Crazy, tumultuous, unpredictable, challenging and in some cases accelerating—all these describe 2020. For the global direct selling industry, it was a year of phases unfolding differently in regions and countries around the world, depending upon a number of factors associated with the severity of COVID, governmental response to it, market readiness and the infrastructure capability of the global supply chain.

And when the World Federation of Direct Selling Associations compiled 2020 statistics from DSAs the world over—an arduous task undertaken by a dedicated team of volunteers representing some of the finest direct selling companies—they found global factors like lockdowns, job displacement and supply chain disruptions ebbed and flowed from market to market and even within markets, producing highs and lows set out in black and white data.

But the real “big picture” insight for 2020 is how well the industry performed despite those challenges. The $179.3 billion generated in estimated retail sales globally during 2020 underscores the entrepreneurial and adaptable nature of the industry, as well as the core power of one-to-one relationships deepened through the increasing use of technology during a time of separation and uncertainty.

Also emerging from WFDSA’s data is increasing numbers of preferred customer programs, with 40 percent of markets now reporting some category of participation that allows people to sign up with companies to access products. Some 30 million of these preferred customers appear in the 2020 data, in addition to seller counts. Migration of discount customers to preferred customer programs is also increasing.

Market readiness and the ability of companies to leverage technology varied greatly in 2020, and WFDSA theorizes these factors had a substantial impact on sales results.

“I think there are going to be a lot of case studies coming out of 2020. It’s interesting to look at some of the markets that really performed well and to contrast some of the markets that didn’t. What are the lessons from that? There’s a lot to be gained,” says Tim Sanson, co-chair, WFDSA Global Research Sub-Committee.

“In a lot of markets, the industry responded extremely well, and some of the reasons we theorize are the increased use of technology, social media, and video conferencing for independent sellers to continue to stay connected with their customers and to continue to build their businesses,” Sanson says.

The extra time people had to work, while stuck at home or displaced from regular jobs, also provided opportunities for sellers to connect with customers, who may have been craving social interaction.

Companies shifted away from traditional in-person meetings, went virtual and found meaningful ways to stay connected digitally. Sanson says the ability to leverage that technology was one of the keys. But market readiness for that was not consistent.

For those companies and markets that performed well, the looming task is to cement gains in 2021 while the entire industry learns from the lessons 2020 dished out.

The Data

*All WFDSA data have been rounded throughout.

WFDSA reports global estimated retail sales of $179.3 billion (Constant U.S. Dollars) for 2020.

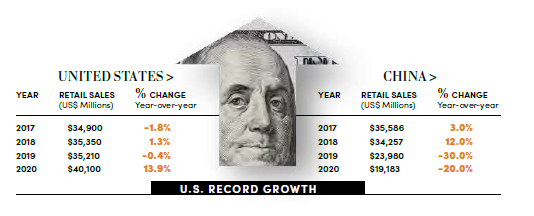

History shows that China’s market volatility infuses ups and downs into global market data. So, for the second year, data is reported for dual analyses—one includes China, and another excludes China due to its size, struggles and impact that market’s performance has on the industry as a whole.

Excluding China1 (Q1 2019, Chinese Government 100-day review of nutritional supplement industry not related specifically to direct selling), 2020 worldwide retail sales showed a year-over-year increase of 5.8 percent, up from 1.4 percent in 2019. Global sales results, including China, rallied from a 4.3 percent decrease in 2019 to show a 2.3 percent increase in 2020.

Regional market performance, due to the extenuating circumstances of COVID, was a mixed bag of ups and downs for 2020. The Americas’ estimated retail sales expanded 10.6 percent, Europe was up 1.6 percent, and emerging markets in the Africa/Middle East region gained 4.0 percent. China’s estimated retail sales lost significant ground and hit Asia/Pacific hard, as that region’s performance fell 3.6 percent.

Global industry growth, measured by the 3-year Compound Annual Growth Rate (CAGR), indicates a healthy expansion pace of 3.0 percent (excluding China) and -0.1 percent (including China) for the 2017-2020 period.

2020 was a tumultuous year, and it is reflected in the composition of DSN’s Billion Dollar Markets list. Significant rank shifting occurred, as the United Kingdom fell from 11 to 23 (in part due to incomplete data), and Ecuador dropped from the list entirely. Sales swings were wide in some country markets, with China dropping 20 percent on the heels of a 30 percent decrease in 2019 and Peru struggling with a 16.5 percent fall.

But 47 out of 70 markets reported estimated retail sales growth, and the upsides swung the pendulum wide in the other direction too, with the United Kingdom posting 45 percent growth and a near-record 13.9 percent increase in the United States. Both India (up 28.3 percent) and Canada (up 26 percent) advanced several rankings after stretching product sales in 2020. Argentina’s performance (up 90.3 percent), despite the impact of extreme, non-COVID related inflation, is notable.

Of the 23 Billion Dollar Markets, the top ten performers make up 78 percent of global estimated retail direct sales for 2020. The United States leads with 22.4 percent of global sales, followed by China with 10.7 percent; Germany, 10 percent; Korea, 9.9 percent; Japan, 8.8 percent; Brazil, 4.6 percent; Malaysia, 3.9 percent; Mexico, 2.9 percent; France, 2.9 percent; and Taiwan, China at 2.5 percent.

125.4 million independent representatives participated in direct selling in 2020, an increase of nearly six million over 2019’s 119.9 million. This includes more than 65 million independent representatives who work either full- or part-time to earn supplemental income. Excluding China, all regions increased sales force numbers with the largest increase of 18.2 percent in the emerging markets within Africa and the Middle East.

2020 BREAKDOWN BY REGION

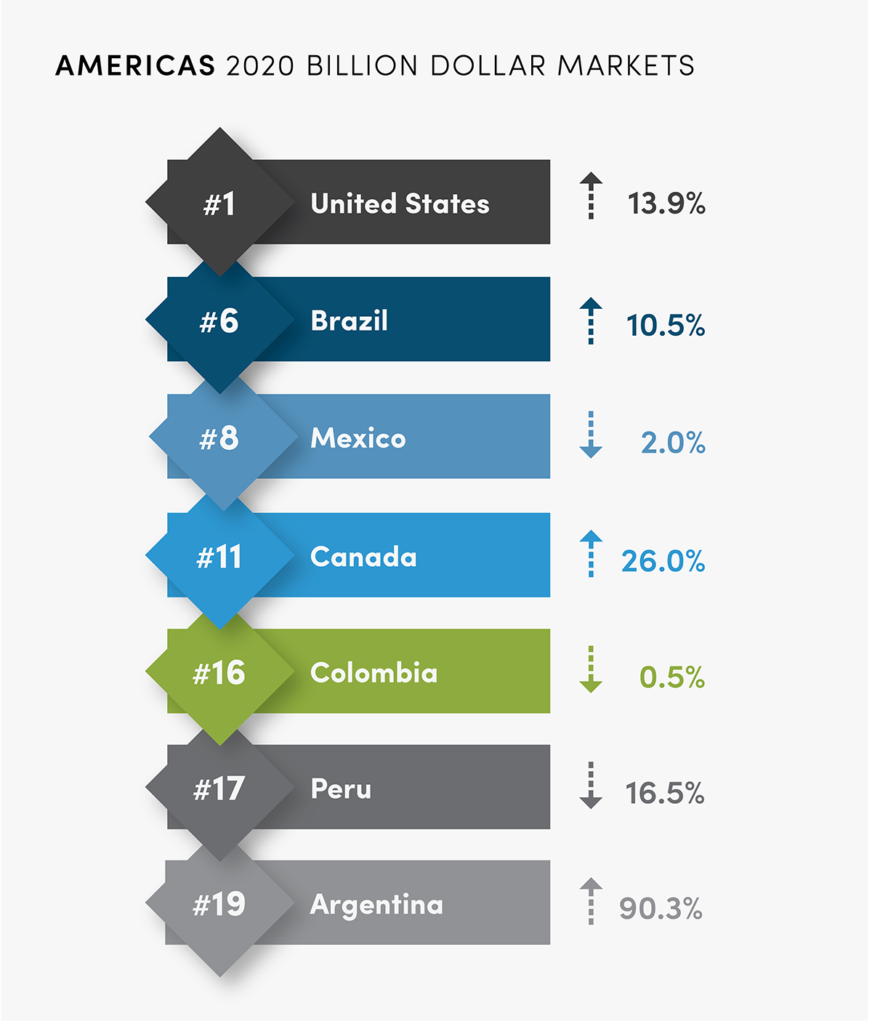

The Americas

The Americas—North and South/Central—comprised 36 percent of direct selling’s global estimated retail sales in 2020. Combined, they reported $64.7 billion for 2020, posting growth of 10.6 percent with CAGR increasing to 3.9 percent.

Seven Billion Dollar Markets exist in this region for 2020. Ecuador, previously ranked on the 2019 list, did not qualify in 2020. Wellness and Cosmetics and Personal Care products were even-matched in sales popularity in recent years; however, 2020 saw a surge in Wellness products, and it took a 31 percent share, compared to Cosmetics 29 percent. A distant third is Household Goods and Durables at 13 percent, up from 11 percent in 2019. The Americas recorded nearly three million more independent representatives (33.7 million), up 9 percent over 2019 and offering a revitalization of sorts after declines dating back to 2017 and 2018.

Regional data for the Americas are reported together; however, the Americas are split here to better understand each of the distinct markets.

North America

Direct selling in North America for 2020 reported $43.2 billion in sales, up 14.7 percent thanks to a near-record increase in both the United States and superb performance in Canada.

After a year of flat-line sales in 2019, the United States held 22.4 percent of the global market in 2020. The U.S. pushed through the challenges of COVID to sales increases seldom seen before in the market and gained 2.4 percent global market share over 2019. They generated $40.1 billion in estimated retail sales, an increase of 13.9 percent, which helped the overall U.S. CAGR reach 4.7 percent in 2020. Following a 6 percent retail sales fall for 2019, Canada’s direct selling market surged ahead with 26 percent sales growth, reaping $3.1 billion in estimated retail sales with a 5 percent CAGR.

WFDSA data shows 18.1 million independent representatives in North America, up from 17.5 million in 2019; 16.7 million of them live and work in the United States, with 1.4 million in Canada. Both markets saw increases this year.

South/Central America

The South/Central America region is made up of five Billion Dollar Markets: Brazil, Mexico, Colombia, Peru, and Argentina. Performance in this region was a mixed bag. Despite Argentina’s inflationary market, their 90.3 percent increase is notable. Brazil marked a sales increase of 10.5 percent. But other countries experienced significant losses: Peru declined 16.1 percent. Ecuador, a recent Billion Dollar Market, fell off the 2020 list after a 23.1 percent decline in sales. All told, this region reported estimated retail sales of $21.5 billion, an increase of 3.3 percent for 2020 and a CAGR of 2.3 percent.

Market performance breakdown was as follows: Brazil ($8.3 billion, 4.6 percent of global market, 4.0 percent CAGR), Mexico ($5.3 billion, 2.9 percent of global market, 0.6 percent CAGR), Colombia ($2 billion, 1.4 percent CAGR), Peru ($2 billion, -3.8 percent CAGR), and Argentina ($1.5 billion, 41.2 percent CAGR). Inflationary economies like Argentina typically report restated data later in the year.

Cosmetics and Personal Care products reined in 57 percent of product sales; however, 2020 showed a third year of decline from a high of 67 percent in 2017. The Wellness category is growing and captured 19 percent of sales in 2020. South and Central America saw a surge in independent representatives, as 2020 recorded nearly 15.7 million—almost two million additional representatives over 2019 (13.4 million).

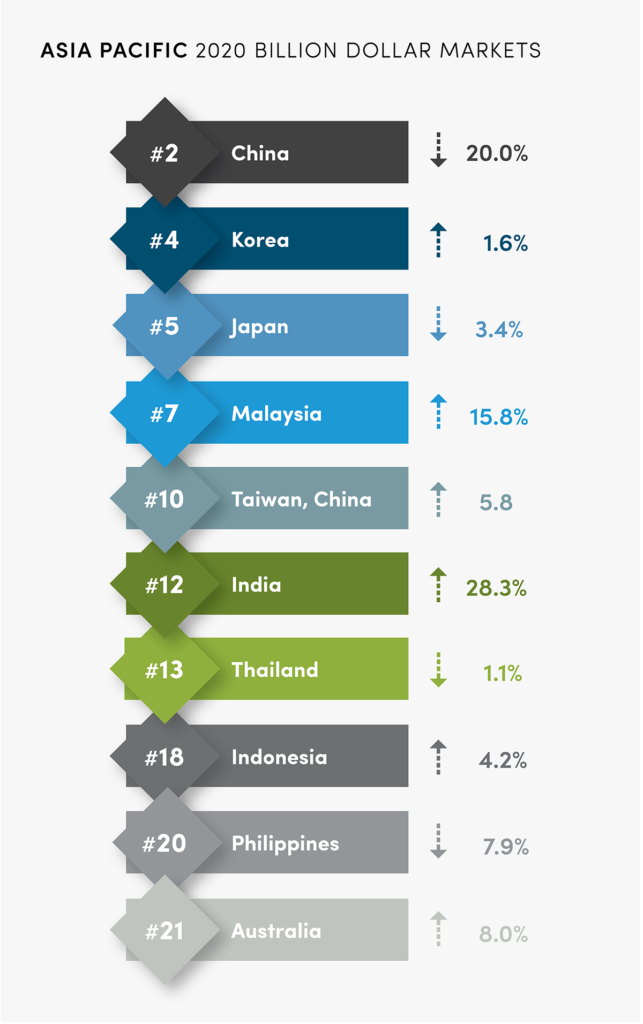

Asia Pacific

There are ten Billion Dollar Markets in the Asia-Pacific region, which generated 43 percent of global retail sales. Asia-Pacific estimated retail sales were down for the second year, reporting $76.5 billion in 2020, a decrease of 3.6 percent. The 3-year CAGR stood at -3.7 percent. Nearly 70 million independent direct sellers represented products and services throughout the whole of the region, nearly two million more than in 2019. That was 55 percent of the global independent direct sellers total. Wellness products comprised 47 percent of all sales, with Cosmetics and Personal Care at 22 percent.

China, the largest and most influential Asia/Pacific market, generated $19.2 billion in 2020 estimated retail sales, a reduction of 20 percent. As a result, their global market share fell to 10.7 percent in 2020, compared to 13 percent in 2019. China’s 3-year CAGR fell sharply again in 2020 to -17 percent. Totals for independent representatives fell for the third year to 3.6 million in 2020, a loss of nearly two million representatives since W2018.

The ordinary complexities of the China market paired with the impact of COVID brought significant challenges to data collection; however, WFDSA partnered with the Direct Selling Research Center at Peking University for the second year to improve understanding, consistency, and confidence in the data they collect.

The 2020 Billion Dollar Markets list includes nine other Asia/Pacific countries, whose performance reflected the impact and timing of COVID and each country’s ability to surmount the challenges it presented. India once again marked significant growth, generating a half-billion more dollars in estimated retail sales over 2019 with a total of $3 billion and a CAGR of 17.6 percent. Malaysia continued its forward momentum with a surprise surge, posting nearly $1 billion more in sales during 2020 over 2019 with estimated retail sales of $7 billion. CAGR remains steady at 11.4 percent. But Asia/Pacific markets like Australia, Japan, the Philippines, and Thailand struggled.

The performance of the remaining Asia-Pacific Billion Dollar Markets was as follows: Australia ($1.3 billion, -0.1 percent CAGR), Indonesia ($1.6 billion, 7.6 percent CAGR), Japan ($16 billion, 8.6 percent of the global market, -1.5 percent CAGR), Korea ($17.7 billion, 9.9 percent of global market, 2.6 percent CAGR), Philippines ($1.4 billion, 1.9 percent CAGR), Taiwan-China ($4.5 billion, 2.5 percent of global market, 5.8 percent CAGR) and Thailand ($3.0 billion, -0.9 percent CAGR).

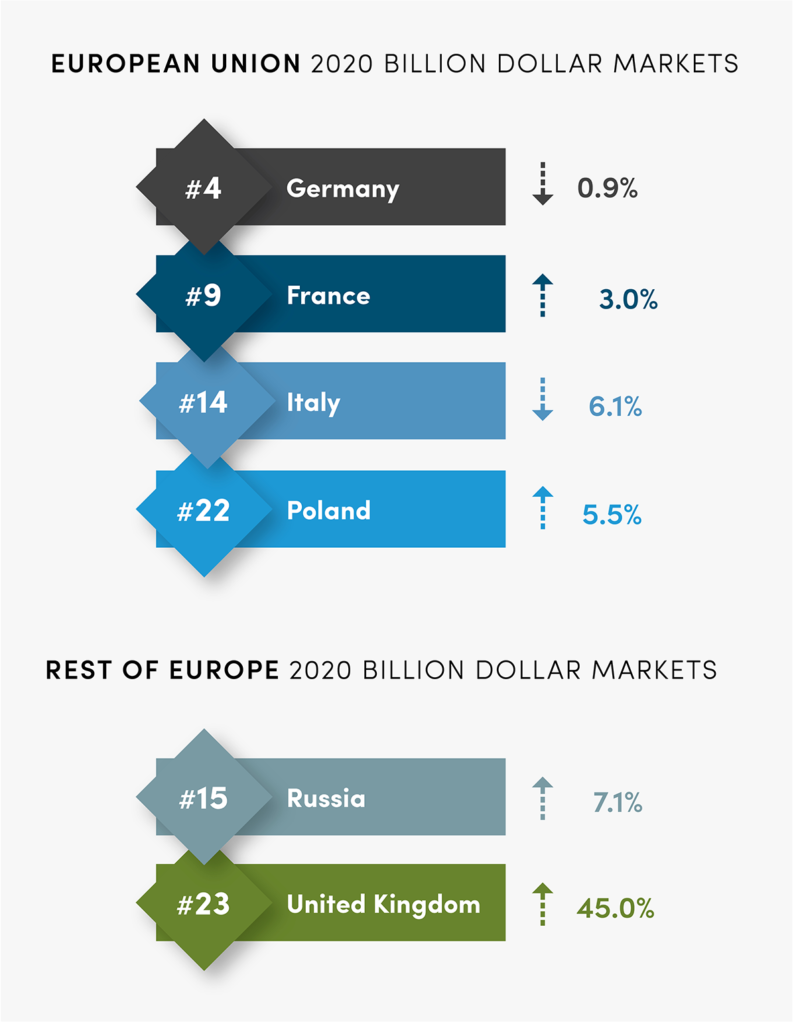

Twenty percent of global direct selling takes place in Europe, and it continues to grow, holding a 1.2 percent CAGR. Since a slight downturn in 2018, Europe’s sales trajectory has been on the rise. In 2020, the regional market increased 1.6 percent, with estimated retail sales for the whole of Europe at $36.2 billion. European Union country markets reported $31.2 billion in estimated retail sales, a slight decrease over 2019; however, following Brexit, the United Kingdom is categorized and reported as Rest of Europe for the first time in 2020.

Independent representatives number 14.5 million in Europe, with 6.7 million living and working within the European Union, and another 7.9 million throughout the Rest of Europe. Wellness (29 percent) and Cosmetics and Personal Care (20 percent) ranked as top product categories; however, Household Goods and Durables increased market share by 6 percent over 2019, posting 20 percent in 2020. Home Improvement products slotted fourth at 13 percent.

Germany moved up a rank to number three on the 2020 Billion Dollar Markets list. It comprised 10 percent of the global marketplace with $18 billion in estimated retail sales, an increase of 0.9 percent, and a CAGR of 2.0 percent. Poland showed increases of 5.5 percent with estimated retail sales for 2020 at $1.1 billion and a 2.8 percent CAGR. France and Italy, the only remaining European Union representatives on the list, were in decline last year. France dropped 3.0 percent with $5.1 billion estimated retail sales, while Italy recorded a 6.1 percent decrease over 2019 with $2.8 billion in estimated retail sales.

Rest of Europe

This sub-region of Europe reported increased estimated retail sales of 12.4 percent totaling $5 billion. The market also showed a 2.0 percent CAGR.

Russia is still the largest player in the region, with 56 percent of sales and estimated retail sales of $2.2 billion. 2020 was a recovery year for Russia, showing an increase of 7.1 percent after two years of slumping sales. Russia’s CAGR has yet to recover, however, and is -1.6 percent. Due to the United Kingdom’s exit from the European Union, that market now reports as the second largest country market in the Rest of Europe with just over $1 billion in estimated retail sales, a 45 percent increase. However, the United Kingdom fell from its previous rank of 11 in 2019 to number 23. This is due to incomplete data and will likely be restated later in the year. Their CAGR is 8.0 percent.

While developing markets within the Rest of Europe lost traction in 2019, there was a turnaround for Norway (up 13 percent), Switzerland (up 7.4 percent), and Turkey (up 5 percent) in 2020. Ukraine posted the only losses, down 8.5 percent.

While product category sales data is not available for the Rest of Europe as a whole, its two largest markets offer insights. Russia reports Cosmetics and Personal Care products took 42 percent, with Wellness at 37 percent. The United Kingdom shows similar results with Cosmetics and Personal Care at 51 percent and Wellness at 29 percent. Independent representative numbers total 7.9 million. DSN

Global factors like lockdowns, job displacement and supply chain disruptions ebbed and flowed from market to market and even within markets producing highs and lows. But the real “big picture” insight for 2020 is how well the industry performed despite those challenges.

About the Research

This collaborative, global data collection effort of the World Federation of Direct Selling Associations, Seldia (The European Direct Selling Association), and local direct selling associations and their member companies around the world, depicts the state of the global direct selling industry for 2020.

Compiled annually, this is a collection of individual market data in local currency figures, which are converted into U.S. dollars using current year constant dollar exchange rates to eliminate the impact of currency fluctuation. All statistics are based on estimated retail sales and in some instances may be restated using actual sales data as they become available. Statistics for some markets represent direct selling association member companies only and not the entire industry in that country. Other statistics are WFDSA research estimates. All statistics expire June 2022.

From the August 2021 issue of Direct Selling News magazine.