best Life” podcast series, aimed at broadening the funnel for new distributor recruitment.

Governance and forward-looking sentiment remain cautiously optimistic. While the rapid stock price appreciation has improved the technical picture, institutional investors are now looking toward the upcoming Q4 and full-year earnings report to validate whether the “beta” success of digital tools like Pro2col is translating into material revenue acceleration. Management continues to balance this aggressive digital investment with the need for strict cost controls to maintain the adjusted EBITDA margins that catalyzed the late-2025 recovery.

Medifast, Inc. (NYSE: MED), through its subsidiaries, operates as a health and wellness company offering habit-based, coach-guided lifestyle solutions focused on weight management and obesity support in the United States. The company’s flagship brand, OPTAVIA, delivers clinically-supported weight loss programs, GLP-1 support plans and a wide variety of food products—such as bars, shakes, soups, cereals and snacks—complemented by one-on-one coaching, digital tools and community support. Medifast was founded in 1980 and is headquartered in Baltimore, Maryland. Its products are sold via point-of-sale transactions and ecommerce.

For the month of January 2026, shares of Medifast increased by 7.1% compared to December. Year-to-date, the stock is up 7.1%. Since the establishment of the DSCI on February 1, 2020, the stock has declined by 85.6%. The stock traded within a 52-week range of a high of $16.66 and a low of $10.10.

Momentum in January was primarily driven by a positive market reaction to the company’s aggressive brand visibility and leadership adjustments. On January 5, Medifast announced a planned leadership transition aimed at accelerating its transformation into a “metabolic health” company.

This governance shift was accompanied by a renewed marketing push, including a feature in People Magazine highlighting a client’s metabolic health journey and the premiere of the second episode of the docuseries Health by Design on January 15. These events helped catalyze a relief rally, lifting shares off their 52-week lows as investors speculated on a potential operational floor.

Operational execution remains centered on the company’s pivot toward the GLP-1 companion market. Management continues to emphasize its “Metabolic Synchronization” strategy—designed to help users preserve lean muscle mass while using weight-loss medications—as a critical differentiator against generic food competitors. However, the operational backdrop remains challenging. Guidance for the upcoming fourth-quarter results implies continued pressure on top-line revenue ($65M–$80M range) and a year-over-year decline in active earning coaches. The company is betting that its new “LifeMD” collaboration and updated coach training will stabilize these metrics in early 2026.

Market sentiment is cautiously awaiting the Q4 and full-year 2025 financial results, scheduled for release on February 17, 2026. While the 7.1% gain in January reflects some optimism, analyst ratings remain mixed, with concerns lingering over the timeline for returning to profitability. Investors are closely monitoring whether the company’s robust cash position can effectively bridge the gap until the new metabolic health initiatives gain traction. Until coach productivity shows definitive signs of reversing its downward trend, the stock is likely to remain volatile and sensitive to news regarding the broader GLP-1 pharmaceutical landscape.

USANA Health Sciences, Inc. (NYSE: USNA) develops, manufactures and sells science-based nutritional, personal care and skincare products across Asia Pacific, the Americas and Europe. The company operates through two segments: Direct Selling and Hiya Direct-To-Consumer. Its product lineup includes USANA Nutritional Optimizers for cardiovascular, skeletal and digestive health; Essentials/CellSentials—vitamin and mineral supplements for all ages beginning at 13 months; and food products such as meal replacement shakes and snack bars for healthy weight management, digestive health and hydration.

USANA also offers the Celavive skincare line tailored for various skin types and ethnicities, as well as online tools and business materials for associates. Products are sold through retail, subscription-based models and direct selling. The company holds research collaboration agreements with the Beijing University of Chinese Medicine and the National Sports Training Bureau. USANA was founded in 1992 and is headquartered in Salt Lake City, Utah.

For the month of January 2026, USANA’s stock rose by 10.5% compared to December. Year-to-date, the stock is up 10.5%, reflecting a sharp rebound from the previous year’s lows, though it still underscores underperformance relative to broader markets and peers over the longer term. Since the establishment of the DSCI on February 1, 2020, USANA shares have lost 67.2%. The stock traded within a 52-week range of a high of $38.32 and a low of $18.48.

Momentum in January was significantly influenced by a major leadership transition and a strategic update delivered ahead of the ICR Conference. On January 8, the company announced the return of Kevin Guest as Chief Executive Officer, a move that investors viewed as a stabilizing force given his deep experience with the company’s sales force and culture. This sentiment was further bolstered on January 12, when USANA released preliminary fiscal year 2025 net sales of approximately $925 million—slightly ahead of prior guidance—and provided an initial 2026 sales outlook of up to $1 billion. These announcements helped catalyze the stock’s double-digit gain, signaling renewed market confidence in the company’s ability to navigate its turnaround.

Operationally, the company’s diversification strategy is becoming a central growth engine. Management highlighted that while the core direct selling business faces continued pressure, its subsidiaries are accelerating. The Hiya direct-to-consumer segment is projected to generate between $140 million and $155 million in 2026, while Rise Wellness (comprising Rise Bar and Protein Pop) is expected to jump to $65–$80 million. To support this growth, USANA is heavily investing in inventory and capital expenditures, accepting near-term breakeven margins in the Rise Wellness segment to capture market share. This shift from a pure-play MLM model to a diversified health and wellness platform is beginning to reshape the company’s revenue mix.

Despite the positive price action, investor sentiment remains watchful. While the leadership change and preliminary numbers were well-received, analysts continue to debate the long-term profitability of the pivot to low-margin consumer goods compared to the traditional high-margin direct selling model. With the full fourth-quarter and fiscal year 2025 results scheduled for February 17, the market is waiting to see if the “leadership renewal” strategy and subsidiary growth can translate into consistent bottom-line improvements.

eXp World Holdings, Inc. (NASDAQ: EXPI), together with its subsidiaries, provides cloud-based real estate brokerage services for residential homeowners and homebuyers. The company operates through three segments: North American Realty, International Realty, and Other Affiliated Services. It acts as a licensed broker for processing residential and commercial real estate transactions and provides other real estate support services.

In addition, the company offers FrameVR.io, a web-accessible proprietary technology providing immersive 3D platforms; SUCCESS magazine and its related media properties, which offer training, classes, resources and tools under the SUCCESS brand; and SUCCESS Space, a coworking solution that provides rental workspaces, professional development coaching, media production services, virtual-world communications technology and full-service cafes.

The company operates primarily in North America, Canada, the United Kingdom, Australia, South Africa, India, Mexico, Portugal, France, Brazil, Italy, Hong Kong, Colombia, Spain, Israel, Panama, Germany, the Dominican Republic, Greece, New Zealand, Chile, Poland, Dubai and has expanded into Japan, Romania and the Netherlands, with additional international markets across Europe and Asia. eXp World Holdings, Inc. was formerly known as eXp Realty International Corporation and changed its name in May 2016. The company was incorporated in 2008 and is headquartered in Bellingham, Washington.

In January 2026, eXp World Holdings’ stock declined 0.1% compared to December 2025. This slight consolidation follows the previous month’s volatility, reflecting a cautious holding pattern among investors ahead of full-year earnings. While the stock faced resistance due to broader sector rotation and continued scrutiny on agent governance, it stabilized relative to the sharper selloffs seen in late 2025. Despite this flat monthly performance, long-term appreciation remains robust, with shares up an aggregate 89.1% over the six years since the launch of the DSCI in February 2020.

Operationally, the company began the year by restructuring its executive compensation to align leadership incentives more closely with shareholder interests, effective January 1. Growth initiatives continued with the onboarding of high-profile agent teams, such as the Nick Shivers Team, reinforcing the appeal of the agent-centric model. Management maintained a strict focus on cost efficiency and capital allocation while preparing for the rollout of enhanced agent productivity tools. The International Realty segment continues to be a focal point, leveraging recent market entries in Europe to drive cross-border transaction volume.

Market sentiment in January was mixed, weighed down by a Delaware Court of Chancery ruling regarding board oversight duties, which added a layer of governance risk to the investment narrative. However, technical indicators such as the RSI moving out of oversold territory suggested potential stabilization. Analyst commentary remains focused on the company’s ability to navigate legal headwinds while maintaining the scalability of its cloud-based platform, with significant attention turning toward the upcoming Q4 and full-year financial results expected in late February.

Primerica, Inc. (NYSE: PRI), together with its subsidiaries, provides financial products and services to middle-income households in the United States and Canada. The company operates in three segments: Term Life Insurance; Investment and Savings Products; Senior Health; and Corporate and Other Distributed Products. The Term Life Insurance segment underwrites individual term life insurance products. The Investment and Savings Products segment provides mutual funds and various retirement plans, managed investments, variable and fixed annuities and fixed indexed annuities; and offers segregated funds.

The Corporate and Other Distributed Products segment provides mortgage loans; prepaid legal services that assist subscribers with legal matters, such as drafting wills, living wills and powers of attorney, trial defense, and motor vehicle-related matters; ID theft defense services; auto and homeowners’ insurance; home automation solutions; and insurance products, including supplemental and accidental death, and disability insurance. It distributes and sells its products through licensed sales representatives. Primerica, Inc. was founded in 1927 and is headquartered in Duluth, Georgia.

In January 2026, Primerica’s stock price increased by 1.8% compared to December 2025. This positive start to the year contrasts with the broader volatility seen in the financial sector, bringing the year-to-date performance to a gain of 1.8%. The stock’s resilience reflects continued investor confidence in the company’s defensive business model and its ability to generate consistent cash flow despite a complex macroeconomic backdrop. Long-term performance remains exceptional; since the launch of the Direct Selling Capital Advisors Direct Selling Index (DSCI) on February 1, 2020, Primerica shares have appreciated 140.1%, solidifying its position as a standout performer among index constituents.

Operationally, Primerica kicked off the year with significant momentum, highlighted by its largest-ever Senior Leadership Meeting held in early January, where management outlined strategic initiatives for sales force expansion and digital tool adoption. The company also began executing on its $475 million share repurchase program for 2026, providing structural support to the stock price. Additionally, the release of its latest Middle-Income Household Budget Index in late January offered critical insights into the “new reality” of cost-of-living pressures facing its core demographic, reinforcing the relevance of its financial education and protection products.

Market sentiment remained cautiously optimistic throughout the month, with investors positioning themselves ahead of the Fourth Quarter 2025 financial results scheduled for mid-February. Analyst commentary continues to favor Primerica’s disciplined expense management and capital return strategy, viewing the company as a stable anchor in the direct selling space. While some concerns persist regarding the impact of sustained high interest rates on investment product sales, the consensus view suggests that the company’s strong balance sheet and recurring insurance revenues provide a substantial buffer against near-term headwinds.

Within the broader industry context, recent reports from Direct Selling News emphasize the growing importance of trust and tangible value in the gig economy. Primerica’s recent national survey data, which highlights the financial resilience of middle-income families, aligns well with this industry-wide shift toward consumer advocacy. As the sector moves away from speculative growth models, Primerica’s focus on fundamental financial needs—protection, savings and debt management—continues to distinguish it as a leader in sustainable direct selling.

Oliveda International, Inc. (OTC: OLVI) was founded in 2003 and has more than 20 years of experience in: 1) the management and organic certification of mountain olive trees; 2) the extraction of international award-winning extra virgin olive oils; 3) the extraction of hydroxytyrosol, a compound with antioxidant, anti-inflammatory, anticancer and skin- and eye-protective effects; and 4) the production and distribution of cosmetic and holistic waterless products derived from the olive tree.

Oliveda International, Inc. and its subsidiaries, including Olive Tree People Inc., Olive Tree People Europe AG, Oliveda Deutschland GmbH, and Olive Tree Farmers SL, were founded by German real estate investor Thomas Lommel. The group has established a unique market position through innovations such as Olive Tree Therapy “10 years in 14 days,” olive matcha (made from ground olive leaves), and a coffee alternative based on olive leaves and hydroxytyrosol. Lommel is also active in the mindfulness sector with his olive tree sound bath meditations and the broadcast of olive tree frequencies globally.

In January 2026, Oliveda’s stock declined 8.6% compared to December 2025. For the first month of 2026, the stock has declined by 8.6%. This continued downward trajectory extends the volatility seen throughout the previous year, with the share price struggling to find a stable floor despite aggressive corporate communications regarding growth and valuation. The decline reflects persistent skepticism in the broader market regarding the disconnect between the company’s self-reported valuation milestones and its actual market capitalization.

Operationally, the company began the year with a major strategic pivot, announcing the full withdrawal of its products from European retail shelves to focus exclusively on a Direct-to-Consumer (DTC) model. Management positioned this shift—affecting markets in Germany, Austria, Switzerland and Spain—as a move to mirror its US strategy and empower its “Waterless Beauty Consultant” network. While the company touted this as a necessary step to scale its “Olive Tree People” ecosystem and convert flagship locations in Berlin and Düsseldorf into experiential hubs, the abrupt transition adds near-term execution risk to its revenue model.

As an OTC-listed issuer, Oliveda operates with significantly reduced disclosure requirements compared to exchange-listed peers. The absence of consistent, detailed financial reporting limits visibility into revenue sustainability, profitability and cash flow generation, materially constraining institutional participation and investor confidence. These factors have positioned the stock as highly speculative within the direct selling universe.

While the company continues to emphasize product innovation and distributor engagement within the broader wellness and sustainable personal care categories, market participants remain cautious. Without demonstrable improvements in financial transparency, operational consistency, and distributor network stability, the company is likely to remain subject to elevated share price volatility and restricted access to capital markets.

Looking ahead, Oliveda’s long-term prospects hinge on its ability to improve disclosure practices, establish predictable operating performance and demonstrate sustained consumer demand for its differentiated offerings. Until such visibility improves, the stock is expected to remain suitable only for investors with a high tolerance for risk.

The Beachbody Company, Inc. (NYSE: BODI) operates as a fitness and nutrition company in the United States and internationally. The company offers Beachbody on Demand, a subscription streaming service providing fitness programs such as P90X, Insanity and 21 Day Fix; nutrition programs including Portion Fix and 2B Mindset; and nutritional products like Shakeology shakes and Beachbody Performance supplements. The company also faces legal challenges in California, where efforts are underway to reclassify independent consultants as employees, which may impact its direct selling model.

In January 2026, Beachbody’s stock price increased by 9.8% compared to December 2025. This solid start to the year brings the year-to-date gain to 9.8%, building on the momentum established in late 2025. The positive performance was primarily driven by significant improvements in the company’s capital structure and renewed investor interest following management’s participation in key investor conferences. The “January Effect,” combined with the traditional seasonal surge in fitness-related spending, further supported the stock’s upward trajectory.

Operationally, the month was defined by a critical financial milestone: on January 8, the company announced a favorable amendment to its credit agreement with Tiger Finance. This restructuring significantly enhanced financial flexibility by modifying liquidity covenants, effectively de-risking the balance sheet and validating the company’s turnaround strategy.

On the product front, excitement built around the announcement of “P90X Generation Next,” a modernized iteration of its flagship program set to launch in early February. This launch represents a strategic pivot toward leveraging legacy brand equity to drive new digital subscriber growth. Additionally, the company launched the “10 Minute BODi Accountability Group” challenge, aiming to boost user retention through micro-habits and community engagement.

Market sentiment remained constructively bullish throughout January. The credit agreement amendment was well-received by analysts, who viewed it as a removal of a significant overhang on the stock. Management’s presentation at the ICR Conference in Orlando earlier in the month further solidified confidence in the company’s profitability-first approach. While caution remains regarding the long-term resolution of independent contractor classification in California, the immediate focus has shifted toward the company’s improved liquidity position and its ability to execute on its 2026 product roadmap.

From an industry perspective, Direct Selling News and broader market analysis highlight a shift in the digital fitness sector toward “hybrid accountability” models—combining digital convenience with the community support typical of direct selling. Beachbody’s January initiatives align closely with this trend. As the company moves into February, investor attention is expected to center on the initial uptake of the new P90X program and upcoming Q4 earnings, which will provide the first concrete data points on the sustainability of this recent growth.

The Real Brokerage Inc. (NASDAQ: REAX) is a technology-driven, asset-light real estate brokerage that empowers agents through a cloud-based platform, AI-enabled tools and integrated fintech solutions. Founded in 2014, the company operates across the United States and Canada, utilizing an independent contractor model and performance-based compensation structure that aligns with direct selling–adjacent distribution frameworks.

Entering January 2026, the stock faced a period of consolidation and mixed sentiment following the broader rotation out of technology and financial sectors. While analysts maintained a “Strong Buy” consensus with an average price target of approximately $6.33, the stock experienced downward pressure, ending the month near $3.54. Despite this volatility, institutional ownership remained stable at approximately 53%, and the company received a notable rating upgrade to “Strong Buy” from Freedom Capital Markets late in the month, signaling continued professional confidence in the platform’s long-term value proposition.

During the month, the company demonstrated exceptional recruitment momentum, officially surpassing the 32,000-agent milestone. This growth was bolstered by the strategic onboarding of high-production teams, including the expansion of its Michigan footprint through the 172-agent “Good Company” brokerage and the addition of the Houston Properties Team. These moves underscore the continued success of Real’s “Private Label” and “Pro Teams” programs, which allow established independent brokerages and teams to leverage Real’s technology while maintaining their local brand identity.

Technology and agent sentiment remained central to the company’s January narrative. Real released its monthly agent survey, which showed agent optimism hitting an 11-month high as the industry anticipates a 2026 housing market recovery. Management also announced plans to host the Fourth Quarter and Full Year 2025 earnings call in early March, while continuing to highlight the operational efficiencies provided by the reZEN platform and the Leo CoPilot AI.

Although the month was marked by some external legal and sector-wide headwinds, The Real Brokerage enters February focused on its quality-at-scale strategy, supported by a debt-free balance sheet and a rapidly expanding North American network.

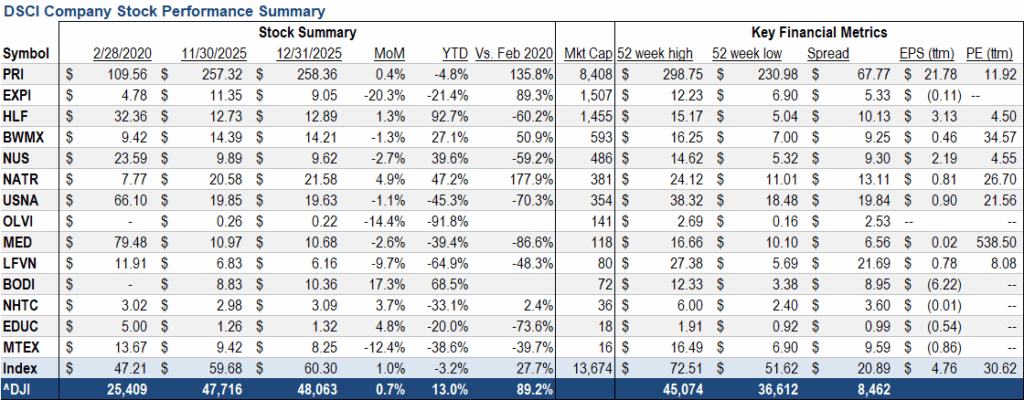

Below are two summary diagrams on the direct selling large cap companies.

Small Cap

Nature’s Sunshine Products, Inc. (NASDAQ: NATR), a natural health and wellness company, manufactures and sells nutritional and personal care products in Asia, Europe, North America, Latin America,] and internationally. The company provides general health products related to blood sugar support, bone health, cellular health, cognitive function, joint health, mood, sexual health, sleep, sports and energy and vision; immune products; cardiovascular products; and digestive products. It also offers personal care products, including oils and lotions, aloe vera gel, herbal shampoo, herbal skin treatment, toothpaste and skin cleanser products, as well as weight management products.

The company provides its products under the Nature’s Sunshine Products and Synergy WorldWide brands directly to customers and to a sales force of independent consultants. Nature’s Sunshine Products, Inc. was founded in 1972 and is headquartered in Lehi, Utah.

In January 2026, NATR’s share price increased by approximately 16.9% compared to December 2025, marking a strong start to the new year and significantly accelerating the momentum established in late 2025. For the first month of 2026, the stock delivered a total return of 16.9%, outperforming small-cap peers across the health, wellness and direct selling sectors. Since the inception of the DSCI index, Nature’s Sunshine shares have gained 224.8%, representing the largest cumulative return among all small-cap stocks and all companies included in the DSCI. The company does not currently pay a dividend, continuing to prioritize reinvestment in growth initiatives, digital capabilities and long-term operational efficiency.

Operationally, Nature’s Sunshine entered 2026 with continued strength following a robust finish to the prior year. Recent quarterly results reflected sustained double-digit year-over-year revenue growth, driven by resilient international demand and expanding adoption of digital and subscription-based sales tools. Margin performance remained a key highlight, supported by disciplined pricing strategies, favorable product mix, and ongoing supply chain optimization. Adjusted EBITDA growth continued to outpace revenue, underscoring the scalability of the business model. Management commentary has emphasized execution consistency, consultant productivity, and ongoing investments in technology and customer engagement as core drivers for 2026 performance.

Market sentiment toward NATR strengthened further in January. According to Yahoo Finance data, analyst coverage continues to reflect a moderate buy consensus, with increasing attention on the company’s ability to generate durable cash flow, expand margins and compound growth over multiple years rather than short-term volatility. Valuation discussions suggest the stock remains reasonably priced relative to its growth trajectory and balance sheet profile, particularly within the small-cap wellness universe. Institutional ownership trends and limited short interest continue to signal confidence in the company’s long-term strategy.

From an industry perspective, Direct Selling News highlights several structural trends supporting Nature’s Sunshine’s positioning. These include accelerating digital adoption across direct selling models, rising global consumer demand for preventive health and wellness solutions and heightened emphasis on transparency, product quality and regulatory compliance. Companies that successfully blend technology-enabled commerce with relationship-driven selling are gaining competitive advantage, and Nature’s Sunshine’s ongoing digital transformation aligns well with these sector dynamics.

Looking ahead, Nature’s Sunshine enters 2026 with strong momentum, a diversified global footprint, and a clear strategic focus. Growth opportunities include further international expansion, increased penetration of autoship and loyalty programs and continued margin enhancement through operational discipline. Risks remain related to macroeconomic conditions, foreign exchange fluctuations, regulatory developments and competitive intensity within the wellness category. Overall, the company begins the new year with exceptional stock performance, improving financial fundamentals and a favorable position within the global direct selling landscape.

LifeVantage Corporation (NASDAQ: LFVN) engages in the identification, research, development, formulation and sale of advanced nutrigenomic activators, dietary supplements, nootropics, pre- and probiotics, weight management and skin and hair care products. It offers Protandim, a dietary supplement; LifeVantage Omega+, a dietary supplement that combines DHA and EPA Omega-3 fatty acids, Omega-7 fatty acids, and vitamin D3; LifeVantage ProBio, a dietary supplement to support gut health; LifeVantage IC Bright, a supplement to support eye and brain health, reduce eye fatigue and strain, supports cognitive functions, and support normal sleep patterns; LifeVantage Daily Wellness, a dietary supplement designed to strengthen immune health; LifeVantage Rise AM & Reset PM System that provides the body with the right nutrients; LifeVantage D3+, a dietary supplement that provides vitamin D3, vitamin K2, magnesium, calcium, and other trace minerals to support a balanced immune system, strong bones and cardiovascular health; PhysIQ Fat Burn to support weight management; PhysIQ Prebiotic is a dietary supplement designed to support the good bacteria in the gut and a healthy microbiome; Petandim for Dogs, a supplement to combat oxidative stress in dogs; and Axio, a nootropic energy drink mix.

The company also provides anti-aging skincare products, including liquid collagen, facial cleansers, eye cream, moisturizing cream, sunscreen, perfecting lotions, hand creams, as well as hair care products, such as invigorating shampoos, nourishing conditioners, and scalp serums under the TrueScience brand name. It sells its products through its website and network of independent consultants in the United States, Mexico, Japan, Australia, Hong Kong, Canada, Thailand, the United Kingdom, the Netherlands, Germany, Taiwan, Austria, Spain, Ireland, Belgium, New Zealand, Singapore and the Philippines. The company also launched Evolve Compensation Plan and other LV360 initiatives into the Philippines, Taiwan, Hong Kong and Singapore. The company is based in Lehi, Utah.